Bubble in Carbon Credits during COVID-19: Financial Instability or Positive Impact (“Minsky” or “Social”)?

Abstract

:1. Introduction

2. Literature Review

3. Data and Research Methodology

- KRBN (tracking IHS Markit Global Carbon),

- GRN (tracking Barclays Global Carbon II TR) and

- Solactive Carbon Emission Allowances Rolling Futures TR (SOLCARBT).

4. Empirical Results

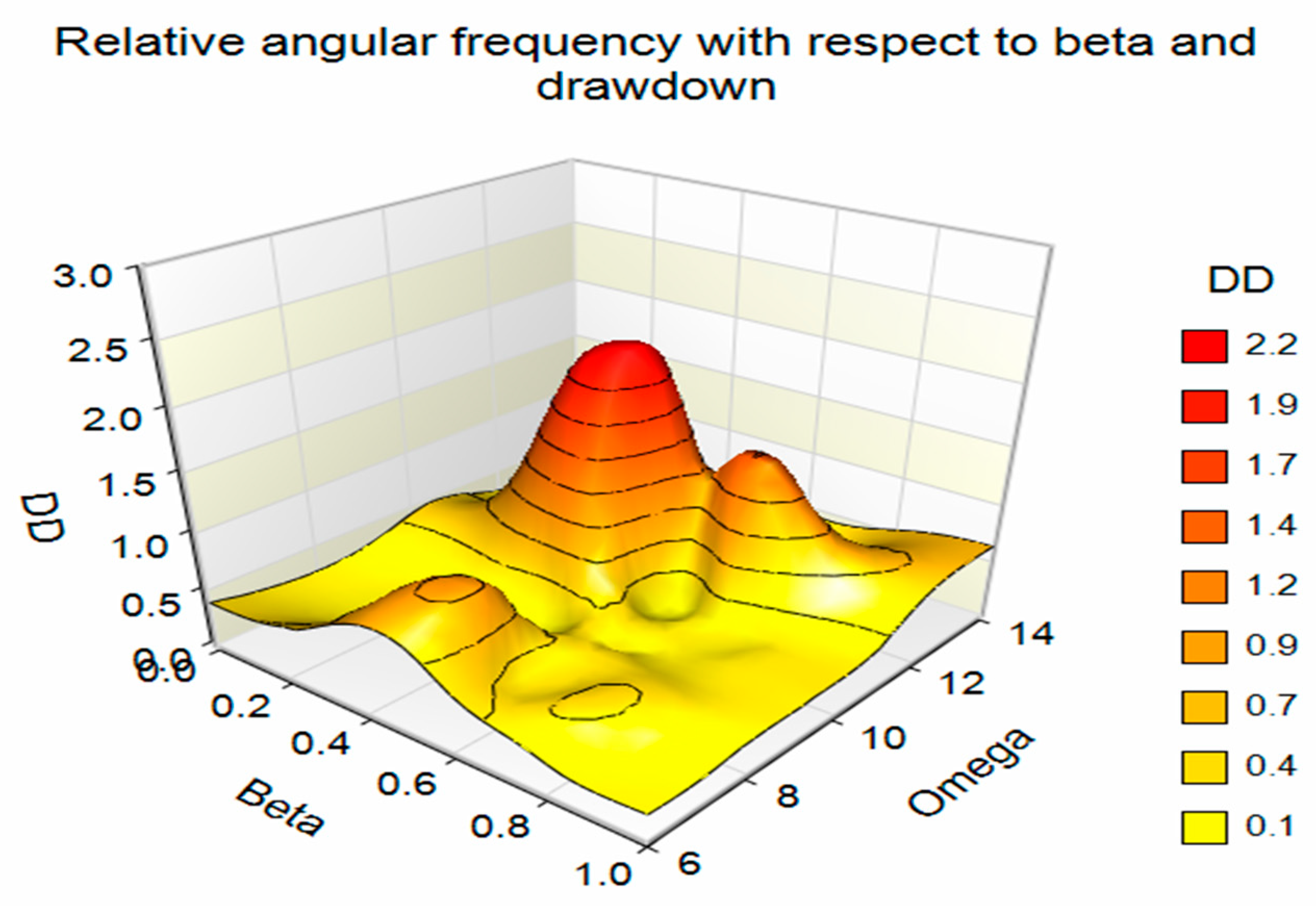

- β = 0.52 ± 0.38

- ω = 9.65 ± 3.39

- Minimum Drawdown (%) = 14%

- Average Drawdown (%) = 54%

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

| 1 | John Kerry Backs New Carbon-Price ETF in Climate Change Fight. Available online: https://www.bloomberg.com/news/articles/2020-07-30/john-kerry-backs-new-carbon-price-etf-in-climate-change-fight#xj4y7vzkg (accessed on 6 August 2022). |

| 2 | Niche asset nears mainstream as investors warm to EU carbon market. Available online: https://www.ft.com/content/4535374d-11ab-31aa-9908-b7c0ac2ee266 (accessed on 10 June 2022). |

| 3 | Carbon Pricing Dashboard. Available online: https://carbonpricingdashboard.worldbank.org/ (accessed on 10 June 2022). |

| 4 | Wall Street’s Favorite Climate Solution Is Mired in Disagreements. Available online: https://www.bloomberg.com/news/features/2021-06-02/carbon-offsets-new-100-billion-market-faces-disputes-over-trading-rules (accessed on 10 June 2022). |

| 5 | United Nations Climate Change (n.d.). Emissions Trading. Available online: https://unfccc.int/process/the-kyoto-protocol/mechanisms/emissions-trading (accessed on 10 June 2022). |

| 6 | World Bank (n.d.). What is Carbon Pricing? Available online: https://www.worldbank.org/en/programs/pricing-carbo. (accessed on 10 June 2022). |

| 7 | Refinitive. Carbon Market Year in Review 2020. 2021. Available online: https://www.refinitiv.com/content/dam/marketing/en_us/documents/reports/carbon-market-year-in-review-2020.pdf. (accessed on 10 June 2022). |

