COVID-19 Pandemic and Investor Herding in International Stock Markets

1

School of Business, Lebanese American University, Jbeil P.O. Box 36, Lebanon

2

Department of Economics and Finance, Southern Illinois University Edwardsville, Edwardsville, IL 62026, USA

3

Department of Economics, University of Pretoria, Pretoria 0002, South Africa

*

Authors to whom correspondence should be addressed.

Risks 2021, 9(9), 168; https://doi.org/10.3390/risks9090168

Submission received: 23 July 2021

/

Revised: 25 August 2021

/

Accepted: 8 September 2021

/

Published: 13 September 2021

(This article belongs to the Special Issue Mathematical and Statistical Models on Risk with applications in Business, Economics, Finance, and COVID-19)

Abstract

:The aim of this study is to understand the effect of the recent novel coronavirus pandemic on investor herding behavior in global stock markets. Utilizing a daily newspaper-based index of financial uncertainty associated with infectious diseases, we examine the association between pandemic-induced market uncertainty and herding behavior in a set of 49 global stock markets. More specifically, we study the pattern of cross-sectional market behavior and examine whether the pandemic-induced uncertainty drives directional similarity across the global stock markets that cannot be explained by the standard asset pricing models. Utilizing a time-varying variation of the static herding model, we first identify periods during which herding is detected. We then employ probit models to examine the possible association between pandemic-induced uncertainty and the formation of herding. Our findings show a strong association between herd formation in stock markets and COVID-19 induced market uncertainty. The herding effect of COVID-19 induced market uncertainty is particularly strong for emerging stock markets as well as European PIIGS stock markets that include some of the hardest hit economies in Europe by the pandemic. The findings establish a direct link between the recent pandemic and herd formation among market participants in global financial markets. Considering the evidence that herding behavior can drive security prices away from equilibrium values supported by fundamentals and further contribute to price fluctuations in financial markets, our findings have significant implications for policy makers and investors in their efforts to monitor investor sentiment and mitigate mis-valuations that might occur as a result. Furthermore, the evidence on the behavioral pattern of stock investors in relation to infectious diseases uncertainty can be useful in studying price discovery in stock markets and might help market participants in forming hedging strategies to mitigate downside risk in their investment portfolios.

1. Introduction

Herding behavior has been shown to exacerbate price fluctuations and drive pricing inefficiencies in financial markets (e.g., Bikhchandani and Sharma 2001; Blasco et al. 2012; Alhaj-Yaseen and Yau 2018; Demirer et al. 2019). Irrespective of the nature of such behavior among investors, rational or otherwise, the literature generally suggests that herding is more prevalent during periods of market stress or heightened uncertainty. Although a large number of studies have examined the presence of herding behavior in financial markets from different angles and using a wide range of samples (e.g., see Uwilingiye et al. 2019 for a recent review), the literature has not yet examined the role of the recent COVID-19 pandemic in this context as a driver of herding behavior among market participants. Given that the recent COVID-19 pandemic has triggered a massive spike in uncertainty, quickly transitioning from a healthcare crisis into an economic one, this paper examines the role of the pandemic as a driver of investor herding in international stock markets by utilizing a daily newspaper-based index of financial uncertainty associated with infectious diseases, recently developed by Baker et al. (2020).

The literature offers several arguments regarding the emergence of herd behavior among market participants. Devenow and Welch (1996) argue that investors feel a sense of security in following the crowd, particularly during periods of heightened uncertainty. Froot et al. (1992) argue that information acquisition costs play a role in why some investors may tend to mimic others, especially when such costs are high for certain traders. Other arguments that are proposed to explain why investors herd include the emergence of informational cascades (Banerjee 1992); managers’ tendency to avoid reputation (or compensation) related costs (Maug and Naik 1996); and the self-reinforcing nature of confidence in the majority opinion (Teraji 2003). Whatever the underlying factor that drives herd behavior might be, there is ample evidence that associates herding with excessive volatility in financial markets (e.g., Blasco et al. 2012; Demirer et al. 2019), posing serious challenges for investors when it comes to the pricing of assets as well as managing financial risks. Considering the evidence by Balcilar et al. (2014) that market volatility is the primary factor governing switches between herding and anti-herding states, the recently established newspaper-based index of financial uncertainty associated with infectious diseases, developed by Baker et al. (2020), offers an interesting opening to examine the role of COVID-19 induced market volatility over herding formation in global stock markets.

