Consumers’ Switching from Cash to Mobile Payment under the Fear of COVID-19 in Taiwan

Department of Business Administration, National Central University, Taoyuan City 320, Taiwan

*

Author to whom correspondence should be addressed.

Sustainability 2022, 14(14), 8489; https://doi.org/10.3390/su14148489

Submission received: 30 May 2022

/

Revised: 8 July 2022

/

Accepted: 8 July 2022

/

Published: 11 July 2022

(This article belongs to the Special Issue The Evolution of Consumer Behavior in the Sustainable Business: Evidence from COVID-19)

Abstract

:The COVID-19 pandemic impacts our lives significantly; people have changed their daily lives in response to the unprecedented epidemic which not only awakened the arrival of a new normal in business, but also new lifestyles. For example, the adaptation of contactless mobile payment has grown in the past two years to avoid unnecessary contact and possible infections. In this study, we intend to examine behavioral intentions that made consumers shift from traditional cash payment to mobile payment during the COVID-19 period. Our research framework and hypotheses were developed and examined through the push (dissatisfaction)–pull (alternative attractiveness)–mooring (perceived fear) model. We used structural equation modeling (SEM) to validate our model and corresponding hypotheses. The results of this study showed that dissatisfaction with tradition-al payments and customer’s perceived fears positively and significantly affected switching intentions. However, alternative attractiveness had no significant impact on consumers’ switching intentions from cash to mobile payments during the pandemic. Moreover, this study shows how perceived fear has a mediating effect that motivates people to change their payment behaviors. Implications and future research directions about consumers changing in such a dynamic time are also discussed.

1. Introduction

The COVID-19 epidemic has already changed our businesses and lives significantly in the past two years, it has increased the pace of digital transformation and online business, pushed the booming of online learning and work from home (WFH). These challenges called for new mindsets, new technologies, and new approaches. For example, the requirement of keeping social distance and quarantine made more people change their paying behaviors to use mobile payment for making their purchases offline and online to avoid possible close contact. According to the Global Payment Report released by Worldpay [1], mobile payment has become the most commonly used payment method for consumers around the world, whether it is online shopping or physical consumption, accounting for 49% (USD 2.6 trillion) and 29%, respectively, in 2021 (USD 13.3 trillion); it also predicts that that ratio will rise to 53% and 39% in 2025.

In Taiwan, the convenience for people to use cash and the popularity of credit cards and debit cards made people less motivated to use mobile payment, the use of which was relatively small [1]; however, in recent years, the modification of related laws and regulations by government and proactive promotion by those financial institutions and payment platforms, consumers’ acceptance of mobile payment has become more and more popular. For confronting the global spread of COVID-19 since the end of 2019, the increasing awareness to maintain hygiene and to prevent the epidemic spreading have made more people prefer to use mobile payment whether they shop offline or online [2]. The COVID-19 pandemic accidently increased the rapid popularization of mobile payment and accelerated the development of digitalization.

According to the 2021 Mobile Payment Consumer Survey conducted by the Taiwan Market Intelligence & Consulting Institute [3], it was found that consumers’ preference for mobile payment as their preferred payment method has increased from 37% in 2020 to 50% in 2021. Moreover, Taiwan’s government also listed the development of mobile payment as an important policy and proposed a target of 90% mobile payment penetration by 2025, which shows that mobile payment is on a growing track for further development.

Mobile payment began with the first payment transaction using a mobile device in 1997 [4]. During this period, mobile payment has seen tremendous changes due to the development of new technologies, products, and services. However, mobile payment has still been an attractive topic of study for scholars and practitioners for over 25 years.

It can be confirmed from a recent study which has analyzed and developed the evolution of mobile payment research from 1997 to 2021 [5]. According to their study, from the perspective of behavior, mobile payment can be studied based on various customer behavior factors. For instance, switching behavior [6], consumers’ trust [7], post-adoption behavior [8], etc. Moreover, mobile payment can be studied based on various technological perspectives. Some examples are the integration of the expectation confirmation model with the health belief model [9] and technology continuous theory [10] or UTAUT and protection motivation theory [11].

When we consider the entire action payment life cycle can be divided into three phases: adoption, use, and termination [12], most past research has been conducted with regard the adoption of mobile payment by consumers as the adoption of emerging technologies by consumers, focusing on the intention of adoption, and works seldom explore the conversion behavior of consumers from traditional cash payment to mobile payment [13,14]. Past research, however, has only explained the adoption and continued use of mobile payments from a single perspective that ignores the barriers that come with cash [15,16].

Because consumer switching behavior is a complex decision, we consider the process of consumer adoption of mobile payments as a dynamic process of switching from traditional payment methods to emerging payment methods. To clarify this issue, this study applies push–pull–mooring (PPM) to understand consumers’ switching behavior from traditional payment to mobile payment under the COVID-19 pandemic. To address such a specific context, we incorporated the perceived fear of COVID-19 as our mooring factor and considered consumers’ switching from cash to contactless mobile payment as the realization of protection motivation to understand whether it is an important factor for hindering or promoting migration decisions to switch into mobile payment during the epidemic.

Our research goal is to explore consumers’ switching intentions between cash and mobile payments through a push–pull–mooring (PPM) model. We argue this work may make some important contributions to the field. First, this study used a more comprehensive push–pull–mooring (PPM) model to examine consumers’ switching behavior from cash to mobile payment. Second, pull and push factors under the PPM model have been used to examine the use of consumers’ mobile payments [17,18], but how mooring factors may affect such switching behavior is less discussed. We used perceived fear under COVID-19 as a mooring factor to scrutinize if such a fear has a direct or indirect effect for consumers to use mobile payment instead of paying by cash. Finally, we generate results to offer suggestions for mobile payment service providers to attract potential customers as well as to retain existing customers.

This paper is organized as follows. Next, recent literature will be discussed, followed by the research methods and results. We conclude with further discussions and conclusions at the end of this work.