| 8 | Drawdown is the cumulative loss from one local maximum to the immediate next minimum; a size that is above the threshold ‘ε’. |

| 9 | Historical Drawdowns for Global Equity Portfolios. Available online: https://steadyoptions.com/articles/historical-drawdowns-for-global-equity-portfolios-r595/ (accessed on 10 June 2022). |

References

- Adrian, Tobias, Patrick Bolton, and Alissa M. Kleinnijenhuis. 2022. How Replacing Coal With Renewable Energy Could Pay For Itself. IMF Blog. June 8. Available online: https://blogs.imf.org/2022/06/08/how-replacing-coal-with-renewable-energy-could-pay-for-itself/ (accessed on 1 August 2022).

- Anjos, Miguel F., Felipe Feijoo, and Sriram Sankaranarayanan. 2022. A multinational carbon-credit market integrating distinct national carbon allowance strategies. Applied Energy 319: 119181. [Google Scholar] [CrossRef]

- Brée, David S., and Nathan Lael Joseph. 2013. Testing for financial crashes using the log periodic power law model. International Review of Financial Analysis 30: 287–97. [Google Scholar] [CrossRef]

- Christopoulos, Apostolos G., Spyros Papathanasiou, Petros Kalantonis, Andreas Chouliaras, and Savvas Katsikidis. 2014. An Investigation of cointegration and casualty relationships between the PIIGS’ stock markets. Stock Markets European Research Studies 17: 109–23. [Google Scholar] [CrossRef]

- Davidson, Paul. 2008. Is the Current Distress Caused by the Sub-Prime Mortgage Crisis a Minsky Moment? Or is it the Result of Attempting to Securitize Illiquid Non-Commercial Mortgage Loans. Journal of Post Keynesian Economics 30: 669–76. [Google Scholar] [CrossRef]

- Drozdz, S., F. Ruf, J. Speth, and M. ójcik. 1999. Imprints of log-periodic self-similarity in the stock market. The European Physical Journal B-Condensed Matter and Complex Systems 10: 589–93. [Google Scholar] [CrossRef]

