The Ability of Selected European Countries to Face the Impending Economic Crisis Caused by COVID-19 in the Context of the Global Economic Crisis of 2008

Abstract

:1. Introduction

2. Materials and Methods

3. Results

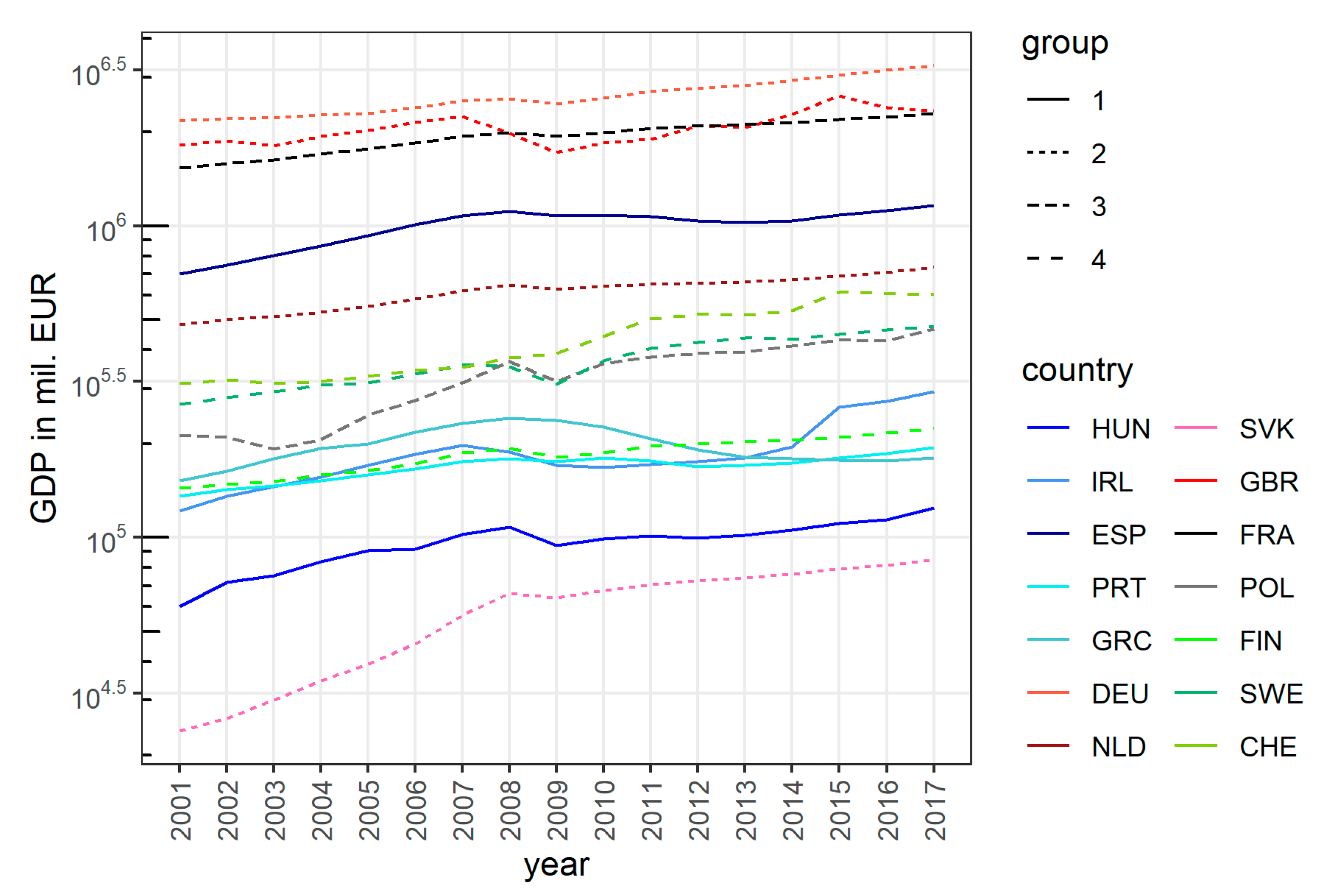

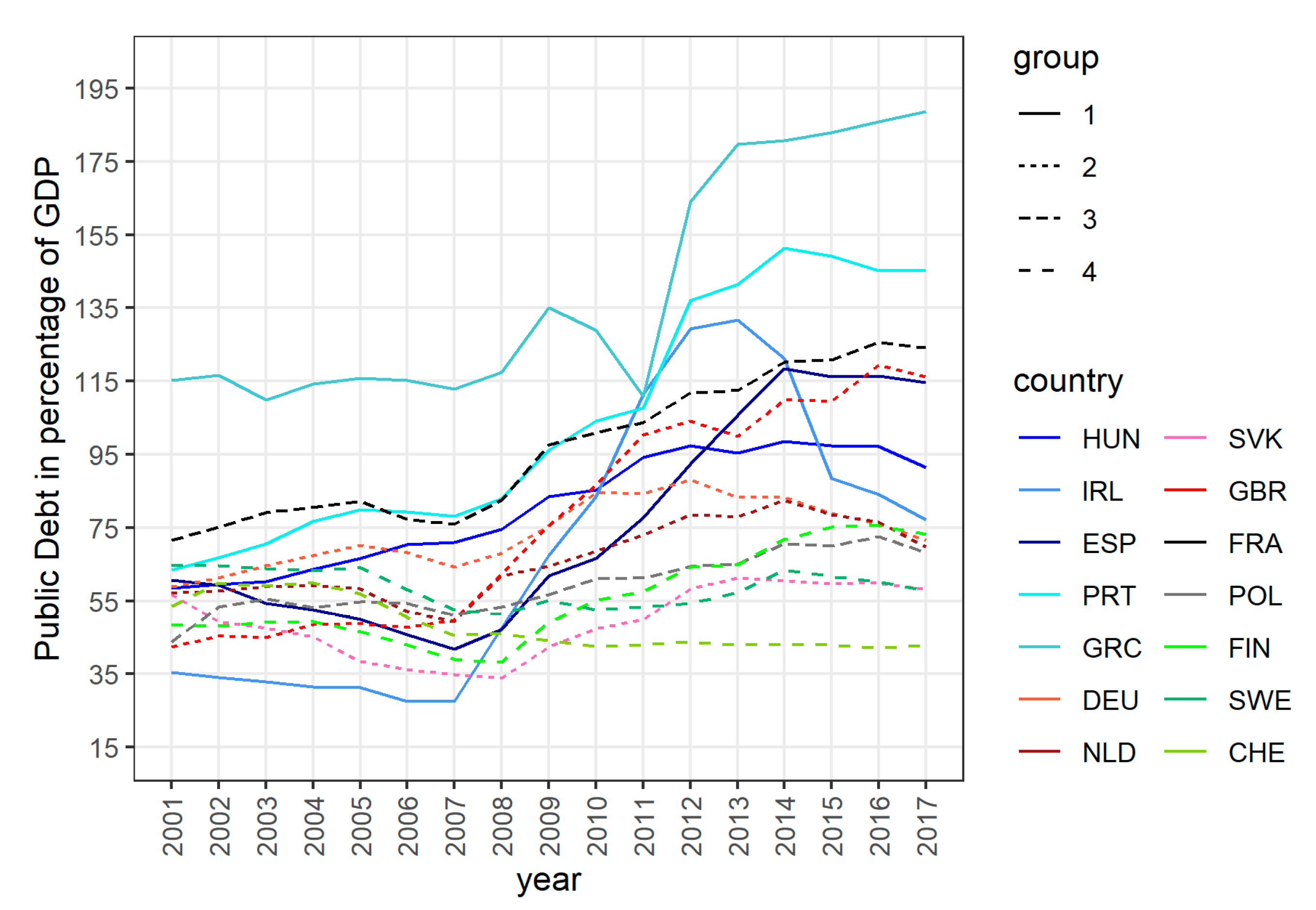

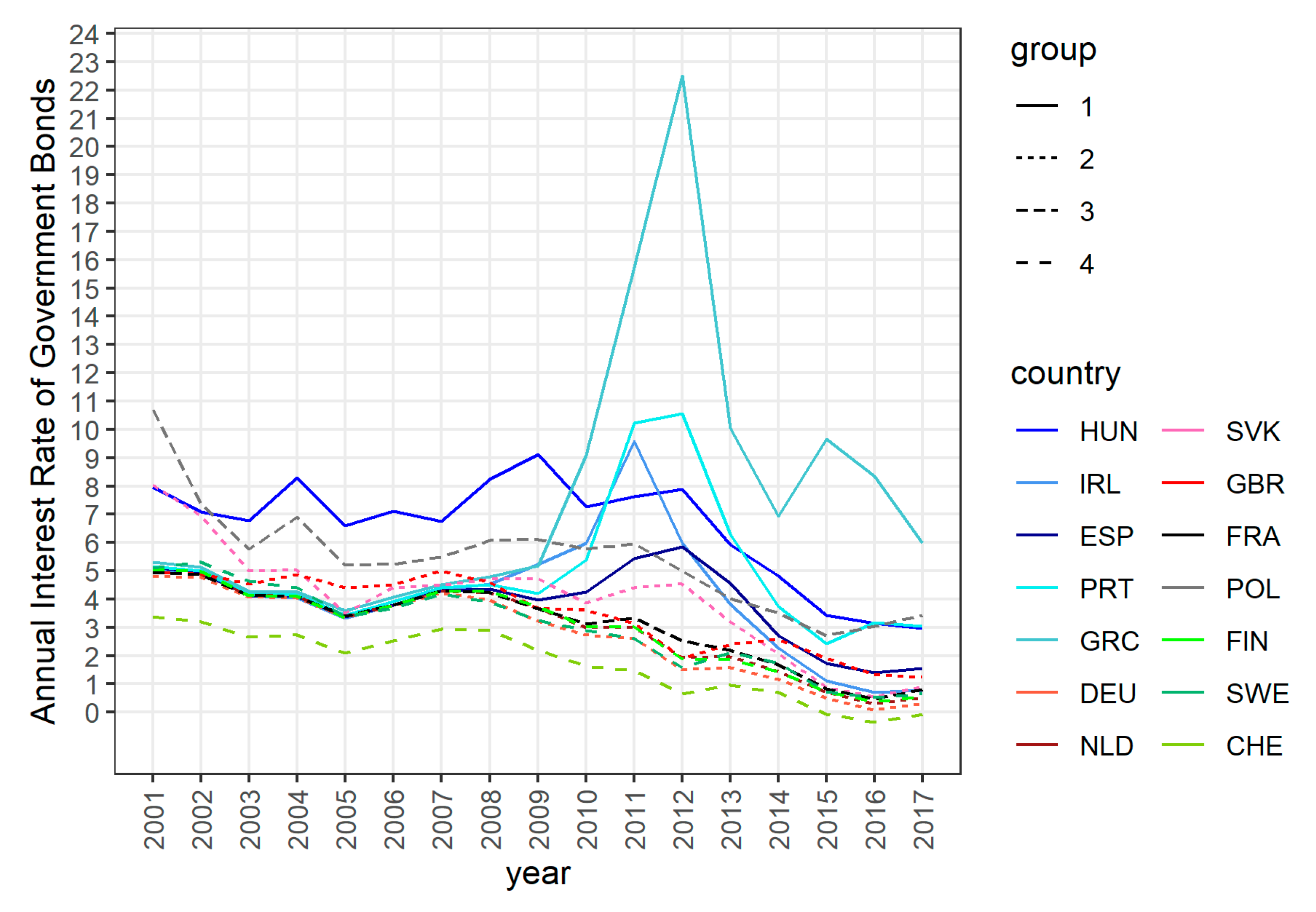

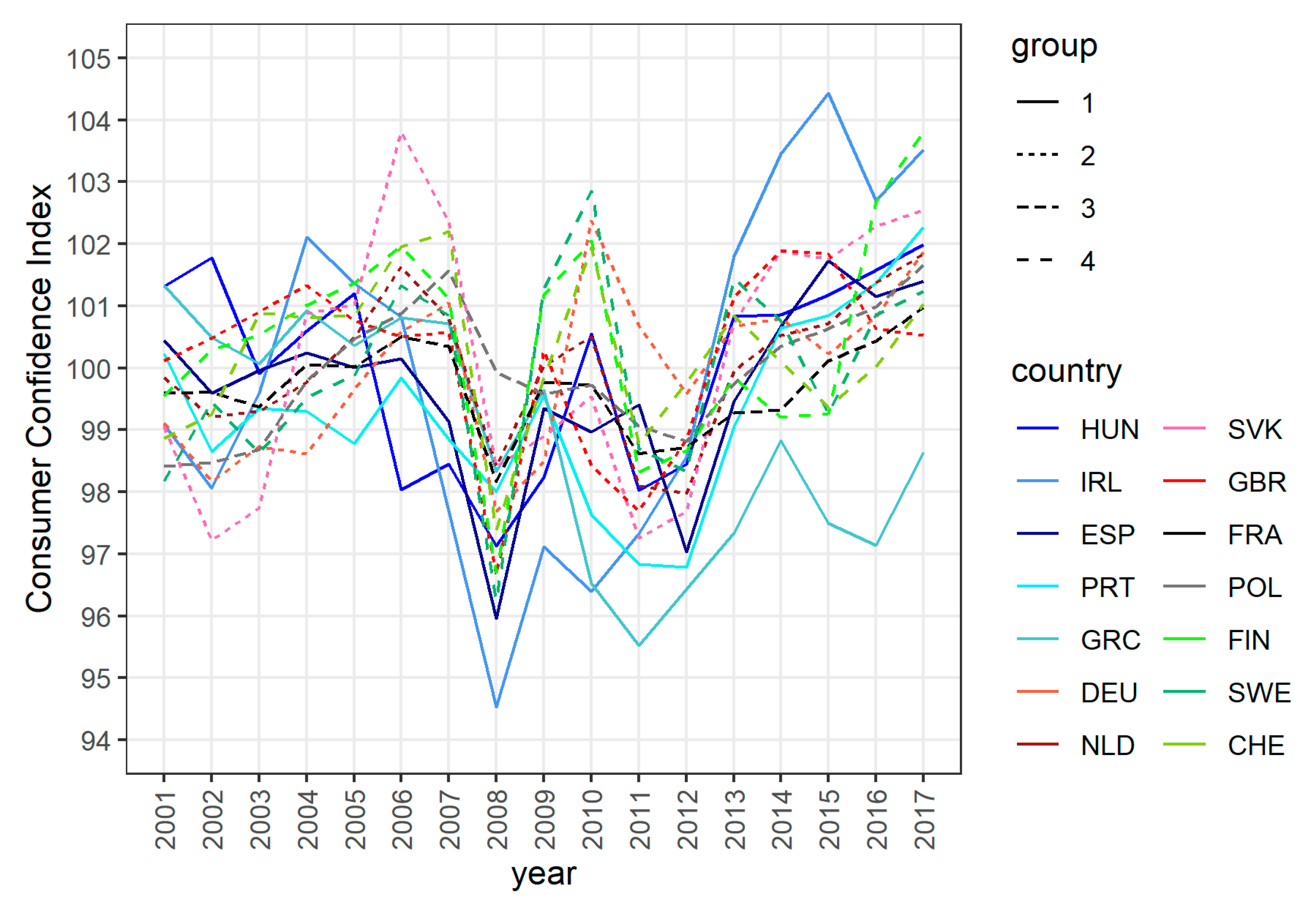

3.1. Economic Indicators Development

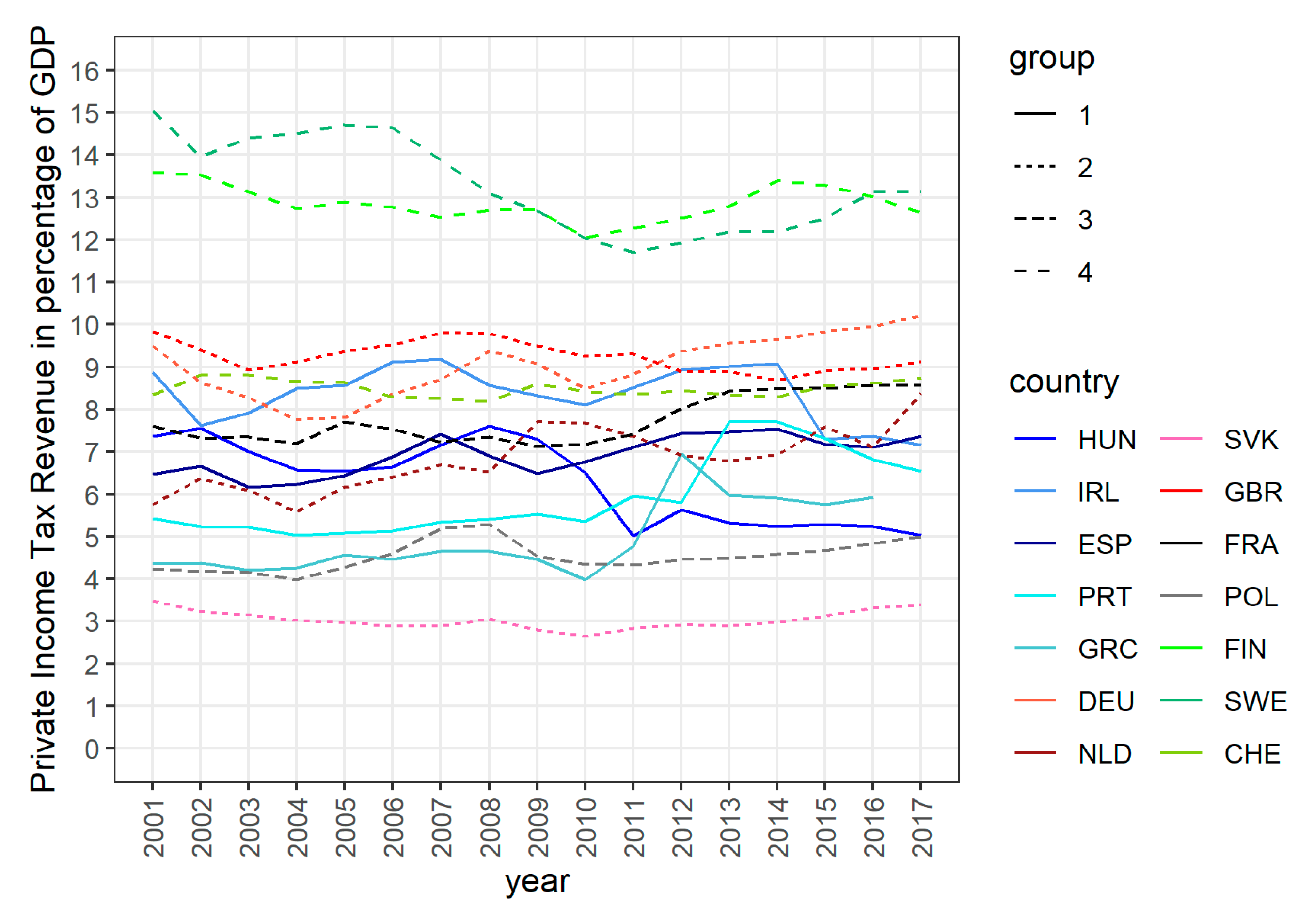

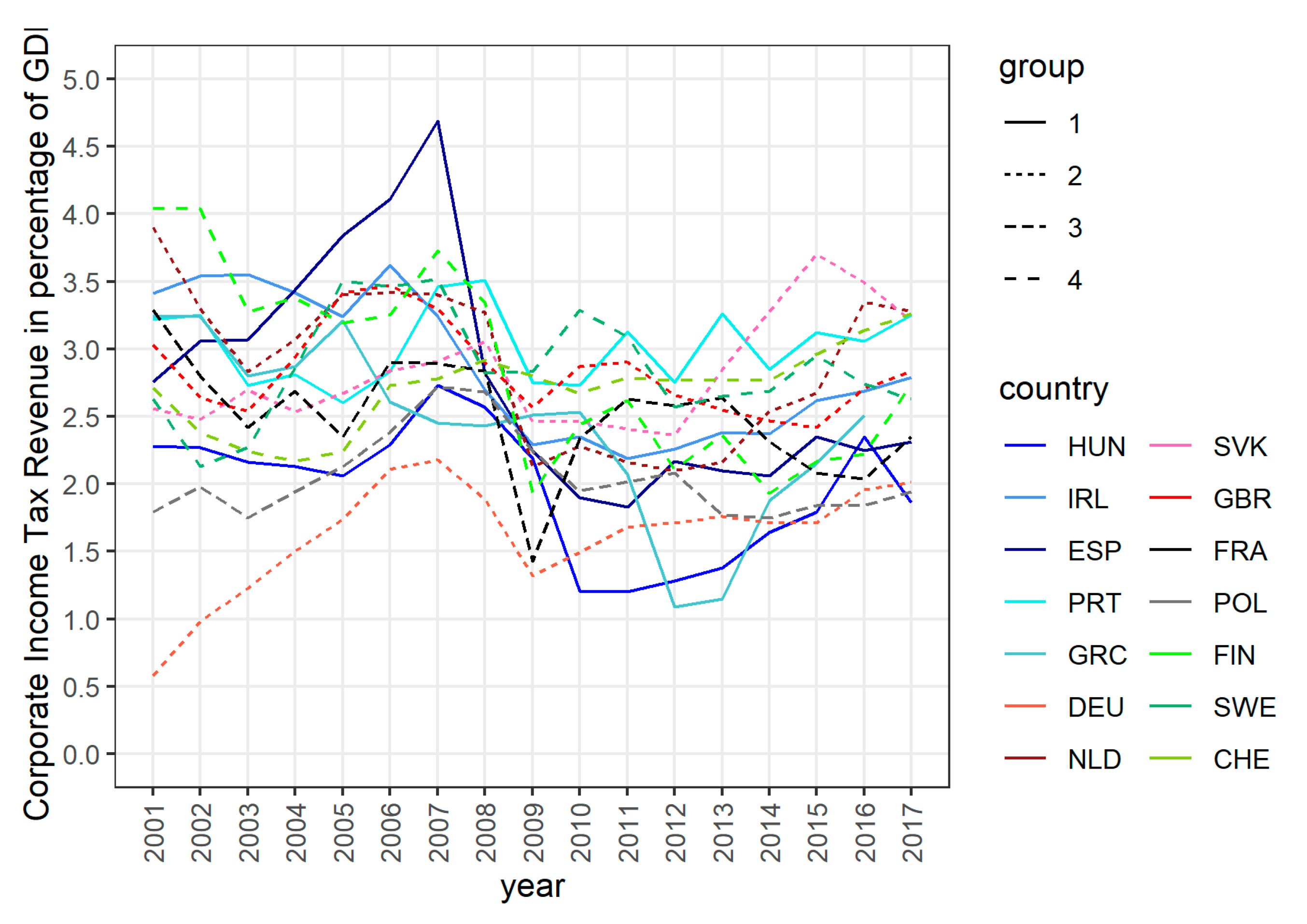

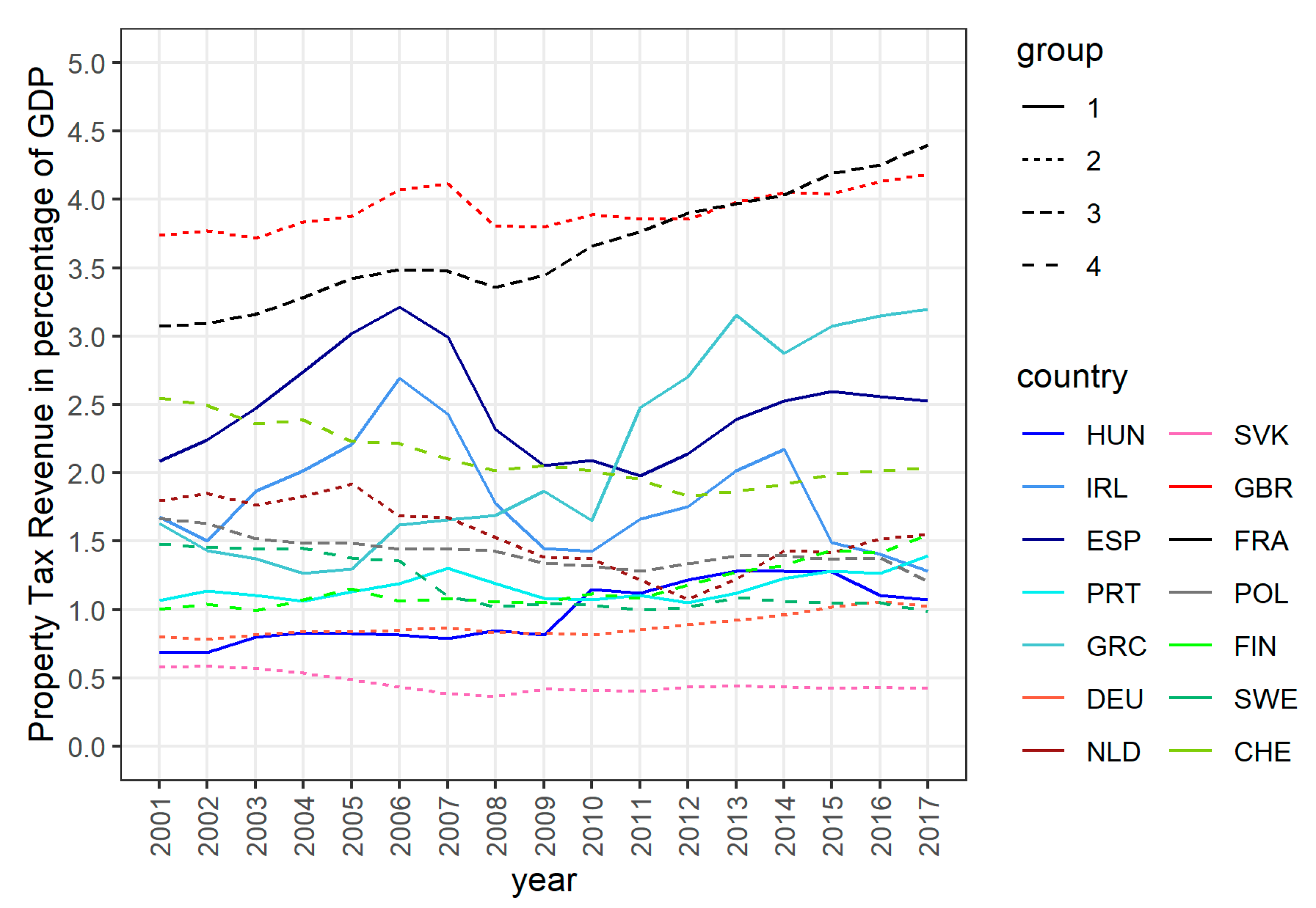

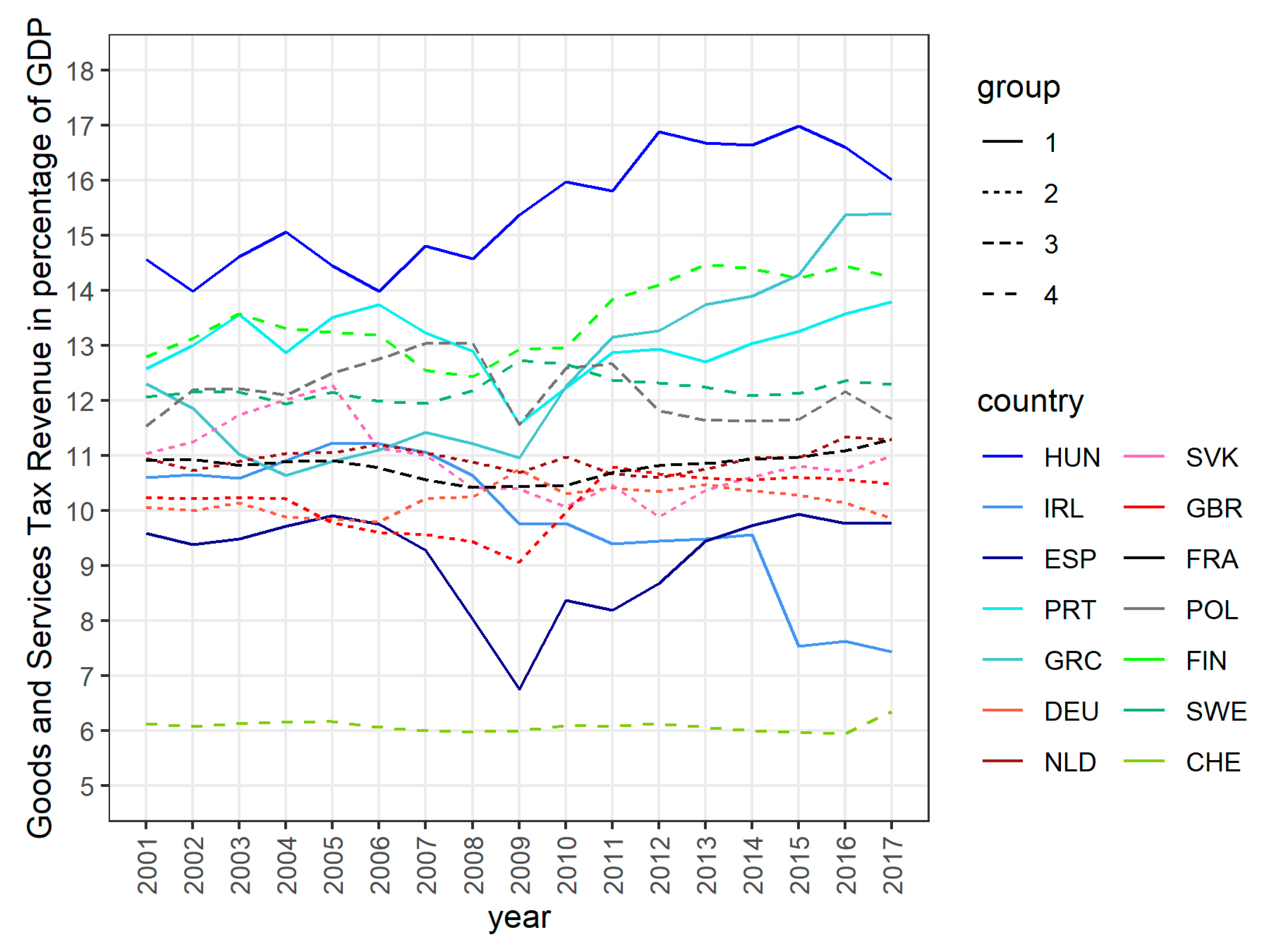

3.2. The Impact of Tax Revenues on the GDP