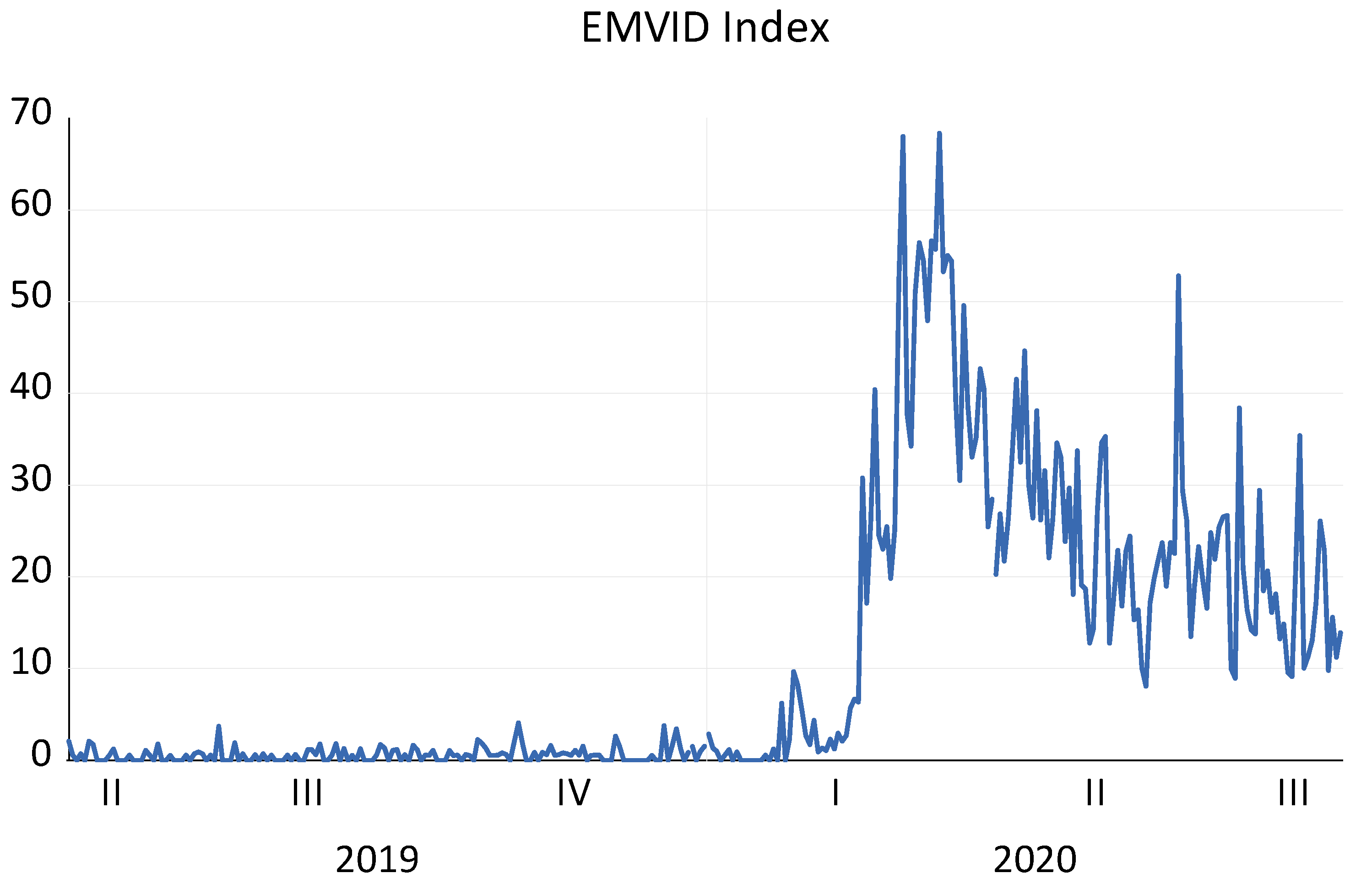

The earlier literature has already established the role of time-varying disaster risks as a factor that can explain the high excess returns and volatility observed in stock markets via its effects on investment growth or consumption patterns (e.g., Barro and Ursúa 2012; Gourio 2012; Wachter 2013, among others). Clearly, the probability and size of disasters lead to a great deal of uncertainty, which in turn can contribute to cash flow as well as discount rate shocks in stock valuations. However, quantifying the uncertainty related to such risks has been a challenge in most studies as it is often hard to distinguish between disaster induced uncertainty from the component of uncertainty that is driven by non-disaster related factors. To that end, the recently developed newspaper-based index of Baker et al. (2020), which tracks equity market volatility (EMV), in particular the movements in the Chicago Board Options Exchange (CBOE)’s Volatility Index (VIX), due to infectious diseases, provides an interesting opening. This index, presented in Figure 1, highlights the massive increase in uncertainty due to the pandemic over the recent months. The availability of this index at a daily frequency further allows us to examine the possible link between time-varying herding in stock markets and pandemic induced market uncertainty from a novel perspective. To the best of our knowledge, ours is the first study to examine herding behaviour in international stock market in this context.

Our analysis is related to a growing literature that establishes a link between the COVID-19 pandemic and increased volatility and uncertainty in financial markets (Akhtaruzzaman et al. 2020; Alexakis et al. 2021; Bouri et al. 2020; Fernandez-Perez et al. 2020; Goodell 2020; Sharif et al. 2020; Haldar and Sethi 2020; Milcheva 2021; Ozkan 2021; Salisu et al. 2021; Scherf et al. 2021). The general theme in this emerging strand of the literature is that the pandemic has led to increased uncertainty regarding economic fundamentals, which in turn has led to a significant dip in financial markets driven by the greater risk premium required on risky assets. However, the effect of the lockdown restrictions due to the pandemic has been rather heterogeneous across the global markets (Scherf et al. 2021), while Ozkan (2021) documents differences in departures from market efficiency due to the pandemic across the global markets. Given this, an interesting question is whether or not such heterogeneity in how global financial markets respond to the pandemic is in part driven by herding (or anti-herding) behavior. To that end, the cross-sectional statistic that we use in our herding tests offers a perfect tool as the testing methodology focuses on the cross-sectional behavior of stock markets and builds the herding test based on the cross-sectional patterns. Considering the evidence of heightened uncertainty due to the pandemic and the evidence that establishes a link between speculative or irrational behavior of market participants (e.g., De Long et al. 1990; Froot and Obstfeld 1991; and Hey and Morone 2004, among others), this paper provides new insight to the role of pandemic driven uncertainty over investor behavior.

Our findings indicate a strong association between herd formation in stock markets and COVID-19 induced financial market uncertainty. The herding effect of COVID-19 driven uncertainty is particularly strong for emerging stock markets as well as European PIIGS stock markets that include some of the hardest hit economies in Europe by the pandemic. Overall, the findings establish a direct link between the recent pandemic and investor behavior in financial markets, which has not been previously revealed. Considering the evidence that herding behavior can drive security prices away from equilibrium values supported by fundamentals and further contribute to price fluctuations in financial markets (e.g., Bikhchandani et al. (1992); Nofsinger and Sias (1999); and Blasco et al. (2012), our findings have significant implications for policy makers and investors in their efforts to monitor investor sentiment and mitigate mis-valuations that might occur as a result. Furthermore, the evidence on the behavioral pattern of stock investors in relation to infectious diseases uncertainty can be useful in studying price discovery in stock markets and might help market participants in forming hedging strategies to mitigate downside risk in their investment portfolios.