- Filimonov, Vladimir, and Didier Sornette. 2013. A stable and robust calibration scheme of the log-periodic power law model. Physica A: Statistical Mechanics and Its Applications 392: 3698–707. [Google Scholar] [CrossRef]

- Frankel, Tamar. 2012. The Ponzi Scheme Puzzle: A History and Analysis of Con Artists and Victims. Oxford: Oxford University Press. [Google Scholar]

- Galbraith, James K., and Daniel Munevar Sastre. 2009. The Generalized Minsky Moment. London: Edward Elgar Publishing, Chapter 14. [Google Scholar]

- Garber, Peter M. 1990. Famous first bubbles. Journal of Economic Perspectives 4: 35–54. [Google Scholar] [CrossRef]

- Geuder, Julian, Harald Kinateder, and Niklas F. Wagner. 2019. Cryptocurrencies as financial bubbles: The case of Bitcoin. Finance Research Letters 31: 179–84. [Google Scholar] [CrossRef]

- Ghosh, Bikramaditya, Dimitris Kenourgios, Antony Francis, and Suman Bhattacharyya. 2020. How well the log periodic power law works in an emerging stock market? Applied Economics Letters 28: 1174–80. [Google Scholar] [CrossRef]

- Ghosh, Bikramaditya, Spyros Papathanasiou, and Vandana Gablani. 2022a. Are Policy Stances Consistent with the Global GHG Emission Persistence? In Applications in Energy Finance. Edited by C. Floros and I. Chatziantoniou. Cham: Palgrave Macmillan, pp. 255–79. [Google Scholar] [CrossRef]

- Ghosh, Bikramaditya, Spyros Papathanasiou, Nikita Ramchandani, and Dimitrios Kenourgios. 2021. Diagnosis and prediction of IIGPS’ countries bubble crashes during BREXIT. Mathematics 9: 1003. [Google Scholar] [CrossRef]

- Ghosh, Bikramaditya, Spyros Papathanasiou, Vandita Dar, and Dimitrios Kenourgios. 2022b. Deconstruction of the Green Bubble during COVID-19. International Evidence. Sustainability Special Issue: Creative Economy for Sustainable Development. 14: 3466. [Google Scholar] [CrossRef]

- Giorgis, Vincent, Tobias A. Huber, and Didier Sornette. 2021. Swiss Finance Institute Research Paper Series N ° 21–36. In Swiss Finance Institute Research Paper Series. Available online: https://deliverypdf.ssrn.com/delivery.php?ID=570005095083087107002003101079018104100051081067090053088024114105127020070074083070039012044061104010048121001124098091088121019053041013058006011002001090075031020022037105125083122074101021125097020021097069069114028117081081064082126111106004121&EXT=pdf&INDEX=TRUE (accessed on 16 August 2022).

- Gisler, Monika, Didier Sornette, and Ryan Woodard. 2011. Innovation as a social bubble: The example of the Human Genome Project. Research Policy 40: 1412–25. [Google Scholar] [CrossRef]

- Haken, Hermann. 1975. Generalized Ginzburg-Landau equations for phase transition-like phenomena in lasers, nonlinear optics, hydrodynamics and chemical reactions. Zeitschrift für Physik B Condensed Matter 21: 105–14. [Google Scholar] [CrossRef]

- Johansen, Anders. 2003. Characterization of large price variations in financial markets. Physica A: Statistical Mechanics and Its Applications 324: 157–66. [Google Scholar] [CrossRef]

- Johansen, Anders, and Didier Sornette. 2010. Shocks, crashes and bubbles in financial markets. Brussels Economic Review 53: 201–54. [Google Scholar]

- Johansen, Anders, Olivier Ledoit, and Didier Sornette. 2000. Crashes as critical points. International Journal of Theoretical and Applied Finance 3: 219–55. [Google Scholar] [CrossRef]

- Keen, Steve. 1995. Finance and economic breakdown: Modeling Minsky’s “financial instability hypothesis”. Journal of Post Keynesian Economics 17: 607–35. [Google Scholar] [CrossRef]