3.2.1. Group 1

3.2.2. Group 2

3.2.3. Group 3

3.2.4. Group 4

4. Discussion

5. Conclusions

Supplementary Materials

Author Contributions

Funding

Conflicts of Interest

References

- Ağca, Şenay, and Deniz Igan. 2019. Fiscal consolidations and the cost of credit. Journal of International Economics 120: 84–108. [Google Scholar] [CrossRef]

- Alesina, Alberto, Carlo Favero, and Francesco Giavazzi. 2015. The output effect of fiscal consolidation plans. Journal of International Economics 96: S19–S42. [Google Scholar] [CrossRef] [Green Version]

- Alesina, Alberto, Omar Barbiero, Carlo Favero, Francesco Giavazzi, and Matteo Paradisi. 2017. The Effects of Fiscal Consolidations: Theory and Evidence (No. w23385). Cambridge: National Bureau of Economic Research, Available online: https://www.nber.org/papers/w23385.pdf (accessed on 22 July 2020).

- Anderson, Derek, Benjamin Hunt, and Stephen Snudden. 2014. Fiscal consolidation in the euro area: How much pain can structural reforms ease? Journal of Policy Modeling 36: 785–99. [Google Scholar] [CrossRef] [Green Version]

- Antelo, Manel, and David Peón. 2014. Fiscal consolidation and the sustainability of public debt in the GIPSI countries. Cuadernos de Economía 37: 52–71. [Google Scholar] [CrossRef] [Green Version]