2. Data and Testing Methodology

2.1. Data

We utilize daily data for Morgan Stanley Capital International (MSCI) indexes in US Dollars for 49 individual countries and the overall MSCI World index over the period of 1 January 2019 to 10 August 2020. The source of our data is DataStream of Thomson Reuters. Besides examining all countries together as a group, we examine herd formation across various country groups based on the suggestion by Bikhchandani and Sharma (2001) that herd formation would be more likely to occur at the level of investments with similar characteristics where investors face similar decision problems. For this purpose, we sort the countries into advanced and emerging country groups based on the MSCI country classification1. We further explore herding within a group of major commodity exporters (Canada, Norway, Australia, New Zealand and Chile), BRICS nations (Brazil, Russia, India, China and South Africa) and PIIGS (Portugal, Ireland, Italy, Greece and Spain) in order to account for the similarity in economic fundamentals as well as the investment allocations maintained by global investment funds.

Since the focus of our analysis is to check for the presence of herding over the ongoing COVID-19 period, we split the data into equal number of observations (i.e., 159 data points) from 23 May 2019 to 31 December 2019 and 1 January 2020 to 10 August 2020 to account for possible structural breaks in herding patterns before and during the outbreak of the Coronavirus. Further, to study the possibility of time-varying herding, we conduct a time-varying estimation of our model (which we discuss below), with the period of 1 January 2019 to 22 May 2019 used as the size of the rolling window, i.e., 102 observation. Understandably, this ensures that we are able to analyze the evolution of the herding coefficient estimates over equal periods before and during the ongoing pandemic.

2.2. Testing Methodology

Some of the pioneering works in the strand of the literature that deals with herding tests in financial markets include Christie and Huang (1995) and Chang et al. (2000) who propose a return dispersion-based methodology to detect herding2. These herding tests focus on the cross-sectional behavior of asset returns within portfolios that include assets of similar characteristics. Following Chang et al. (2000), we use the cross-sectional absolute standard deviations (CSAD) across country returns (and the various categorizations) and examine the non-linear relation between the level of return dispersion and the aggregate market return, as captured by the MSCI World index3. The CSAD statistic, used as a measure of return dispersion, is formulated as follows:

where Ri,t and Rm,t is the log-returns on stock index of a specific country i and the overall index for period t, respectively; N is the number of stock indexes in the portfolio at time t4.

Chang et al. (2000) suggest that during periods of market stress, one would expect return dispersion (CSADt) and the aggregate market return (Rm,t) to have a nonlinear relationship such that herding, if present, would yield lower dispersion across country returns during large aggregate market fluctuations. Following the argument by Christie and Huang (1995) that the probability of herd formation is greater during periods of market stress and large price movements, the benchmark model is formulated based on the following quadratic model of return dispersion and market return:

The presence of herding then is tested via the following hypotheses:

Hypothesis 1 (H1).

In the absence of herding effects, we expect in Equation (2) that α1 > 0 and α2 = 0.

Hypothesis 2 (H2).

If herding behavior exists, we expect α2 < 0.

Hypothesis 3 (H3).

If anti-herding behavior exists, we expect α2 > 0.

The return-dispersion based herding test has been applied to different contexts in a large number of studies in the literature (e.g., Gleason et al. 2004; Demirer and Kutan 2006; Chiang and Zheng 2010; Balcilar and Demirer 2015; Balcilar et al. 2017; Babalos and Stavroyiannis 2015; Cakan et al. 2019 and more recently, Sibande et al. (2021). Despite the large number of studies in different contexts, however, the literature has largely focused on detecting herding without delving into the underlying drivers of such behavior. To the best of our knowledge, ours is the first study to examine herding in the context of pandemic-induced uncertainty. As noted earlier, given the dynamic nature of possible herding formation, we utilize a time-varying approach via rolling regressions of the model in Equation (2).

3. Empirical Findings

The results from the static model in Equation (2) are reported in Table 1 for the full-sample, i.e., 23 May 2019 to 10 August 2020, and pre- and during COVID-19 periods. As indicated by the non-negative estimates for the herding coefficient (α2), the static dispersion model yields no evidence of herding across any of the country groups. If anything, when significance holds particularly for the full sample, the results indicate the presence of anti-herding behavior across all the markets and the various categorizations, implied by the positive and significant α2 estimates. The finding of anti-herding for full sample in the static model is in fact consistent with the observation by Scherf et al. (2021) that the lockdown restrictions due to the pandemic has been rather heterogeneous across the global markets as well as the finding by Ozkan (2021) of differences in departures from market efficiency due to the pandemic across the global markets. It can thus be argued that the finding of anti-herding in the full sample is driven by the heterogeneity in how global financial markets responded to the pandemic as such heterogeneity in global markets would lead to greater dispersion in the cross-sectional behavior of global returns.