2. Literature Review

2.1. Mobile Payment

Mobile payments can be used as long as the mobile network is used, regardless of the use of voice, short message service (SMS) or near-field communication (NFC) [19]. Mobile payment (M-payment) is a payment method that combines physical payment tools with mobile vehicles, it can be divided into the following two categories [20]. Based on the technologies used, the first one is the remote mobile payment (RMP), a transaction through the e-commerce network. Remote payment allows consumers to transfer an amount of money at any time without being restricted by space, time, and location. The mobile phone does not need to be near any card reader or sensor to complete the payment operation. Most of these payment methods require the credit card or debit card information to be entered in advance or at the payment moment, and the security measures of the consumption authorization code are used to deduct the payment. The other is the proximity mobile payment (PMP), the near-end transaction using a smartphone to pay; with the physical card data stored in the mobile phone, consumers use near-field communication (NFC) technology or scan the QR code provided by the sellers to complete the transaction payment in the physical store.

According to the statistics of National Credit Card Center of R.O.C [21], in Taiwan, mobile payment accounted for 20.2% and 7.8% of the total credit card consumption in September 2021, an increase of 28% over the same period last year, the payment amount increased by 59%; it shows that consumers’ payment habits have changed, and the adaption of mobile payment increased gradually. When the COVID-19 pandemic spread around the world, the nature of contactless in using M-payments made many people change their payment habits to adapt different M-payment services around their living environments. Compared with using traditional cash to conduct transactions, mobile payment not only reduces contact risks, improves epidemic prevention security, transaction convenience, etc., but also avoids the risk of physical cash or card loss [14].

Because M-payment transactions are delivered digitally and globally, consumers can check historical transaction records at any time to grasp the accounting status, and invoices can also be stored electronically, which is environmentally friendly. In addition, for sellers and retail channels, mobile payment can reduce merchants’ checkout errors, reduce the risk of cash theft and accounting errors, and also has the advantages of collecting big data and further business analytics, so that they can use consumers’ transaction data and purchasing behaviors and habits to conduct follow-up analysis for developing new marketing strategies and new products/services [14,22]. Actually, it is beneficial for both buyers and sellers.

2.2. Push–Pull–Mooring (PPM) and Switching Intention

In this study, we develop our framework based on the push–pull–mooring (PPM) model, it originated from the migration theory that considers factors that affect people’s migration decisions are divided into push, pull and mooring [23]. In general understanding, a pushing force is a negative factor that prompts people to migrate from the original place a pulling force is a positive factor that attracts people to migrate to another alternative location, and a mooring is a locking factor that affects or hinders the cause of migration [12,24].

In fact, ideas of PPM model have been used in different research topics, including consumer behavior research, to further explore consumers’ switching intentions between different service providers [25,26]. Actually, consumers often compare two products or services and switch in different environments or conditions. Such switching behaviors are similar to migration behaviors; people change their perceptions and attitudes on the one hand, and they are replaced by alternatives on the other hand [27]. We consider that the consumer switching behavior is highly similar to human migration [26,28]. Therefore, we chose to use the PPM model attempts to establish this research framework to explore the conversion behavior between cash and mobile payment. In our study, switching refers to the complete terminating of an existing product or service, but existing services and alternative services may be used at the same time; therefore, we define switching intent as consumers’ willingness to change their way to pay, whether they choose to pay via cash or to pay via mobile payment [29].

2.2.1. Push (Dissatisfaction)

In this research, push is considered as a negative factor that drives consumers to be reluctant to use existing products or services [30] (cash payment in this study), and its main factor is dissatisfaction with existing products or services [31]. This study defines dissatisfaction as consumers’ overall evaluation of past experiences with cash payment.

Past studies have confirmed that consumer dissatisfaction with existing products or services positively affects consumers’ willingness to switch [32,33,34]; therefore, satisfied consumers continue to use the product or service, while dissatisfied consumers consider switching to other alternatives. Satisfaction has been identified as an important determinant of consumer switching intent.

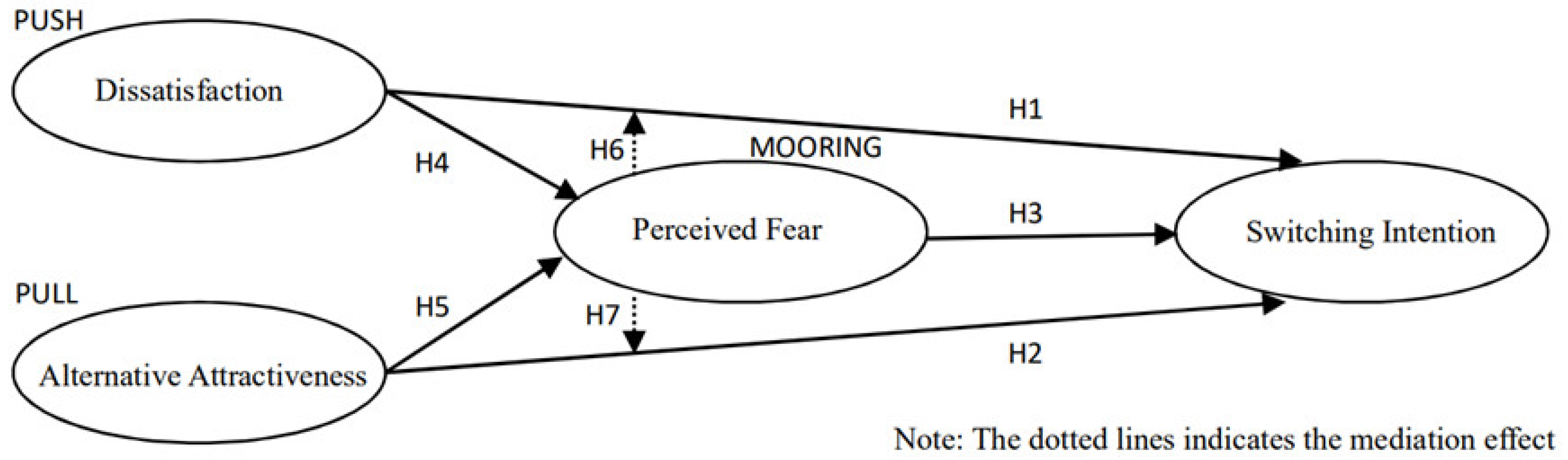

Hypothesis 1 (H1).

Dissatisfaction has a significant positive impact on switching intention from cash to M-payment.

2.2.2. Pull (Alternative Attractiveness)

In this study, alternative attractiveness refers to the attractiveness of M-payment as an alternative to cash. When consumers believe that M-payment is better than cash, there is a tendency for higher frequencies of switching to M-payment.