- Attinasi, Maria Grazia, and Luca Metelli. 2017. Is fiscal consolidation self-defeating? A panel-VAR analysis for the Euro area countries. Journal of International Money and Finance 74: 147–64. [Google Scholar] [CrossRef] [Green Version]

- Banerjee, Ryan, and Fabrizio Zampolli. 2019. What drives the short-run costs of fiscal consolidation? Evidence from OECD countries. Economic Modelling 82: 420–36. [Google Scholar] [CrossRef] [Green Version]

- Caselli, Paola. 2001. Fiscal consolidation under fixed exchange rates. European Economic Review 45: 425–50. [Google Scholar] [CrossRef]

- Castro, Vítor. 2017. The impact of fiscal consolidations on the functional components of government expenditures. Economic Modelling 60: 138–50. [Google Scholar] [CrossRef] [Green Version]

- Cimadomo, Jacopo, Sebastian Hauptmeier, and Tom Zimmermann. 2014. Fiscal consolidations and bank balance sheets. Journal of International Money and Finance 45: 74–90. [Google Scholar] [CrossRef] [Green Version]

- Comisión Europea. 2020a. European Economic Forescast Spring 2020. Available online: https://ec.europa.eu/info/sites/info/files/economy-finance/ip125_en.pdf (accessed on 22 July 2020).

- Comisión Europea. 2020b. European Economic Forescast Summer 2020. Available online: https://ec.europa.eu/info/sites/info/files/economy-finance/ip132_en.pdf (accessed on 22 July 2020).

- Comisión Europea. 2020c. Recovery Plan for Europe. Available online: https://ec.europa.eu/info/live-work-travel-eu/health/coronavirus-response/recovery-plan-europe_en#documents (accessed on 22 July 2020).

- Comisión Europea. 2020d. Recovery of Euro Area and EU Economic Sentiment Intensifies—Employment Expectations again Up. Available online: https://ec.europa.eu/info/sites/info/files/full_bcs_2020_06_en.pdf (accessed on 22 July 2020).