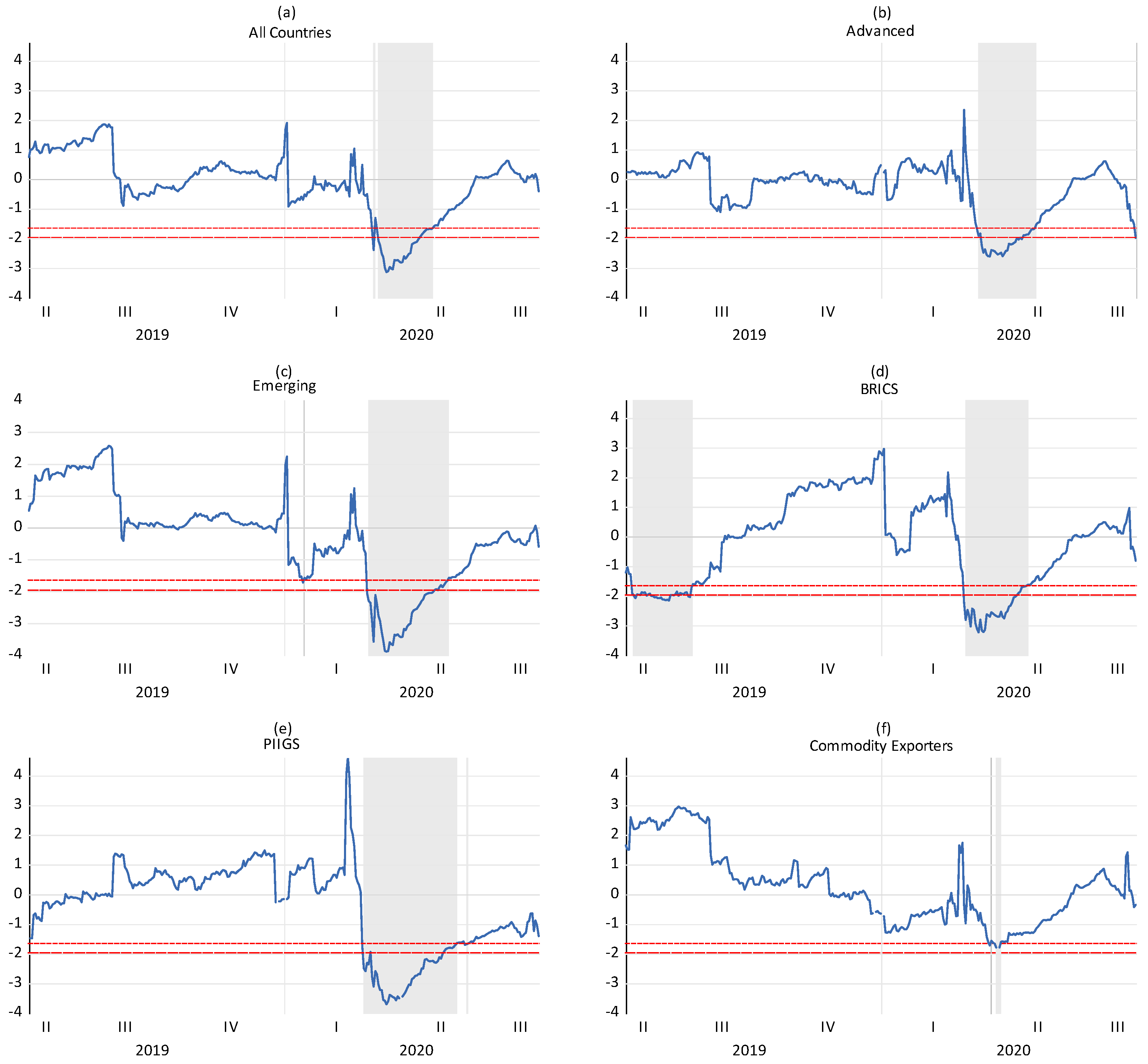

Balcilar et al. (2013), however, argue that the static model in Equation (2) leads to misleading conclusions regarding the presence of herd behavior as parameters in this specification are assumed to be constant over time. In fact, in a subsequent study, Balcilar et al. (2014) observe that the market often switches between herding and anti-herding states and that market volatility is the primary factor governing those switches. Given this and considering that investor behavior can be characterized to be dynamic and time-varying, depending on the market conditions, we resort to a rolling-window approach following Stavroyiannis and Babalos (2017). Figure 2 reports the evolution of the t-statistics for the herding coefficient in Equation (2) across the various country groups over the full sample period of 23 May 2019 to 10 August 2020. Understandably for herding, we are looking to identify periods for which the t-statistics are significantly negative, i.e., less than or equal to −1.645 and −1.96 corresponding to the 10% and 5% levels of significance. These two significance levels are selected in order to examine the findings at high and low levels of herding indicated by the significance of the herding coefficients obtained from the herding model in Equation (2). This setting allows us to relate periods of strong and weak herding, indicated by the significance of the estimated herding coefficients, to pandemic-induced uncertainty captured by the EMVID series.

Indeed, as seen in Figure 2, we are able to detect some evidence of herding primarily during the period that corresponds to the COVID-19 outbreak. More specifically, periods during which herding is detected are found as follows: all countries: 17 March 2020–7 May 2020; advanced: 24 March 2020–13 May 2020; emerging: 16 June 2020–10 August 2020 (besides some intermittent episodes in 2019 and early 2020); BRICS: 28 May 2019–18 July 2019, and 12 March 2020–6 May 2020; PIIGS: 9 March 2020–8 June 2020, and; commodity exporters: 3 April 2020–13 April 2020 (only at the 10% level of significance)5. The above evidence thus suggests that herding in the stock markets is a short-lived phenomenon induced by the instantaneous and dynamic behavior of investors. The observed patterns in each country group also support the findings in Balcilar et al. (2013, 2014) that the market often switches between herding and anti-herding states and herding is more prevalent during volatile market periods, underscoring the tendency of investors to feel a sense of security in the majority opinion during periods of uncertainty6.

Having detected episodes of herding formation across various international stock market classifications, a crucial question to ask is whether or not we can formally associate significant herding behavior over these periods with the outbreak of the COVID-19 pandemic. For this purpose, we resort to a probit model. We first define two dummy variables: D1 and D2 (also plotted in Figure 2), which take the value of unity during periods of statistically significant herding at 10% and 5% levels of significance respectively, i.e., for days in Figure 2 when the rolling t-statistic on α2 ≤ −1.645 and α2 ≤ −1.96 and zero otherwise. As mentioned earlier, these two levels of significance are used to identify periods of relatively weak (at 10% level of significance) and strong (at 5% level of significance) herding. Since D1 is more frequent than D2, it has a higher mean value, as can be seen from Table A1 reported in the Appendix A of the paper, which includes the summary statistics of the various dummy variables associated with herding of the country groups.