M-payment provides a convenient transaction process, including pre-purchase and post-purchase, and provides consumers with a safe, fast, and convenient way to transact [35,36,37]. Such convenience will increase consumers’ willingness to use mobile payment [36,38], this convenience can be treated as alternative attractiveness for consumers to change their payment behavior. In this work, we refer to such alternative attractiveness as a pull factor; the attractiveness of mobile payment that is considered as an alternative to pay in cash.

Therefore, when consumers think that the attractiveness of mobile payment is higher than that of cash, the intention to switch is stronger. This is the attractiveness of M-payment, and it is also a pull for consumers. Past research has shown that alternative attractiveness and conversion intention are positively related [14]. Therefore, we believe that alternative attractiveness will positively affect consumers’ willingness to switch from cash to M-payment during the epidemic and proposed our second hypothesis:

Hypothesis 2 (H2).

Alternative attractiveness has a significant positive impact on switching intention from cash to M-payment.

2.2.3. Mooring (Perceived Fear)

We considered mooring as a personal or situational effect that may promote or hinder consumers’ intentions to switch to mobile payment [26]. For example, fear is the mechanism by which individuals protect themselves from dangerous situations [39]. During the rapid spread of COVID-19 around the world, fear of losing health and life, fear of being fired or unemployed, and fear of declining economic situations all bring psychological distress to people [40,41,42]. Due to the COVID-19 pandemic, with an increasing number of studies confirming that fear has a positive correlation with consumer behavior [43], fear may drive and accelerate the adoption of technologies or techniques, such as mobile payment, that can minimize these fears [44]. Therefore, we hypothesize that fear influences an individual’s intention to engage in health-focused behavior, which leads consumers to use contactless mobile payment. It is well documented in past studies that hope and fear motivate people to engage in mitigating behaviors toward a threat [45,46,47]. For example, the fear of environmental threats leads to engagement in protective behaviors [48]. Emotions, such as fear and hope, were found to affect consumers’ purchase decision making [49,50,51]. For example, emotions play a critical role in restaurant consumer behaviors because of threat [47]; some studies in disease and health communication have supported the direct relationship between customers’ protection motivation and their health-focused behaviors [52,53].

The proposed research model indicates that emotional responses, such as fear, generated from cognitive evaluations of the threat play an important role in shaping customer switching behaviors. Therefore, this study includes perceived fear as mooring and hypothesize that a perceived fear will positively affect consumers’ willingness to switch from cash to action payment during the epidemic.

Hypothesis 3 (H3).

Perceived fear has a significant positive impact on switching intention from cash to M-payment.

At the same time, due to consumers’ dissatisfaction with traditional cash payment and the risks brought by the attractiveness of mobile payment, which may increase perceived fear, this study proposes the following hypotheses:

Hypothesis 4 (H4).

Dissatisfaction has a significant positive impact on perceived fear.

Hypothesis 5 (H5).

Alternative attractiveness has a significant positive impact on perceived fear.

2.3. Mediating Effect

Aside from examining the push (dissatisfaction), pull (alternative attractiveness), and mooring (perceived fear) model we developed, we also consider whether perceived fear has a mediating effect in consumers’ switching behavior from using cash to M-payment. According to the 2021 Mobile Payment Consumer Survey [3], mobile payment is the payment method that consumers used the most frequently during the epidemic, and cash payment is the one that reduces the frequency the most, and reasons for using mobile payment during the epidemic were in order of convenience, discounts, and hygiene. This survey also shows the hygiene factor has the highest increase, up 14% compared with 2020, and the preferential factor is down 7%. We argue that consumers have attached great importance to contactless demand during the epidemic, which in turn attracts non-users to start using mobile payment. Therefore, the following hypotheses are proposed:

Hypothesis 6 (H6).

Perceived fear mediates the effect of dissatisfaction on switching intention from cash to M-payment.

Hypothesis 7 (H7).

Perceived fear mediates the effect of alternative attractiveness on switching intention from cash to M-payment.

3. Research Methods

Based on the above discussions, our research conceptual model is shown as Figure 1, while these hypothesized relationships are tested in the empirical study that follows. In this study, we designed a questionnaire with measures of the relevant constructs primarily based on scales taken from past research literature.

All the measurements for the constructs in this model were measured by multiple items, each with a 5-point Likert type scale ranging from 1 (strongly disagree) to 5 (strongly agree). Specifically, four items were used to measure each of the constructs: dissatisfaction [31,54], alternative attractiveness [25,55], perceived fear [56,57] and switching intention [58,59]; Table 1 provides a summary of the measures. All the measurements were adapted and revised from previous studies to match this study.

The target of analysis was customers who used both cash and M-payment in Taiwan physical stores during the COVID-19 pandemic. To restrict the data, only people with experience of using M-payment after December 2019 were selected. In fact, the major leading technologies that facilitate M-payment at present mainly include NFC and QR code [60]. For this study we also focus on NFC (Apple Pay, Google Pay, etc.) and QR code (LinePay, JAKPAY, PX Pay and FamiPay, etc.) payments.

The questionnaire encompassed three parts. The first part consisted of different questions just to check the respondent’s interest levels and his/her awareness about the subject. This part of the questionnaire also verified the respondent’s previous experience of using M-payment and certain filter questions were added to weed out the unsuitable participants. The second part comprised questions related to measurement items. The third part covered the respondent’s profile and details.

Using the convenience sampling approach, a total of 654 samples were collected via two ways: paper-and-pencil questionnaire and online questionnaire. After deleting invalid observations, 590 valid samples remained. These 590 samples were adequate enough to conduct a Confirmatory Factor Analysis (CFA) and a Structural Equation Modeling (SEM), exceeding the absolute minimum sample size [61]. Several researchers suggest that the number of subjects should be at least ten times that of the questionnaire items (i.e., 16 in this current study) [62]. In this way, the minimal number of respondents was 160 for this study, which recruited a total of 590 samples. Therefore, the final sample size was deemed acceptable for achieving statistically significant results.

In total, 45% were male and 55% were female. In terms of their age, those aged 26–34 years old accounted for 55% of the sample, while ages 35–44 accounted for 23%. The respondent experience with M-payment was dominated with one to two years’ experience, at 52%, followed by 31% that only had one year of experience; 3% had more than two years’ experience, and 6% had half a year of experience. Finally, 68% of the participants were college graduates and had a university degree.