- Croissant, Yves, and Giovanni Millo. 2008. Panel Data Econometrics in R: The Plm Package. Journal of Statistical Software 27: 1–43. [Google Scholar] [CrossRef] [Green Version]

- De Vito, Antonio, and Juan-Pedro Gomez. 2020. Estimating the COVID-19 cash crunch: Global evidence and policy. Journal of Accounting and Public Policy 39: 106741. [Google Scholar] [CrossRef]

- Dimitras, Augustinos I., Maria I. Kyriakou, and George Iatridis. 2015. Financial crisis, GDP variation and earnings management in Europe. Research in International Business and Finance 34: 338–54. [Google Scholar] [CrossRef]

- Erceg, Christopher J., and Jesper Lindé. 2013. Fiscal consolidation in a currency union: Spending cuts vs. tax hikes. Journal of Economic Dynamics and Control 37: 422–45. [Google Scholar] [CrossRef] [Green Version]

- Fatás, Antonio, and Lawrence H. Summers. 2018. The permanent effects of fiscal consolidations. Journal of International Economics 112: 238–50. [Google Scholar] [CrossRef]

- Feld, Lars P., and Gebhard Kirchgässner. 2003. The impact of corporate and personal income taxes on the location of firms and on employment: Some panel evidence for the Swiss cantons. Journal of Public Economics 87: 129–55. [Google Scholar] [CrossRef] [Green Version]

- Fernandes, Nuno. 2020. Economic Effects of Coronavirus Outbreak (COVID-19) on the World Economy. Available online: http://www.agoraceg.org/system/files/iese_impact_covid19.pdf (accessed on 22 July 2020).

- Garrett, Thomas A. 2007. Economic Effects of the 1918 Influenza Pandemic. Available online: http://www.indexinvestor.com/resources/Research-Materials/Disease/Economic_Impact_of_1918_Influenza.pdf (accessed on 22 July 2020).

- Goldman Sachs. 2020. Reopening the Economy. April 28. Available online: https://www.goldmansachs.com/insights/talks-at-gs/04-30-2020-phasing-in-the-reopening-of-the-economy-f/presentation.pdf (accessed on 22 July 2020).

- Heylen, Freddy, and Gerdie Everaert. 2000. Success and failure of fiscal consolidation in the OECD: A multivariate analysis. Public Choice 105: 103–24. [Google Scholar] [CrossRef]

- Honda, Yuzo. 1985. Testing the Error Components Model with Non-Normal Disturbances. The Review of Economic Studies 52: 681–90. [Google Scholar] [CrossRef]

- Jones, Erik. 2016. Competitiveness and the European financial crisis. In The Political and Economic Dynamics of the Eurozone Crisis. Oxford: Oxford University Press, pp. 79–99. [Google Scholar]

- Lee, Young, and Roger H. Gordon. 2005. Tax structure and economic growth. Journal of Public Economics 89: 1027–43. [Google Scholar] [CrossRef]

- Lee, Jong-Wha, and Warwick J. McKibbin. 2004. Estimating the global economic costs of SARS. In Learning from SARS: Preparing for the Next Disease Outbreak: Workshop Summary; Washington, DC: National Academies Press, April, p. 92. Available online: https://www.ncbi.nlm.nih.gov/books/NBK92473/ (accessed on 22 July 2020).

- Lemoine, Matthieu, and Jesper Lindé. 2016. Fiscal consolidation under imperfect credibility. European Economic Review 88: 108–41. [Google Scholar] [CrossRef] [Green Version]

- Leung, Kathy, Joseph T. Wu, Di Liu, and Gabriel M. Leung. 2020. First-wave COVID-19 transmissibility and severity in China outside Hubei after control measures, and second-wave scenario planning: A modelling impact assessment. The Lancet 395: 1382–93. [Google Scholar] [CrossRef]

- Manganelli, Benedetto, Pierluigi Morano, Paolo Rosato, and Pierfrancesco De Paola. 2020. The Effect of Taxation on Investment Demand in the Real Estate Market: The Italian Experience. Buildings 10: 115. [Google Scholar] [CrossRef]

- Moody’s Analytics. 2020. Europe Economic Outlook: Global Recession. April. Available online: https://www.moodysanalytics.com/-/media/presentation/2020/europe-economic-outlook.pdf (accessed on 22 July 2020).

- O’Connor, Casey M., Afshin A. Anoushiravani, Matthew R. DiCaprio, William L. Healy, and Richard Iorio. 2020. Economic recovery after the COVID-19 pandemic: Resuming elective orthopedic surgery and total joint arthroplasty. The Journal of Arthroplasty 35: 32–36. [Google Scholar] [CrossRef]

- OECD. 2011. Fiscal consolidation: Targets, plans and measures. OECD Journal on Budgeting 11: 2. [Google Scholar] [CrossRef]

- OECD. 2013. Government at a Glance 2013. Paris: OECD Publishing. [Google Scholar] [CrossRef]

- Plackett, Robin L. 1983. Karl Pearson and the Chi-Squared Test. International Statistical Review/Revue Internationale de Statistique 51: 59–72. [Google Scholar] [CrossRef]

- Qiu, Wuqi, Cordia Chu, Ayan Mao, and Jing Wu. 2018. The Impacts on Health, Society, and Economy of SARS and H7N9 Outbreaks in China: A Case Comparison Study. Journal of Environmental and Public Health 2018: 1–7. [Google Scholar] [CrossRef] [PubMed]

- Reicher, Claire. 2014. A set of estimated fiscal rules for a cross-section of countries: Stabilization and consolidation through which instruments? Journal of Macroeconomics 42: 184–98. [Google Scholar] [CrossRef] [Green Version]

- Standard & Poor’s. 2020. Large Risks to Growth Ahead_European Economic Snapshots, 4th May. Available online: https://www.standardandpoors.com/pt_LA/delegate/getPDF?articleId=2424390&type=COMMENTS&subType (accessed on 22 July 2020).