Then, we use a probit model to relate this dummy with the infectious disease equity market volatility (EMV) tracker, which has been recently constructed by Baker et al. (2020) as a newspaper-based index available at the daily frequency from January 19857. This index is based on textual analysis of four sets of terms namely, E: economic, economy, financial; M: “stock market”, equity, equities, “Standard and Poors”; V: volatility, volatile, uncertain, uncertainty, risk, risky; ID: epidemic, pandemic, virus, flu, disease, coronavirus, mers, sars, ebola, H5N1, H1N1, and then obtain daily counts of newspaper articles that contain at least one term in each of E, M, V, and ID across approximately 3000 US newspapers. The raw EMVID count is scaled by the count of all articles in the same day, and finally, Baker et al. (2020) multiplicatively rescale the resulting series to match the level of the VIX, by using the overall EMV index, and then scaling the EMVID index to reflect the ratio of the EMVID articles to total EMV articles. The EMVID index, presented in Figure 1 over the rolling-window estimation period of 23 May 2019 to 10 August 2020 clearly highlights the spikes (peaking in March of 2020) associated with the impact of the COVID-19 outbreak on financial market uncertainty.

The probit model to relate the occurrence of herding formation to the pandemic induced uncertainty index is formulated as follows: Pr(Di = 1|X) = Φ(β0 + β1EMVID) where, i = 1, 2; Pr denotes probability, and Φ is the cumulative distribution function (CDF) of the standard normal distribution, with the parameters β0 and β1 estimated by maximum likelihood. As can be clearly seen in Table 2, we observe that the EMVID index has a positive and significant effect, consistently in all country groups examined. The positive and significant β1 estimates reported in Table 2 suggest that the pandemic induced financial market uncertainty increases the probability of herding, in a statistically significant manner at least at the 5% level. The observed positive association between pandemic induced uncertainty and herd formation is found to be robust to the significance level that we use to detect herding, i.e., irrespective of whether we use D1 or D2 to capture periods of significant herd formation. In other words, the results reported in Table 2 clearly show that EMVID tends to drive herding in global equity markets, as well as in the different sub-groups examined. Interestingly, the strongest pandemic effect on herding formation is observed for emerging stock markets as well as the PIIGS countries that include some of the hardest hit European countries by COVID-19 like Italy and Spain. The strong pandemic effect over investor behavior in these sub-groups indeed supports the psychology-based argument offered by Devenow and Welch (1996) where following the market consensus induces a sense of security among less informed traders. Considering that developing markets, that are often plagued with institutional inefficiencies and informational asymmetries, the findings support the presence of information-driven motives behind herding behavior as the actions of more informed traders reveal valuable information to investors who have limited access to information (e.g., Avery and Zemsky 1998; Shleifer and Summers 1990; Froot et al. 1992; and Chari and Kehoe 2004).

The findings, overall, establish a clear association between pandemic induced financial market uncertainty and herd formation in international stock markets. Evidence on such association extends our limited understanding on the effect of COVID-19 pandemic on investor behavior in international stock markets, which is somewhat comparable to previous findings (e.g., Gleason et al. 2004) that point to a relationship between herding and highly volatile markets. In our case, the EMVID index reflects investor sentiment and the high level of this newspaper-based index of uncertainty associated with infectious diseases captures the fear of investors. Under such disaster risks, investors seek for confirmation, leading to significant herding.

4. Conclusions

This study examines the effect of the recent novel coronavirus pandemic on investor herding behavior in global stock markets by utilizing the recently developed newspaper-based index of Baker et al. (2020), which tracks equity market volatility (EMV), in particular the movements in the Chicago Board Options Exchange (CBOE)’s Volatility Index (VIX), due to infectious diseases. Utilizing a combination of rolling window regressions and probit analysis, applied to daily return data for 49 international stock markets, we document strong association between herd formation in global stock markets and COVID-19 induced financial market uncertainty. The herding effect of COVID-19 driven uncertainty is particularly strong for emerging stock markets and the European PIIGS stock markets that include some of the hardest hit economies in Europe by the pandemic. This finding suggests that herding depends on the development status of the economy under study. Notably, our findings establish a direct link between the recent novel coronavirus pandemic and investor behavior in financial markets, highlighting the role of disaster risks such as COVID-19 as a potential driver of behavioral patterns in financial markets.

The implications of the above findings matter to both regulators and investors as they confront them with challenges. In fact, the existence of herding behavior might jeopardize market efficiency and limits the possibility of diversification. Considering the evidence that herding behavior can drive security prices away from equilibrium values supported by fundamentals and further contribute to price fluctuations in financial markets (e.g., Bikhchandani et al. (1992), Nofsinger and Sias (1999) and Blasco et al. (2012)), our findings present challenges for policy makers and investors in their efforts to monitor investor sentiment and mitigate mis-valuations that might occur as a result. From a practical perspective, the evidence on the behavioral pattern of stock investors in relation to infectious diseases uncertainty can be useful in studying price discovery in stock markets and might help market participants in forming hedging strategies to mitigate downside risk in their investment portfolios. From an asset pricing perspective, our findings suggest that investment sentiment indicators could be useful in volatility forecasting as well as the valuation of derivative contracts. For future research, it would be interesting to examine whether or not these behavioral patterns contribute to volatility jumps as well as jump induced risk premia in asset prices.

Author Contributions

Conceptualization, R.G.; methodology, R.G. and R.D.; formal analysis, J.N. and R.G.; data curation, E.B.; writing—original draft preparation, R.G., E.B., R.D. and J.N.; writing—review and editing, R.G., R.D., J.N.; project administration, R.G. and R.D.. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no specific grant from any funding agency in the public, commercial, or not-for-profit sectors.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Data will be available from the authors upon request.

Acknowledgments

We would like to thank three anonymous referees for many helpful comments. Any remaining errors are solely ours.