- Kenourgios, Dimitrios, Spyros Papathanasiou, and Anastasia Christina Bampili. 2021. On the predictive power of CAPE or Shiller’s PE ratio: The case of the Greek stock market. Operational Research, accepted. [Google Scholar] [CrossRef]

- Knuth, Sarah. 2018. Breakthroughs for a green economy? Financialization and clean energy transition. Energy Research & Social Science 41: 220–29. [Google Scholar] [CrossRef]

- Korzeniowski, Piotr, and Ireneusz Kuropka. 2013. Forecasting the Critical Points of Stock Markets’ Indices Using Log-Periodic Power Law. Ekonometria 1: 100–10. [Google Scholar]

- Koutsokostas, Drosos, Spyros Papathanasiou, and Dimitris Balios. 2019. Adjusting for risk factors in mutual fund performance and performance persistence. The Journal of Risk Finance 20: 352–69. [Google Scholar] [CrossRef]

- Koutsokostas, Drosos, Spyros Papathanasiou, and Nikolaos Eriotis. 2018. Can mutual fund managers predict security prices to beat the market? The case of Greece during the debt crisis. The Journal of Prediction Markets 12: 40–62. [Google Scholar] [CrossRef]

- Le, Thai-Ha, Ha-Chi Le, and Farhad Taghizadeh-Hesary. 2020. Does financial inclusion impact CO2 emissions? Evidence from Asia. Finance Research Letters 34: 101451. [Google Scholar] [CrossRef]

- Leal, Patrícia Alexandra, António Cardoso Marques, and José Alberto Fuinhas. 2019. Decoupling economic growth from GHG emissions: Decomposition analysis by sectoral factors for Australia. Economic Analysis and Policy 62: 12–26. [Google Scholar] [CrossRef]

- Li, Chong. 2017. Log-periodic view on critical dates of the Chinese stock market bubbles. Physica A: Statistical Mechanics and its Applications 465: 305–11. [Google Scholar] [CrossRef]

- Lin, Li, Ruo En Ren, and Didier Sornette. 2014. The volatility-confined LPPL model: A consistent model of “explosive” financial bubbles with mean-reverting residuals. International Review of Financial Analysis 33: 210–25. [Google Scholar] [CrossRef]

- Lohmann, Larry. 2008. Carbon trading, climate justice and the production of ignorance: Ten examples. Development 51: 359–65. [Google Scholar] [CrossRef]

- Lohmann, Larry. 2010. Neoliberalism and the Calculable World: The Rise of Carbon Trading. In Rise and Fall of Neoliberalism: The Collapse of an Economic Order? Edited by Kean Birch and Vlad Mykhnenko. London: Zed Books Ltd., pp. 77–93. [Google Scholar]

- Marcus, Alfred, Joel Malen, and Shmuel Ellis. 2013. The promise and pitfalls of venture capital as an asset class for clean energy investment: Research questions for organization and natural environment scholars. Organization & Environment 26: 31–60. [Google Scholar]

- Mathews, John A. 2008. How carbon credits could drive the emergence of renewable energies. Energy Policy 36: 3633–39. [Google Scholar] [CrossRef]

- Mathews, John A. 2013. The renewable energies technology surge: A new techno-economic paradigm in the making? Futures 46: 10–22. [Google Scholar] [CrossRef]

- Michaelowa, Axel, Igor Shishlov, and Dario Brescia. 2019. Evolution of international carbon markets: Lessons for the Paris Agreement. Wiley Interdisciplinary Reviews: Climate Change 10: e613. [Google Scholar] [CrossRef]

- Milner, M. 2007. “Global Carbon Trading Market Triples to £15 bn”: ExecReview. Available online: http://www.execreview.com/2007/05/global-carbon-trading-market-triples-to-15bn/ (accessed on 1 August 2022).