- Villar Rubio, Elena, Quesada Rubio, José Manuel, and Valentín Molina Moreno. 2015. Convergence analysis of environmental fiscal pressure across EU-15 countries. Energy & Environment 26: 789–802. [Google Scholar] [CrossRef]

- Von Hagen, Jürgen, and Rolf R. Strauch. 2001. Fiscal consolidations: Quality, conomic conditions, and success. Public Choice 109: 327–46. [Google Scholar] [CrossRef]

- White, Halbert. 1980. A Heteroskedasticity-Consistent Covariance Matrix Estimator and a Direct Test for Heteroskedasticity. Econometrica: Journal of the Econometric Society 48: 817–38. Available online: https://econpapers.repec.org/RePEc:ecm:emetrp:v:48:y:1980:i:4:p:817-38 (accessed on 22 July 2020). [CrossRef]

- Williams, Richard. 2015. Panel Data 4: Fixed Effects vs. Random Effects Models. University of Notre Dame. Available online: https://www3.nd.edu/~rwilliam/stats3/panel04-fixedvsrandom.pdf (accessed on 22 July 2020).

- Wooldridge, Jeffrey M. 2002. Econometric Analysis of Cross Section and Panel Data. Cambridge: MIT Press, pp. 1–735. Available online: https://jrvargas.files.wordpress.com/2011/01/wooldridge_j-_2002_econometric_analysis_of_cross_section_and_panel_data.pdf (accessed on 22 July 2020).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| PM | FM | |||

|---|---|---|---|---|

| Regression Coefficient | p-Value | Regression Coefficient | p-Value | |

| PITR | −46,153.7 | 0.027 | 5775.6 | 0.700 |

| CITR | −144,551 | 0.002 | −28,025.5 | 0.020 |

| PTR | 227,780.3 | <0.001 | 72,750.3 | 0.113 |

| DEF | 9738.6 | 0.19 | 94.7 | 0.959 |

| DEBT | −1384.1 | 0.11 | 315.5 | 0.234 |

| GTR | −70,369.5 | <0.001 | −37,311.2 | 0.007 |

| IR | −26,952.9 | 0.025 | −11,077.7 | 0.203 |

| CCI | −25,030.1 | 0.187 | −8995.2 | 0.119 |

| PM | FM | |||

|---|---|---|---|---|

| Regression Coefficient | p-Value | Regression Coefficient | p-Value | |

| PITR | 185,843.7 | 0.000 | 136,700.6 | 0.000 |

| CITR | −516,424.0 | 0.000 | −101,089.0 | 0.079 |

| PTR | 94,962.0 | 0.275 | 577,000.1 | 0.000 |

| DEF | 92,066.7 | 0.001 | 30,460.0 | 0.007 |

| DEBT | 11,980.6 | 0.006 | 4262.9 | 0.021 |

| GTR | −458,229.0 | <0.001 | −74,839.1 | 0.084 |

| IR | 67,232.6 | 0.161 | −29,486.8 | 0.149 |

| CCI | 87,290.1 | 0.019 | 10,309.4 | 0.458 |

| PM | FM | |||

|---|---|---|---|---|

| Regression Coefficient | p-Value | Regression Coefficient | p-Value | |

| PITR | 185,843.7 | 0.000 | 136,700.6 | 0.000 |

| CITR | −516,424.0 | 0.000 | −101,089.0 | 0.079 |

| PTR | 94,962.0 | 0.275 | 577,000.1 | 0.000 |

| DEF | 92,066.7 | 0.001 | 30,460.0 | 0.007 |

| DEBT | 11,980.6 | 0.006 | 4262.9 | 0.021 |

| GTR | −458,229.0 | <0.001 | −74,839.1 | 0.084 |

| IR | 67,232.6 | 0.161 | −29,486.8 | 0.149 |

| CCI | 87,290.1 | 0.019 | 10,309.4 | 0.458 |

| PM | FM | |||

|---|---|---|---|---|

| Regression Coefficient | p-Value | Regression Coefficient | p-Value | |

| PITR | 51,884.6 | <0.001 | 25,508.9 | 0.000 |

| CITR | 59,293.7 | 0.029 | 38,597.4 | 0.015 |

| PTR | −263,748 | <0.001 | −15,579.8 | 0.697 |

| DEF | −19,901.1 | 0.009 | −13,677.1 | 0.002 |

| DEBT | 1239.6 | 0.46 | −4984.3 | 0.000 |

| GTR | −88,139.1 | <0.001 | −21,602.6 | 0.127 |

| IR | −51,410.8 | <0.001 | −55,667.6 | 0.000 |

| CCI | −5,074.2 | 0.223 | −5816.6 | 0.017 |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Oravský, R.; Tóth, P.; Bánociová, A. The Ability of Selected European Countries to Face the Impending Economic Crisis Caused by COVID-19 in the Context of the Global Economic Crisis of 2008. J. Risk Financial Manag. 2020, 13, 179. https://doi.org/10.3390/jrfm13080179

Oravský R, Tóth P, Bánociová A. The Ability of Selected European Countries to Face the Impending Economic Crisis Caused by COVID-19 in the Context of the Global Economic Crisis of 2008. Journal of Risk and Financial Management. 2020; 13(8):179. https://doi.org/10.3390/jrfm13080179

Chicago/Turabian StyleOravský, Róbert, Peter Tóth, and Anna Bánociová. 2020. "The Ability of Selected European Countries to Face the Impending Economic Crisis Caused by COVID-19 in the Context of the Global Economic Crisis of 2008" Journal of Risk and Financial Management 13, no. 8: 179. https://doi.org/10.3390/jrfm13080179