Conflicts of Interest

The authors declare that they have no competing interest.

| 1 | Stock market classifications by MSCI are available at https://www.msci.com/market-classification (accessed on 11 August 2020) |

| 2 | Demirer et al. (2010) provide a review of the different testing methodologies based on return dispersion. |

| 3 | We also repeat our analysis by computing the cross-sectional standard deviation (CSSDt =

) statistic instead of CSAD. We obtained qualitatively, as well as quantitatively similar results, which are available upon request from the authors. |

| 4 | Since data is available for all the countries before 1 January of 2019, note we do not lose any observation while computing log-returns used in our model. |

| 5 | As suggested by an anonymous referee, we also conducted the rolling-window analysis by starting from 2018, and found our results to be similar not only qualitatively, but also quantitatively. Complete details of these results are available upon request from the authors. |

| 6 | Based on the valuable suggestion of an anonymous referee, we analyzed the comovement of the trading volumes for these markets during the identified periods of herding. For this purpose, we obtained the principal components of the trading volumes of all the stock markets for which data was available, as well as for countries categorized as advanced and emerging. Then we regressed the principal components on the herding dummies corresponding to either 10% or 5%, and found positive and statistically significant relationships. This suggests that trading volumes comove during periods of herding. Since, trading volume data was not available for all the stock markets considered, we have not reported these results explicitly in the paper due to lack of one-to-one correspondence with stock price indexes. However, these results are available upon request from the authors. |

| 7 | The index is available at: http://policyuncertainty.com/infectious_EMV.html (accessed on 12 August 2020) |

Appendix A

{kind=link}

{kind=link}

Table A1.

Summary statistics of dependent variables.

| Dependent Variable | Statistic | All Countries | Advanced | Emerging | BRICS | PIIGS | Commodity Exporters |

|---|---|---|---|---|---|---|---|

| D1 | Mean | 0.116 | 0.120 | 0.163 | 0.245 | 0.190 | 0.013 |

| Std. dev. | 0.321 | 0.325 | 0.370 | 0.430 | 0.393 | 0.112 | |

| D2 | Mean | 0.085 | 0.085 | 0.132 | 0.172 | 0.152 | 0.000 |

| Std. dev. | 0.279 | 0.280 | 0.338 | 0.378 | 0.360 | 0.000 |

Note: See notes to Table 2. Source: based on authors’ own calculations of summary statistics.

References

- Akhtaruzzaman, Md, Sabri Boubaker, and Ahmet Sensoy. 2020. Financial contagion during COVID–19 crisis. Finance Research Letters 38: 101604. [Google Scholar] [CrossRef] [PubMed]

- Alexakis, Christos, Konstantinos Eleftheriou, and Patroklos Patsoulis. 2021. COVID-19 containment measures and stock market returns: An international spatial econometrics investigation. Journal of Behavioral and Experimental Finance 29: 100428. [Google Scholar] [CrossRef]

- Alhaj-Yaseen, Yaseen S., and Siu-Kong Yau. 2018. Herding tendency among investors with heterogeneous information: Evidence from China’s equity markets. Journal of Multinational Financial Management 47: 60–75. [Google Scholar] [CrossRef]

- Avery, Christopher, and Peter Zemsky. 1998. Multidimensional uncertainty and herd behavior in financial markets. American Economic Review 88: 724–48. [Google Scholar]

- Babalos, Vassilios, and Stavros Stavroyiannis. 2015. Herding, anti-herding behaviour in metal commodities futures: A novel portfolio-based approach. Applied Economics 47: 4952–66. [Google Scholar] [CrossRef]

- Baker, Scott R., Nicholas Bloom, Steven J. Davis, and Stephen J. Terry. 2020. Covid-Induced Economic Uncertainty. NBER Working Paper No. 26983. Cambridge: National Bureau of Economic Research. [Google Scholar]

- Balcilar, Mehmet, and Riza Demirer. 2015. Impact of Global Shocks and Volatility on Herd Behavior in an Emerging Market: Evidence from Borsa Istanbul. Emerging Markets Finance and Trade 51: 140–59. [Google Scholar] [CrossRef]

- Balcilar, Mehmet, Rıza Demirer, and Shawkat Hammoudeh. 2013. Investor Herds and Regime Switching: Evidence from Gulf Arab Stock Markets. Journal of International Financial Markets, Institutions & Money 23: 295–321. [Google Scholar]

- Balcilar, Mehmet, Rıza Demirer, and Shawkat Hammoudeh. 2014. What Drives Herding in Developing Stock Markets? Relative Roles of Own Volatility and Global Factors. North American Journal of Economics and Finance 29: 418–40. [Google Scholar] [CrossRef]

- Balcilar, Mehmet, Rıza Demirer, and Talat Ulussever. 2017. Does speculation in the oil market drive investor herding in emerging stock markets? Energy Economics 65: 50–63. [Google Scholar] [CrossRef]

- Banerjee, Abhijit V. 1992. A simple model of herd behavior. Quarterly Journal of Economics 107: 797–818. [Google Scholar] [CrossRef] [Green Version]

- Barro, Robert J., and José F. Ursúa. 2012. Rare Macroeconomic Disasters. Annual Review of Economics 4: 83–109. [Google Scholar] [CrossRef]

- Bikhchandani, Sushil, David Hirshleifer, and Ivo Welch. 1992. A theory of fads, fashion, custom, and cultural change as informational cascades. Journal of Political Economy 100: 992–1026. [Google Scholar] [CrossRef]

- Blasco, Natividad, Pilar Corredor, and Sandra Ferreruela. 2012. Does herding affect volatility? Implications for the Spanish stock market. Quantitative Finance 12: 311–27. [Google Scholar] [CrossRef] [Green Version]

- Bouri, Elie, Oguzhan Cepni, David Gabauer, and Rangan Gupta. 2020. Return Connectedness across Asset Classes around the COVID-19 Outbreak. International Review of Financial Analysis 73: 101646. [Google Scholar] [CrossRef]