In order to test our hypotheses, we employed SEM with Amos 19. First, we used descriptive statistics to define a demographic profile. Second, we established the quality and adequacy of measurement through CFA by ensuring reliability and convergent and divergent validity. Lastly, we employed path analysis in SEM in order to investigate the hypothesized relationships among the variables.

4. Results

4.1. Results of the Measurement Model

The details of the measurement model are presented in Table 2. The results of the CFA (confirmatory factor analysis) using a maximum likelihood estimation method on 16 items indicated that the model was an excellent fit for the data (χ2 = 319.846, df = 98, p < 0.001; RMSEA = 0.062; RMR = 0.04, GFI = 0.934, CFI = 0.943). Cronbach’s alpha was greater than the recommended minimum standard of 0.60 for each group [63].

The composite reliability (CR) values for all constructs ranged from 0.793 to 0.825, a previous study [64] recommended a CR equal to or greater than 0.60.

These results provided evidence of internal consistency among the multiple measurement items for each construct. The average variances extracted (AVE) for all constructs ranged from 0.500 to 0.544, which is greater than 0.5, and thus demonstrates convergent validity [65]. Table 3 shows the means, the standard deviations, and the correlations matrix for those constructs we examined. Overall, the results indicate that the study measures possess adequate fit, reliability, and validity. The following section presents the structural model in detail.

4.2. Results of the Structural Model

The proposed model was tested through SEM (structural equation modeling). The results of the SEM showed that the proposed model was an adequate fit for the data: χ2 = 246.82 (df = 69, p < 0.001); RMSEA = 0.052; RMR = 0.034; GFI = 0.95; CFI = 0.962; NFI = 0.939. The details of the model are presented in Table 4.

Dissatisfaction had a positive significant impact on both switching intention (β = 0.302, p < 0.001) and perceived fear (β = 0.394, p < 0.001). Therefore, Hypotheses 1 and 4 were also supported. However, the linkage from alternative attractiveness to switching intention was found to be insignificant (β = −0.008, p > 0.05), failing to support Hypothesis 2. Furthermore, the hypothesized path from perceived fear to switching intention was significant, which supports Hypothesis 3 (β = 0.631, p < 0.001). Finally, the relationship between alternative attractiveness and perceived fear was assessed and showed a positive and significant result to support Hypothesis 5 (β = 0.320, p < 0.001).

In order to better clarify the theoretical process to explaining our model, we explored the relevant mediating roles by examining their direct and indirect effects in each path. The standardized direct and indirect effects are summarized in Table 5. The total effects of the constructs on switching intention (direct effect plus indirect effect) can be ranked as follows: dissatisfaction (0.548), alternative attractiveness (0.200), and perceived fear (0.628). Although alternative attractiveness has no direct and significant effect on switching intention, it can indirectly influence switching intention through perceived fear. Therefore, we argued that enhancing alternative attractiveness will eventually lead to higher switching intention.

5. Discussions

5.1. The Findings

Our findings add new insights to the literature on the switching intention of mobile payment. From the perspective of switching behavior, this study explores consumers’ switching intentions between cash and mobile payment during COVID-19, based on the PPM theory, and explores the impact of perceived fear.

The results of this study showed that all hypotheses proposed in this study are valid, except for H2. This suggests that alternative attractiveness had no significant impact on consumers’ switching intentions from cash to mobile payments during the pandemic. Many studies in the past found when consumers consider that M-payment is better than cash, there is a higher tendency for the frequency of switching to M-payment. Particularly in mobile-related studies [14,55,61]. This could be attributed to the fact that privacy and security issues are among the most important concerns for customers in predicting switching behavior [60,66], which is regarded as one of the largest barriers to adopting mobile payment services [67].

In addition, there are many mobile payment providers in Taiwan; each service provider has its own special user interface, features, functions, etc. Therefore, consumers can choose one or more mobile payment providers that are compatible and match to their lifestyles. However, there are more and more choices, but they cannot complete cross-channel transactions with each other, which causes transaction inconvenience. In contrast, cash can be taken anytime and transacted anywhere in a physical store.

In contrast, this is consistent with previous research findings that dissatisfaction with cash payment pushes consumers away from the original choice [25,32], as well as how people may choose to use mobile payment because of perceived fear [40,44]. In addition, among the three factors of PPM, the conversion intention brought by mooring has the greatest influence in our study. We argue that the main reason for consumers to switch to mobile payment under COVID-19 is the perceived fear they feel.

Another focus of this study is to explore the role of perceived fear in switching intentions. In the past, few studies have explored the direct and indirect effects of PPM, especially the locking force Mooring. This study confirms that perceived fear has direct and indirect effects in this research framework.

5.2. Theoretical Implications

This study advances our understanding of the formation of switching intention within the emerging context of M-payment. Even though many kinds of literature have shed light on m payment from user’s adoption perspective, pre adoption and post-adoption perspective, and continuous usage perspective [13,14], a comprehensive study of why consumers switch between cash payment and M-payment has yet to be conducted. This study fills the gaps in current literature under M-payment context.

In terms of the PPM model, this study investigates the intention to switch to mobile payment from three aspects, push factors forcing customers to be away from incumbent payment services, pull factors attracting users to mobile payment services, and mooring factors either encouraging or hindering switching behavior.

This study demonstrated that push (dissatisfaction) and mooring (perceived fear) have a significant effect on the intention to shift cash payments to action payments during the COVID-19. However, consumers’ intention to switch to M-payment have no significant impact on pull (alternative attractiveness).

5.3. Managerial Implications

Mobile payment can be used as a substitute for paper payment methods such as cash and check, which can improve the efficiency, convenience, record keeping, etc. [66].

However, surprisingly, the results of this study showed that during the COVID-19 pandemic, pull factor (alternative attractiveness) had no significant impact on consumers’ switching from cash to mobile payment, but push and mooring factors did affect consumers’ switching intention.