- Minsky, Hyman P. 1977. The financial instability hypothesis: An interpretation of Keynes and an alternative to “standard” theory. Challenge 20: 20–27. [Google Scholar] [CrossRef]

- Minsky, Hyman P. 2016. Can “It” Happen Again? London: Routledge. [Google Scholar]

- Palley, Thomas I. 2009. The Limits of Minsky’s Financial Instability Hypothesis as an Explanation of the Crisis (No. 11/2009). Düsseldorf: Hans-Böckler-Stiftung, Institut für Makroökonomie und Konjunkturforschung (IMK). Available online: http://hdl.handle.net/10419/105923 (accessed on 1 August 2022).

- Papathanasiou, Spyros, Dimitrios Vasiliou, Anastasios Magoutas, and Drosos Koutsokostas. 2021. Do Hedge and Merger Arbitrage Funds Actually Hedge? A Time-Varying Volatility Spillover Approach. Finance Research Letters 44: 102088. [Google Scholar] [CrossRef]

- Papathanasiou, Spyros, Ioannis Dokas, and Drosos Koutsokostas. 2022. Value investing versus other investment strategies: A volatility spillover approach and portfolio hedging strategies for investors. The North American Journal of Economics and Finance 62: 101764. [Google Scholar] [CrossRef]

- Pearse, Rebecca, and Steffen Böhm. 2014. Ten reasons why carbon markets will not bring about radical emissions reduction. Carbon Management 5: 325–337. [Google Scholar] [CrossRef]

- Quinn, William, and John D. Turner. 2020. Boom and Bust: A Global History of Financial Bubbles. Cambridge: Cambridge University Press. [Google Scholar]

- Ramirez-Contreras, Nidia Elizabeth, David Arturo Munar-Florez, Jesús Alberto Garcia-Nuñez, Mauricio Mosquera-Montoya, and André P. C. Faaij. 2020. The GHG emissions and economic performance of the Colombian palm oil sector; current status and long-term perspectives. Journal of Cleaner Production 258: 120757. [Google Scholar] [CrossRef]

- Ricke, Katharine, Laurent Drouet, Ken Caldeira, and Massimo Tavoni. 2018. Country-level social cost of carbon. Nature Climate Change 8: 895–900. [Google Scholar] [CrossRef]

- Sahu, Santosh Kumar, and Unmesh Patnaik. 2020. The tradeoffs between GHGs emissions, income inequality and productivity. Energy and Climate Change 1: 100014. [Google Scholar] [CrossRef]

- Samitas, Aristeidis, Spyros Papathanasiou, Drosos Koutsokostas, and Elias Kampouris. 2022a. Are Timber and Water Investments Safe-Havens? A Volatility Spillover Approach and Portfolio Hedging Strategies for Investors. Finance Research Letters 47: 102657. [Google Scholar] [CrossRef]

- Samitas, Aristeidis, Spyros Papathanasiou, Drosos Koutsokostas, and Elias Kampouris. 2022b. Volatility spillovers between fine wine and major global markets during COVID -19: A portfolio hedging strategy for investors. International Review of Economics & Finance 78: 629–42. [Google Scholar] [CrossRef]

- Sornette, Didier, and Anders Johansen. 1998. A hierarchical model of financial crashes. Physica A: Statistical Mechanics and its Applications 261: 581–98. [Google Scholar] [CrossRef]

- Sornette, Didier, Anders Johansen, and Jean-Philippe Bouchaud. 1996. Stock market crashes, precursors and replicas. Journal de Physique I 6: 167–75. [Google Scholar] [CrossRef]

- Umar, Zaghum, Dimitris Kenourgios, and Sypros Papathanasiou. 2020. The static and dynamic connectedness of environmental, social, and governance investments: International evidence. Economic Modelling 93: 112–24. [Google Scholar] [CrossRef] [PubMed]

- Vliamos, Spyros, and Konstantinos Gravas. 2018. The International Financial System and the Role of Central Banks in the Great 2007–9 Recession and the ‘Monetary Peace’. In Institutionalist Perspectives on Development. Palgrave Studies in Democracy. Innovation, and Entrepreneurship for Growth. Edited by S. Vliamos and M. Zouboulakis. Cham: Palgrave Macmillan. [Google Scholar] [CrossRef]