- Cakan, Esin, Rıza Demirer, Rangan Gupta, and Hardik A. Marfatia. 2019. Oil Speculation and Herding Behavior in Emerging Stock Markets. Journal of Economics and Finance 43: 44–56. [Google Scholar] [CrossRef] [Green Version]

- Chang, Eric C., Joseph W. Cheng, and Ajay Khorana. 2000. An Examination of Herd Behaviour in Equity Markets: An International Perspective. Journal of Banking and Finance 24: 1651–99. [Google Scholar] [CrossRef]

- Chari, Varadarajan V., and Patrick J. Kehoe. 2004. Financial crises as herds: Overturning the critiques. Journal of Economic Theory 119: 129–50. [Google Scholar] [CrossRef]

- Chiang, Thomas C., and Dazhi Zheng. 2010. An empirical analysis of herd behavior in global stock markets. Journal of Banking & Finance 34: 1911–21. [Google Scholar]

- Christie, William G., and Roger D. Huang. 1995. Following the Pied Piper: Do individual Returns Herd around the Market? Financial Analyst Journal 51: 31–37. [Google Scholar] [CrossRef]

- De Long, J. Bradford, Andrei Shleifer, Lawrence H. Summers, and Robert J. Waldmann. 1990. Noise Trader Risk in Financial Markets. Journal of Political Economy 98: 703–38. [Google Scholar] [CrossRef]

- Demirer, Riza, Ali M. Kutan, and Chun-Da Chen. 2010. Do Investors Herd in Emerging Stock Markets? Evidence from the Taiwanese Market. Journal of Economic Behavior & Organization 76: 283–95. [Google Scholar]

- Demirer, Rıza, and Ali M. Kutan. 2006. Does Herding Behavior Exist in Chinese Stock Market? Journal of International Financial Markets, Institutions and Money 16: 123–42. [Google Scholar] [CrossRef]

- Demirer, Rıza, Karyl B. Leggio, and Donald Lien. 2019. Herding and Flash Events: Evidence from the 2010 Flash Crash. Finance Research Letters 31: 476–79. [Google Scholar] [CrossRef]

- Devenow, Andrea, and Ivo Welch. 1996. Rational Herding in Financial Economics. European Economic Review 40: 603–15. [Google Scholar] [CrossRef]

- Fernandez-Perez, Adrian, Aaron Gilbert, Ivan Indriawan, and Nhut H. Nguyen. 2020. COVID-19 Pandemic and Stock Market Response: A Culture Effect. Journal of Behavioral and Experimental Finance 29: 100454. [Google Scholar] [CrossRef]

- Froot, Kenneth A., and Maurice Obstfeld. 1991. Intrinsic Bubbles: The Case of Stock Prices. American Economic Review 81: 1189–214. [Google Scholar]

- Froot, Kenneth A., David S. Scharfstein, and Jeremy C. Stein. 1992. Herd on the street: Informational inefficiencies in a market with short-term speculation. Journal of Finance 47: 1461–84. [Google Scholar] [CrossRef]

- Gleason, Kimberly C., Ike Mathur, and Mark A. Peterson. 2004. Analysis of intraday herding behaviour among the sector ETFs. Journal of Empirical Finance 11: 681–94. [Google Scholar] [CrossRef]

- Goodell, John W. 2020. COVID-19 and finance: Agendas for future research. Finance Research Letters 35: 101512. [Google Scholar] [CrossRef] [PubMed]

- Gourio, Francois. 2012. Disaster Risk and Business Cycles. The American Economic Review 102: 2734–66. [Google Scholar] [CrossRef] [Green Version]

- Haldar, Anasuya, and Narayan Sethi. 2020. The News Effect of COVID-19 on Global Financial Market Volatility. Bulletin of Monetary Economics and Banking 24: 33–58. [Google Scholar]

- Hey, John D., and Andrea Morone. 2004. Do Markets Drive Out Lemmings-or Vice Versa? Economica 71: 637–59. [Google Scholar] [CrossRef]

- Maug, Ernst G., and Narayan Y. Naik. 1996. Herding and Delegated Portfolio Management. New York: Mimeo, London Business School, Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=7362 (accessed on 9 September 2021).

- Milcheva, Stanimira. 2021. Volatility and the Cross-Section of Real Estate Equity Returns during COVID’19. The Journal of Real Estate Finance and Economics, 1–28. [Google Scholar] [CrossRef]

- Nofsinger, J., and R. Sias. 1999. Herding and feedback trading by institutional and individual investors. Journal of Finance 54: 2263–95. [Google Scholar] [CrossRef]

- Ozkan, Oktay. 2021. Impact of COVID-19 on stock market efficiency: Evidence from developed countries. Research in International Business and Finance 58: 101445. [Google Scholar] [CrossRef] [PubMed]

- Salisu, Afees A., Ahamuefula E. Ogbonna, Tirimisiyu F. Oloko, and Idris A. Adediran. 2021. A New Index for Measuring Uncertainty Due to the COVID-19 Pandemic. Sustainability 13: 3212. [Google Scholar] [CrossRef]

- Scherf, Matthias, Xenia Matschke, and Marc Oliver Rieger. 2021. Stock market reactions to COVID-19 lockdown: A global analysis. Finance Research Letters, 102245. [Google Scholar] [CrossRef]

- Sharif, Arshian, Chaker Aloui, and Larisa Yarovaya. 2020. COVID-19 pandemic, oil prices, stock market, geopolitical risk and policy uncertainty nexus in the US economy: Fresh evidence from the wavelet-based approach. International Review of Financial Analysis 70: 101496. [Google Scholar]

- Bikhchandani, Sushil, and Mr Sunil Sharma. 2001. Herd behavior in financial markets: A review. IMF Staff Papers 47: 279–310. [Google Scholar] [CrossRef] [Green Version]

- Shleifer, Andrei, and Lawrence H. Summers. 1990. The noise trader approach to finance. Journal of Economic Perspectives 4: 19–33. [Google Scholar] [CrossRef] [Green Version]