First of all, alternative attractiveness do not affect switching intention to mobile payment. This finding is not in agreement with prior studies such as [22,55], that may attribute to the possibility of risks and uncertainties in using mobile payment transactions, such as security and privacy concerns [14,58,67]. Today’s consumers are far more concerned about financial fraud and loss of sensitive data when using M-payment [68]. Our research indicates that M-payment providers should upgrade technologies regularly and enhance their degree of security, and should responsible for protecting customers’ assets from loss. Additionally, deriving legal issues from e-commerce, it is an important issue and we should be concerned with, such as in recent research discussing the present possibilities of e-commerce in the conditions of the Slovak Republic, especially in the context of consumer protection [69]. Thus, the government should help to provide technical and legal structured assurances to help mobile payment customers feel more safe and secure. This can be achieved by updating the relevant laws to address current issues of data privacy and consumer rights protection. Therefore, the overall suggestion is to create a friendly and positive environment to develop the habit of using M-payment.

Second, more and more mobile payment apps are offered by different companies and platform vendors, which may bother some consumers when trying to choose, therefore, cash still remains a valuable payment tool in most situations.

On the other hand, among the three factors of PPM, dissatisfaction with traditional payments and customers’ perceived fear positively and significantly affected switching intention. Our study indicates that customers are more willing to switch to M-payment due to dissatisfaction with cash payment. Therefore, M-payment providers have to establish and conduct promotional campaigns and compare the functions of M-payment with cash payments, especially emphasizing the importance of contactless payment.

6. Conclusions

This study has enhanced our understanding of the formation of switching intention in the context of M-payment. Although this study has several theoretical and managerial implications, it has several limitations. The targets of this study were customers who had experience using mobile payment during the COVID-19 pandemic. However, for some customers the switch may have already occurred before the outbreak of COVID-19. Therefore, it is suggested to compare customers who had experience using mobile payment prior to and after the COVID-19 pandemic. Furthermore, this study used the PPM model to explore the influencing factors of switching from cash to mobile payment and explores the mediating effect of perceived fear in epidemic times. However, this study did not discuss interfering variables. It is suggested that demographic variables, such as gender and ages can be included for discussion to further understand the differences and provide reference for future promotion or research.

Considering our research limitations in sampling and lack of interfering variables, such as demographic variables in detail, that can be improved in further study, we propose other future research directions here. First, what kind of institutional environment can significantly promote contactless, mobile payment service still needs to be explored, especially in different countries and regions have their own context-specific issues to address, in spite of concerns of privacy and information security that consumers always aware [69].

Second, competition among different mobile payment vendors and platforms could be an interesting inquiry whether during the pandemic or not, future studies may consider how they attract and maintain consumers. Except the PPM model we adopted in this study, future research can consider other consumer behavior perspectives, such as mental accounting theory [2], to further explore consumers’ switching behaviors.

Third, transitioning to a new normal in the post-COVID era, large-scale digital innovation practices, such as working from home, telemedicine, and online learning, not only change people’s daily routines and consumption, but also greatly promote the development of smart cities. Digital payments form an integral part of the smart cities vision. The limitation of this study is that it only examined within the context of M-payment; therefore, future research can refer to our framework to explore other digital transformations in other contexts of study. This could include examples of smart cities around the world [70].

Finally, this study was conducted as a cross-sectional study after the announcement of COVID-19 as a worldwide pandemic. Digital and mobile technology is continually improving and evolving, future studies could also be used to consider a longitudinal approach. This will allow researchers to gauge the changes in factors and observe the differences over time, which would help us understand the trends and changes in consumer behaviors.

Author Contributions

Conceptualization, D.C.C. and S.-Y.Y.; methodology, S.-Y.Y.; software, S.-Y.Y.; validation, D.C.C. and S.-Y.Y.; formal analysis, D.C.C. and S.-Y.Y.; investigation, S.-Y.Y.; resources, S.-Y.Y.; data curation, S.-Y.Y.; writing—original draft preparation, S.-Y.Y.; writing—review and editing, D.C.C.; visualization, D.C.C. and S.-Y.Y.; supervision, D.C.C.; project administration, S.-Y.Y. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Not applicable.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Worldpay. Global Payments Reports. 2022. Available online: https://worldpay.globalpaymentsreport.com/ (accessed on 9 April 2022).

- Zhao, Y.; Bacao, F. How does the pandemic facilitate mobile payment? An investigation on users’ perspective under the COVID-19 pandemic. Int. J. Environ. Res. Public Health 2021, 18, 1016. [Google Scholar] [CrossRef] [PubMed]

- Market Intelligence & Consulting Institute. 2021 Mobile Payment Consumer Survey. Available online: https://mic.iii.org.tw/news.aspx?id=617 (accessed on 10 April 2022).

- Dahlberg, T.; Guo, J.; Ondrus, J. A critical review of mobile payment research. Electron. Commer. Res. Appl. 2015, 14, 265–284. [Google Scholar] [CrossRef]

- Leong, L.Y.; Hew, J.J.; Wong, L.W.; Lin, B. The past and beyond of mobile payment research: A development of the mobile payment framework. Internet Res. 2022. ahead of print. [Google Scholar] [CrossRef]

- Fan, L.; Zhang, X.; Rai, L.; Du, Y. Mobile payment: The next frontier of payment systems? An empirical study based on push-pull-mooring framework. J. Theor. Appl. Electron. Commer. Res. 2021, 16, 155–169. [Google Scholar] [CrossRef]

- Talwar, S.; Dhir, A.; Khalil, A.; Mohan, G.; Islam, A.N. Point of adoption and beyond. Initial trust and mobile-payment continuation intention. J. Retail. Consum. Serv. 2020, 55, 102086. [Google Scholar] [CrossRef]

- Singh, S. An integrated model combining the ECM and the UTAUT to explain users’ post adoption behaviour to-wards mobile payment systems. Australas. J. Inf. Syst. 2020, 24, 1–27. [Google Scholar]

- Sreelakshmi, C.C.; Prathap, S.K. Continuance adoption of mobile-based payments in COVID-19 context: An integrated framework of health belief model and expectation confirmation model. Int. J. Pervasive Comput. Commun. 2020, 16, 351–369. [Google Scholar]

- Daragmeh, A.; Sagi, J.; Zeman, Z. Continuous intention to use e-wallet in the context of the COVID-19 pandemic: Integrating the health belief model (HBM) and technology continuous theory (TCT). J. Open Innov. Technol. Mark. Complex. 2021, 7, 132. [Google Scholar] [CrossRef]

- Srivastava, C.; Mahendar, G.; Vandana, V. Adoption of contactless payments during COVID-19 pandemic—An integration of protection motivation theory (PMT) and unified theory of acceptance and use of technology (UTAUT). Acad. Mark. Stud. J. 2021, 25, 2678. [Google Scholar]