- Wątorek, Marcin, Stanisław Drożdż, and Paweł Oświęcimka. 2016. World financial 2014–2016 market bubbles: Oil negative-US dollar positive. Acta Physica Polonica A 129: 932–36. [Google Scholar] [CrossRef]

- Wheatley, Spencer, Didier Sornette, Tobias Huber, Max Reppen, and Robert N. Gantner. 2019. Are Bitcoin bubbles predictable? Combining a generalized Metcalfe’s law and the log-periodic power law singularity model. Royal Society Open Science 6: 180538. [Google Scholar] [CrossRef] [PubMed]

- Woo, Junghoon, Ridah Fatima, Charles J.Kibert, Richard E.Newman, Yifeng Tian, and Ravi S.Srinivasan. 2021. Applying blockchain technology for building energy performance measurement, reporting, and verification (MRV) and the carbon credit market: A review of the literature. Building and Environment 205: 108199. [Google Scholar] [CrossRef]

- Wu, Tiankuang Tim. 2012. Critical Phenomena with Renormalization Group Analysis of a Hierarchical Model of Financial Crashes [Simon Fraser University]. In ProQuest Dissertations and Theses. Available online: http://login.proxy.library.vanderbilt.edu/login?url=http://search.proquest.com/docview/1515738661?accountid=14816%5Cnhttp://sfx.library.vanderbilt.edu/vu?url_ver=Z39.88-2004&rft_val_fmt=info:ofi/fmt:kev:mtx:dissertation&genre=dissertations+%26+theses&sid= (accessed on 1 August 2022).

- Zhang, Yinpeng, Zhixin Liu, and Xueying Yu. 2017. The diversification benefits of including carbon assets in financial portfolios. Sustainability 9: 437. [Google Scholar] [CrossRef]

- Zhou, Wei, Yang Huang, and Jin Chen. 2018. The bubble and anti-bubble risk resistance analysis on the metal futures in China. Physica A: Statistical Mechanics and Its Applications 503: 947–57. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Parameter | Constraint | Literature |

|---|---|---|

| A | (>0) | Korzeniowski and Kuropka (2013) |

| B | (<0) | Lin et al. (2014) |

| C1 | (Cos function) | Filimonov and Sornette (2013) |

| C2 | (Sine function) | Filimonov and Sornette (2013) |

| tc | (t to ∞) | Korzeniowski and Kuropka (2013) |

| Β | (0.1 to 0.9) | Lin et al. (2014) |

| Ω | (4.8 to 13) | Johansen (2003) |

| Corporate/ | Bubble | Time | tc | A | B | C1 | C2 | β | ω | DD (%) |

|---|---|---|---|---|---|---|---|---|---|---|

| Index | ||||||||||

| KRBN | B1 | 2 November 2020 to 17 December 2020 | 33 | 3.30 | −0.01 | 0.00 | 0.00 | 0.86 | 9.92 | 28% |

| B2 | 15 January 2021 to 16 February 2021 | 26 | 3.51 | −7.77 | 0.00 | 0.00 | 0.88 | 6.76 | 19% | |

| B3 | 17 March 2021 to 14 May 2021 | 52 | 3.59 | −0.03 | −0.02 | −0.01 | 0.63 | 7.46 | 32% | |

| B4 | 19 May 2021 to 5 July 2021 | 32 | 3.57 | 0.00 | 0.01 | 0.01 | 0.41 | 8.83 | 14% | |

| B5 | 22 July 2021 to 25 October 2021 | 70 | 3.73 | 0.00 | 0.00 | 0.00 | 0.17 | 12.72 | 25% | |

| GRN | B1 | 8 October 2019 to 20 December 2019 | 54 | 3.94 | −5.53 | 5.53 | 0.05 | 0.23 | 8.24 | 19% |

| B2 | 11March 2020 to 9 April 2020 | 22 | 3.83 | −0.11 | −0.01 | −0.05 | 0.78 | 7.19 | 42% | |