- Sibande, Xolani, Rangan Gupta, Riza Demirer, and Elie Bouri. 2021. Investor Sentiment and (Anti-)Herding in the Currency Market: Evidence from Twitter Feed Data. Journal of Behavioral Finance, 1–17. [Google Scholar] [CrossRef]

- Stavroyiannis, Stavros, and Vassilios Babalos. 2017. Herding, Faith-Based Investments and the Global Financial Crisis: Empirical Evidence from Static and Dynamic Models. Journal of Behavioural Finance 18: 478–89. [Google Scholar] [CrossRef]

- Teraji, Shinji. 2003. Herd behavior and the quality of opinions. Journal of Socio-Economics 32: 661–73. [Google Scholar] [CrossRef]

- Uwilingiye, Josine, Esin Cakan, Riza Demirer, and Rangan Gupta. 2019. A Note on the Technology Herd: Evidence from Large Institutional Investors. Review of Behavioral Finance 11: 294–308. [Google Scholar] [CrossRef]

- Wachter, Jessica A. 2013. Can time-varying risk of rare disasters explain aggregate stock market volatility? Journal of Finance 68: 987–1035. [Google Scholar] [CrossRef] [Green Version]

Figure 1.

Plot of the EMVID Index. Source: Baker et al. (2020): http://policyuncertainty.com/infectious_EMV.html (accessed on 12 August 2020).

Figure 1.

Plot of the EMVID Index. Source: Baker et al. (2020): http://policyuncertainty.com/infectious_EMV.html (accessed on 12 August 2020).

Figure 2.

Rolling-window herding coefficients (source: based on the authors’ own estimation of Equation (2)). Note: the horizontal lines with short dashes represent a 10% significance level, while the long-dashed lines represent a 5% significance level along with the shaded areas associated D1 and D2 dummy variables. As D2 is corresponds to higher significance level, it overlaps with D1.

Figure 2.

Rolling-window herding coefficients (source: based on the authors’ own estimation of Equation (2)). Note: the horizontal lines with short dashes represent a 10% significance level, while the long-dashed lines represent a 5% significance level along with the shaded areas associated D1 and D2 dummy variables. As D2 is corresponds to higher significance level, it overlaps with D1.

Table 1.

Estimates of the Static Herding Model.

| Sample | Parameters | All Countries | Advanced | Emerging | BRICS | PIIGS | Commodity Exporters |

|---|---|---|---|---|---|---|---|

| Full-Sample | α0 | 0.008 *** | 0.005 *** | 0.01 *** | 0.009 *** | 0.006 *** | 0.006 *** |

| α1 | 0.288 *** | 0.258 *** | 0.269 *** | 0.248 *** | 0.146 *** | 0.176 *** | |

| α2 | 0.994 *** | 0.301 * | 1.474 *** | 1.388 *** | 0.915 *** | 1.964 *** | |

| Pre-COVID | α0 | 0.006 *** | 0.004 *** | 0.007 *** | 0.006 *** | 0.005 *** | 0.005 *** |

| α1 | 0.231 *** | 0.172 *** | 0.22 | −0.012 | 0.004 | 0.131 | |

| α2 | 1.527 | −0.539 | 3.715 | 12.887 * | 8.59 | 1.774 | |

| During-COVID | α0 | 0.007 *** | 0.006 *** | 0.008 *** | 0.008 *** | 0.005 *** | 0.007 *** |

| α1 | 0.354 *** | 0.255 *** | 0.442 | 0.339 | 0.313 | 0.279 | |

| α2 | −0.36 | −0.334 | −0.881 | −0.473 * | −1.306 | −0.205 |

Note: Full-Sample: 23 May 2019 to 10 August 2020; pre-COVID: 23 May 2019 to 31 December 2020; during-COVID: 1 January 2020 to 10 August 2020; the parameters of the model estimated is: CSADt = α0 + α1|Rm,t|+α2R2m,t + εt; ***, * significant at 1%, and 10% levels, respectively. Source: based on the authors’ own estimation of Equation (2).

Table 2.

Estimates of the Probit Model.

| Dependent Variable | Parameters | All Countries | Advanced | Emerging | BRICS | PIIGS | Commodity Exporters |

|---|---|---|---|---|---|---|---|

| D1 | β0 | −2.456 *** | −2.093 *** | −2.204 *** | −1.026 *** | −2.464 *** | −2.632 *** |

| β1 | 0.064 *** | 0.050 *** | 0.070 *** | 0.027 *** | 0.092 *** | 0.022 ** | |

| D2 | β0 | −2.551 *** | −2.166 *** | −2.599 *** | −1.420 *** | −2.460 *** | |

| β1 | 0.056 *** | 0.042 *** | 0.075 ** | 0.034 *** | 0.077 *** |

Note: See notes to Table 1; Di, i = 1, 2 correspond to a value of 1 when the rolling t-statistics of α2 −1.645 and −1.96, respectively. The parameters of the model estimated are as follows: Pr(Di = 1|X) = β0 + β1EMVID; ***, and ** significant at 1%, and 5% levels, respectively. Source: based on authors’ own estimation of the probit model.

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Bouri, E.; Demirer, R.; Gupta, R.; Nel, J. COVID-19 Pandemic and Investor Herding in International Stock Markets. Risks 2021, 9, 168. https://doi.org/10.3390/risks9090168

AMA Style

Bouri E, Demirer R, Gupta R, Nel J. COVID-19 Pandemic and Investor Herding in International Stock Markets. Risks. 2021; 9(9):168. https://doi.org/10.3390/risks9090168

Chicago/Turabian StyleBouri, Elie, Riza Demirer, Rangan Gupta, and Jacobus Nel. 2021. "COVID-19 Pandemic and Investor Herding in International Stock Markets" Risks 9, no. 9: 168. https://doi.org/10.3390/risks9090168

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.