- Wang, L.; Luo, X.R.; Yang, X.; Qiao, Z. Easy come or easy go? Empirical evidence on switching behaviors in mobile payment applications. Inf. Manag. 2019, 56, 103150. [Google Scholar] [CrossRef]

- Handarkho, Y.D.; Harjoseputro, Y. Intention to adopt mobile payment in physical stores: Individual switching behavior perspective based on Push–Pull–Mooring (PPM) theory. J. Enterp. Inf. Manag. 2019, 33, 285–308. [Google Scholar] [CrossRef]

- Loh, X.M.; Lee, V.H.; Tan, G.W.H.; Ooi, K.B.; Dwivedi, Y.K. Switching from cash to mobile payment: What’s the hold-up? Internet Res. 2021, 31, 376–399. [Google Scholar] [CrossRef]

- Ye, C.; Seo, D.; Desouza, K.C.; Sangareddy, S.P.; Jha, S. Influences of IT substitutes and users experience on post adoption user switching: An empirical in vestigation. J. Am. Soc. Inf. Sci. Technol. 2008, 59, 2115–2132. [Google Scholar] [CrossRef]

- Ye, C.; Potter, R. The role of habit in post-adoption switching of personal information technologies: An empirical investigation. Commun. Assoc. Inf. Syst. 2011, 28, 35. [Google Scholar] [CrossRef]

- Kim, C.; Mirusmonova, M.; Lee, I. An empirical examination of factors influencing the intention to use mobile payment. Comput. Hum. Behav. 2010, 26, 310–322. [Google Scholar] [CrossRef]

- Oliveira, T.; Thomas, M.; Baptista, G.; Campos, F. Mobile payment: Understanding the determinants of customer adoption and intention to commend the technology. Comput. Hum. Behav. 2016, 61, 404–414. [Google Scholar] [CrossRef]

- Bank for International Settlements. 2012 Innovations in Retail Payments. Available online: https://www.bis.org/cpmi/publ/d102.htm (accessed on 10 April 2022).

- Vizzarri, A.; Vatalaro, F. M-Payment systems: Technologies and business models. In Proceedings of the 2014 Euro Med Telco Conference (EMTC), Naples, Italy, 12–15 November 2014; pp. 1–6. [Google Scholar] [CrossRef]

- National Credit Card Center of R.O.C. Explore the Trend of NFC and QR Payment 2021. Available online: https://www.nccc.com.tw/wps/wcm/connect/zh/home/openinformation/CaseAnalysisIntroduce/CNT_05_998_20211201133516 (accessed on 10 April 2022).

- Purwandari, B.; Suriazdin, S.A.; Hidayanto, A.N.; Setiawan, S.; Phusavat, K.; Maulida, M. Factors affecting switching intention from cash on delivery to e-payment services in c2c e-commerce transactions: COVID-19, transaction, and technology perspectives. Emerg. Sci. J. 2022, 6, 136–150. [Google Scholar] [CrossRef]

- Chiu, H.C.; Hsieh, Y.C.; Roan, J.; Tseng, K.J.; Hsieh, J.K. The challenge for multichannel services: Cross-channel free-riding behavior. Electron. Commer. Res. Appl. 2011, 10, 268–277. [Google Scholar] [CrossRef]

- Mu, H.L.; Lee, Y.C. Will proximity mobile payments substitute traditional payments? Examining factors influencing customers’ switching intention during the COVID-19 pandemic. Int. J. Bank Mark. 2022, 40, 1051–1070. [Google Scholar] [CrossRef]

- Sun, Y.; Liu, D.; Chen, S.; Wu, X.; Shen, X.L.; Zhang, X. Understanding users’ switching behavior of mobile instant messaging applications: An empirical study from the perspective of push-pull-mooring framework. Comput. Hum. Behav. 2017, 75, 727–738. [Google Scholar] [CrossRef]

- Bansal, H.S.; Taylor, S.F.; James, Y.S. Migrating to new service providers: Toward a unifying framework of consumers’ switching behaviors. J. Acad. Mark. Sci. 2005, 33, 96–115. [Google Scholar] [CrossRef]

- Keaveney, S.M. Customer switching behavior in service industries: An exploratory study. J. Mark. 1995, 59, 71–82. [Google Scholar] [CrossRef]

- Hsieh, P.J. Understanding medical consumers’ intentions to switch from cash payment to medical mobile payment: A perspective of technology migration. Technol. Forecast. Soc. Chang. 2021, 173, 121074. [Google Scholar] [CrossRef]

- Peng, X.; Zhao, Y.; Zhu, Q. Investigating users switching intention for mobile instant messaging applications: Taking WeChat as an example. Comput. Hum. Behav. 2016, 64, 206–216. [Google Scholar] [CrossRef] [Green Version]

- Venkatesh, V.; Morries, M.G.; Davis, G.B. User acceptance of information technology: Toward a unified view. MIS Q. 2003, 27, 425–478. [Google Scholar] [CrossRef] [Green Version]

- Bhattacherjee, A. Understanding information systems continuance: An expectation-confirmation model. MIS Q. 2001, 25, 351–370. [Google Scholar] [CrossRef]

- Chang, I.C.; Liu, C.C.; Chen, K. The push, pull and mooring effects in virtual migration for social networking sites. Inf. Syst. J. 2014, 24, 323–346. [Google Scholar] [CrossRef]

- Fan, L.; Suh, Y.H. Why do users switch to a disruptive technology? An empirical study based on expectation-disconfirmation theory. Inf. Manag. 2014, 51, 240–248. [Google Scholar] [CrossRef]

- Bhattacherjee, A.; Park, S.C. Why end-users move to the cloud: A migration-theoretic analysis. Eur. J. Inf. Syst. 2014, 23, 357–372. [Google Scholar] [CrossRef]

- De Kerviler, G.; Demoulin, N.T.M.; Zidda, P. Adoption of in-store mobile payment are perceived risk and convenience the only drivers. J. Retail. Consum. Serv. 2016, 31, 334–344. [Google Scholar] [CrossRef]

- Teo, A.; Tan, G.W.; Ooi, K.B.; Lin, B. Why consumers adopt mobile payment? A partial least squares structural equation modelling (PLS-SEM) approach. Int. J. Mob. Commun. 2015, 13, 478–497. [Google Scholar] [CrossRef]