| B3 | 4 May 2020 to 9 June 2021 | 310 | 3.19 | −0.02 | −0.01 | 0.00 | 0.45 | 10.98 | 220% | |

| B4 | 11 June 2021 to 1 August 2021 | 68 | 3.26 | −0.01 | 0.00 | 0.00 | 0.75 | 10.17 | 23% | |

| B5 | 19 October 2021 to 11 November 2021 | 20 | 3.37 | −0.12 | −0.01 | 0.01 | 0.58 | 10.68 | 15% | |

| SOLCARBT | B1 | 18 March 2020 to 14 July 2020 | 89 | 4.91 | −0.13 | 0.01 | 0.01 | 0.47 | 7.26 | 93% |

| B2 | 28 October 2020 to 14 May 2021 | 131 | 5.29 | −0.02 | 0.00 | 0.00 | 0.66 | 11.79 | 143% | |

| B3 | 23 July 2021 to 5 October 2021 | 59 | 5.72 | 0.00 | 0.00 | 0.00 | 0.65 | 12.68 | 27% |

| Sr. No. | Critical Date | Drawdown | Company/Index | Events |

|---|---|---|---|---|

| 1 | 9 June 21 | 220% | GRN | Mark Carney, a former governor of the Bank of England, and Bill Winters, the chief executive of Standard Chartered have set up a task force to finalize recommendations for smaller and more permanent governance in this new carbon-offset market. |

| 2 | 14 May 21 | 143% | SOLCARBT | Climate Action Tracker estimated that climate policies implemented across the world at present, including the effect of the pandemic, will lead to a temperature rise of 2.9 °C by the end of the century |

| 3 | 14 July 20 | 93% | SOLCARBT | According to Directive 2003/87/EC, the EU ETS covers emissions from all stationary installations in EU Member States. However, emissions from stationary installations in the United Kingdom are no longer within the scope of the Union law and the EU ETS. |

| 4 | 17 April 20 | 42% | GRN | As of April 2020, Denmark, France, New Zealand, Sweden, and the UK have built on this commitment and enshrined in law a net zero CO2 emissions target into legislation, while Suriname and Bhutan are already carbon negative. In addition, 15 subnational regions, 398 cities, 786 businesses, and 16 investors have also indicated that they are working toward achieving net zero emission targets. |

| 5 | 14 May 21 | 32% | KRBN | Climate Action Tracker estimated that climate policies implemented across the world at present, including the effect of the pandemic, will lead to a temperature rise of 2.9 °C by the end of the century. |

| 6 | 17 December 20 | 28% | KRBN | More than 8.6 million future vintage allowances, cleared at $17.35/tonne as entities, could buy state-owned allowances before the end of the current compliance period. |

| 7 | 8 November 21 | 25% | KRBN | A spokesperson for Bezos’ $10 billion “Bezos Earth Fund” told The Independent that the Amazon founder also “offsets all carbon emissions from his flights”. In his 2021 book, “How to Avoid a Climate Disaster”, Gates writes that he counteracts his non-aviation emissions by “buying offsets through a company that runs a facility that removes carbon dioxide from the air”. |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ghosh, B.; Papathanasiou, S.; Dar, V.; Gravas, K. Bubble in Carbon Credits during COVID-19: Financial Instability or Positive Impact (“Minsky” or “Social”)? J. Risk Financial Manag. 2022, 15, 367. https://doi.org/10.3390/jrfm15080367

Ghosh B, Papathanasiou S, Dar V, Gravas K. Bubble in Carbon Credits during COVID-19: Financial Instability or Positive Impact (“Minsky” or “Social”)? Journal of Risk and Financial Management. 2022; 15(8):367. https://doi.org/10.3390/jrfm15080367

Chicago/Turabian StyleGhosh, Bikramaditya, Spyros Papathanasiou, Vandita Dar, and Konstantinos Gravas. 2022. "Bubble in Carbon Credits during COVID-19: Financial Instability or Positive Impact (“Minsky” or “Social”)?" Journal of Risk and Financial Management 15, no. 8: 367. https://doi.org/10.3390/jrfm15080367