- Porath, M. Immediate payments: Beyond ubiquity, convenience speed and security paving the road to a cashless society. J. Digit. Bank. 2017, 1, 349–357. [Google Scholar]

- Hayashi, F. Mobile Payments: What’s in it for consumers? Federal Reserve Bank of Kansas City. Econ. Rev. 2012, 97, 35–66. [Google Scholar]

- Williams, K.C. Improving fear appeal ethics. J. Acad. Bus. Ethics 2011, 5, 1–24. [Google Scholar]

- Al-Maroof, R.S.; Salloum, S.A.; Hassanien, A.E.; Shaalan, K. Fear from COVID-19 and technology adoption: The impact of Google Meet during Coronavirus pandemic. Interact. Learn. Environ. 2020, 1–16. [Google Scholar] [CrossRef]

- Mamun, M.A.; Griffiths, M.D. First COVID-19 suicide case in Bangladesh due to fear of COVID-19 and xenophobia: Possible suicide prevention strategies. Asian J. Psychiatry 2020, 51, 102073. [Google Scholar] [CrossRef]

- Pakpour, A.H.; Griffiths, M.D.; Lin, C.Y. Assessing psychological response to the COVID-19: The fear of COVID-19 scale and the COVID stress scales. Int. J. Ment. Health Addict. 2021, 19, 2407–2410. [Google Scholar] [CrossRef]

- Addo, P.C.; Jiaming, F.; Kulbo, N.B.; Liangqiang, L. COVID-19: Fear appeal favoring purchase behavior towards personal protective equipment. Serv. Ind. J. 2020, 40, 471–490. [Google Scholar] [CrossRef] [Green Version]

- Brem, A.; Viardot, E.; Nylund, P.A. Implications of the coronavirus (COVID-19) outbreak for innovation: Which technologies will improve our lives? Technol. Forecast. Soc. Chang. 2021, 163, 120451. [Google Scholar] [CrossRef]

- Makarem, S. Emotions and cognitions in consumer health behaviors: Insights from chronically ill patients into the effects of hope and control perceptions. J. Consum. Behav. 2016, 15, 208–215. [Google Scholar] [CrossRef]

- Smith, N.; Leiserowitz, A. The role of emotion in global warming policy support and opposition. Risk Anal. 2014, 34, 937–948. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Kim, J.; Yang, K.; Min, J.; White, B. Hope, fear, and consumer behavioral change amid COVID-19: Application of protection motivation theory. Int. J. Consum. Stud. 2022, 46, 558–574. [Google Scholar] [CrossRef] [PubMed]

- Janmaimool, P. Application of protection motivation theory to investigate sustainable waste management behaviors. Sustainability 2017, 9, 1079. [Google Scholar] [CrossRef] [Green Version]

- Halevy, N. Preemptive strikes: Fear, hope, and defensive aggression. J. Personal. Soc. Psychol. 2017, 112, 224–237. [Google Scholar] [CrossRef]

- Krishen, A.S.; Bui, M. Fear advertisements: Influencing consumers to make better health decisions. Int. J. Advert. 2015, 34, 533–548. [Google Scholar] [CrossRef]

- Macinnis, D.J.; Mello, G.E. The concept of hope and its relevance to product evaluation and choice. J. Mark. 2005, 69, 1–14. [Google Scholar] [CrossRef]

- Cho, H.; Lee, J.S. The influence of self-efficacy, subjective norms, and risk perception on behavioral intentions related to the H1N1 flu pandemic: A comparison between Korea and the US. Asian J. Soc. Psychol. 2015, 18, 311–324. [Google Scholar] [CrossRef]

- Prati, G.; Pietrantoni, L.; Zani, B. Influenza vaccination: The persuasiveness of messages among people aged 65 years and older. Health Commun. 2012, 27, 413–420. [Google Scholar] [CrossRef]

- Thakur, R. Understanding customer engagement and loyalty: A case of mobile devices for shopping. J. Retail. Consum. Serv. 2016, 32, 151–163. [Google Scholar] [CrossRef]

- Chuah, S.H.W.; Rauschnabel, P.A.; Tseng, M.L.; Ramayah, T. Reducing temptation to switch mobile data service providers over time: The role of dedication vs constraint. Ind. Manag. Data Syst. 2018, 118, 1597–1628. [Google Scholar] [CrossRef]

- Gerhold, L. COVID-19: Risk perception and coping strategies. PsyArXiv 2020, 25. [Google Scholar] [CrossRef] [Green Version]

- Huynh, T.L.D. Data for Understanding the Risk Perception of COVID-19 from Vietnamese Sample. Data Brief 2020, 30, 105530. [Google Scholar] [CrossRef] [PubMed]

- Cheng, S.; Lee, S.J.; Choi, B. An empirical investigation of users’ voluntary switching intention for mobile personal cloud storage services based on the push-pull-mooring framework. Comput. Hum. Behav. 2019, 92, 198–215. [Google Scholar] [CrossRef]

- Zhou, T. Understanding users’ switching from online stores to mobile stores. Inf. Dev. 2016, 32, 60–69. [Google Scholar] [CrossRef] [Green Version]

- De Luna, I.R.; Liébana-Cabanillas, F.; Sánchez-Fernández, J.; Muñoz-Leiva, F. Mobile payment is not all the same: The adoption of mobile payment systems depending on the technology applied. Technol. Forecast. Soc. Chang. 2019, 146, 931–944. [Google Scholar] [CrossRef]

- Hair, J.F.; Anderson, R.E.; Tatham, R.L.; Black, W.C. Multivariate Data Analysis, 8th ed.; Prentice-Hall: Upper Saddle River, NJ, USA, 1998. [Google Scholar]

- Comrey, A.L. Factor-analytic methods of scale development in personality and clinical psychology. J. Consult. Clin. Psychol. 1988, 56, 754. [Google Scholar] [CrossRef]

- Cuieford, J.P. Fundamental Statistics in Psychology and Education, 4th ed.; MacGraw-Hill: New York, NY, USA, 1965. [Google Scholar]

- Bagozzi, R.P.; Yi, Y. On the evaluation of structural equation models. J. Acad. Mark. Sci. 1988, 16, 74–94. [Google Scholar] [CrossRef]

- Fornell, C.; Larcker, D.F. Evaluating structural equation models with unobservable variables and measurement error. J. Mark. Res. 1981, 18, 39–50. [Google Scholar] [CrossRef]

- Schierz, P.G.; Schilke, O.; Wirtz, B.W. Understanding consumer acceptance of mobile payment services: An empirical analysis. Electron. Commer. Res. Appl. 2010, 9, 209–216. [Google Scholar] [CrossRef]

- Trütsch, T. The impact of mobile payment on payment choice. Financ. Mark. Portf. Manag. 2016, 30, 299–336. [Google Scholar] [CrossRef] [Green Version]

- Zhou, T. An empirical examination of continuance intention of mobile payment services. Decis. Support Syst. 2013, 54, 1085–1091. [Google Scholar] [CrossRef]

- Peráček, T. E-commerce and its limits in the context of consumer protection: The case of the Slovak Republic. Jurid. Trib. Trib. Jurid. 2022, 12, 35–50. [Google Scholar] [CrossRef]

- Žofčinová, V.; Čajková, A.; Král, R. Local leader and the labour law position in the context of the smart city concept through the optics of the EU. TalTech J. Eur. Stud. 2022, 12, 3–26. [Google Scholar] [CrossRef]

Figure 1.

Research conceptual model.

{kind=link}

Table 1.

Constructs and measurement items.

| Constructs | Measurement | Sources |

|---|---|---|

| Dissatisfaction | DIS1: I feel dissatisfied paying with cash because the change I receive often does not equal the amount I should have received. | [31,54] |

| DIS2: Compared to mobile payment, I feel dissatisfied with cash payment because it would not give me more exclusive time-bound offers | ||

| DIS3: I think the COVID-19 virus can be transmitted to humans from cash and coin. | ||

| DIS4: I feel dissatisfied with my overall experience using cash payment | ||

| Alternative attractiveness (AA) | AA1: There are good mobile payment provider options if I have to switch to mobile payment. | [25,55] |

| AA2: For me, the benefits of using mobile payment is higher than cash | ||

| AA3: I would probably be really pleased and happy with the functions and services of mobile payment | ||

| AA4: Using mobile payment may make me more satisfied and delighted than cash payment | ||

| Perceived Fear (PF) | PF1: The COVID-19 pandemic worries me. | [56,57] |

| PF2: I am afraid of being infected by COVID-19. | ||

| PF3: How likely do you think it is to get COVID-19 in general? | ||

| PF4: Overall, to what extent do you worry about COVID-19? | ||

| Switching Intention (SI) | SI1: I am thinking about switching from cash to mobile payment. | [58,59] |

| SI2: I would like to switch from cash to mobile payment in the future. | ||

| SI3: There is a high probability that I will switch from cash to mobile payment | ||

| SI4: I am ready to switch from cash to mobile payment. |

Table 2.

Results of the reliability and validity check.

| Constructs and Items | Loading | CR | AVE | Cronbach’s Alpha |

|---|---|---|---|---|

| Dissatisfaction | ||||

| DIS1 | 0.705 | 0.793 | 0.500 | 0.791 |

| DIS2 | 0.651 | |||

| DIS3 | 0.666 | |||

| DIS4 | 0.772 | |||

| Alternative attractiveness | ||||

| AA 1 | 0.621 | 0.825 | 0.544 | 0.824 |

| AA 2 | 0.819 | |||

| AA 3 | 0.804 | |||

| AA 4 | 0.689 | |||

| Perceived fear | ||||

| PF 1 | 0.890 | 0.794 | 0.502 | 0.81 |

| PF 2 | 0.765 | |||

| PF 3 | 0.592 | |||

| PF 4 | 0.528 | |||

| Switching intention | ||||

| SI 1 | 0.769 | 0.820 | 0.535 | 0.788 |

| SI 2 | 0.842 | |||

| SI 3 | 0.662 | |||

| SI 4 | 0.635 |

Table 3.

Correlations of constructs.

| Construct | Mean | SD | DIS | AA | PM | SI |

|---|---|---|---|---|---|---|

| Dissatisfaction | 3.527 | 0.702 | 1 | |||

| Alternative attractiveness | 3.371 | 0.730 | 0.491 | 1 | ||

| Perceived fear | 3.464 | 0.776 | 0.560 | 0.518 | 1 | |

| Switching intention | 3.595 | 0.702 | 0.590 | 0.448 | 0.753 | 1 |

Table 4.

Structural parameter estimates of the model.

| Paths | Estimates | t-Values | Results |

|---|---|---|---|

| H1: Dissatisfaction → Switching intention | 0.302 | 5.476 *** | Supported |

| H2: Alternative attractiveness → Switching intention | −0.008 | −0.164 | Not supported |

| H3: Perceived fear → Switching intention | 0.631 | 8.532 *** | Supported |

| H4: Dissatisfaction → Perceived fear | 0.394 | 6.44 *** | Supported |

| H5: Alternative attractiveness → Perceived fear | 0.320 | 5.714 *** | Supported |

*** Significant at p < 0.001.

Table 5.

Standardized direct and indirect effects.

| Paths | DIS | AA | PM | SI |

|---|---|---|---|---|

| Standardized total effects | ||||

| Perceived fear | 0.395 | 0.319 | - | - |

| Switching intention | 0.548 | 0.200 | 0.628 | - |

| Standardized direct effects | ||||

| Perceived fear | 0.395 | 0.319 | - | - |

| Switching intention | 0.300 | 0.628 | - | |

| Standardized indirect effects | ||||

| Perceived fear | - | - | - | - |

| Switching intention | 0.248 | 0.200 | - | - |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Yu, S.-Y.; Chen, D.C. Consumers’ Switching from Cash to Mobile Payment under the Fear of COVID-19 in Taiwan. Sustainability 2022, 14, 8489. https://doi.org/10.3390/su14148489

AMA Style

Yu S-Y, Chen DC. Consumers’ Switching from Cash to Mobile Payment under the Fear of COVID-19 in Taiwan. Sustainability. 2022; 14(14):8489. https://doi.org/10.3390/su14148489

Chicago/Turabian StyleYu, Shih-Yi, and Der Chao Chen. 2022. "Consumers’ Switching from Cash to Mobile Payment under the Fear of COVID-19 in Taiwan" Sustainability 14, no. 14: 8489. https://doi.org/10.3390/su14148489

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.