Course of Values of Key Performance Indicators in City Hotels during the COVID-19 Pandemic: Poland Case Study

1

Department of Regional Geography and Tourism, Faculty of Earth Sciences and Spatial Management, Maria Curie-Skłodowska University, 20-718 Lublin, Poland

2

Faculty of Tourism and Recreation, University College of Tourism and Ecology, 34-200 Sucha Beskidzka, Poland

3

Institute of Tourism, Faculty of Tourism and Recreation, University School of Physical Education in Krakow, 31-571 Krakow, Poland

*

Authors to whom correspondence should be addressed.

Sustainability 2022, 14(19), 12454; https://doi.org/10.3390/su141912454

Submission received: 3 August 2022

/

Revised: 23 September 2022

/

Accepted: 26 September 2022

/

Published: 30 September 2022

(This article belongs to the Special Issue Current Trends in Tourism under COVID-19 and Future Implications)

Abstract

:The main goal of this article is to assess the functioning of hotels during the crisis caused by the COVID-19 pandemic. The analysis was carried out on the basis of selected Key Performance Indicators (KPI) in hotels in Polish cities (Kraków; Poznań; Tri-City: Gdańsk, Gdynia, Sopot; Warsaw; Wrocław). The time range of the analysis covers the whole period of the COVID-19 pandemic in Poland (March 2020–February 2022) with data for 2019—before the outbreak of the pandemic. The analysis of the collected results of OCC, ADR, and RevPAR generally indicates instability of the basic economic indicators dependent not only on the demand limited by the pandemic restrictions but also on the type of tourism prevailing in individual cities. There is a difference between the hotel industry in cities, based mainly on foreign guests and business tourism, and the hotel industry in tourist/coastal regions, which are dominated by leisure tourism. During the greatest restrictions, hotels in Poland recorded huge drops in KPIs: a 95% drop in OCC and RevPAR. It was also found that the instability of demand during the pandemic and rapid changes in the values of the indicators prove the need for greater use of KPI benchmarks.

1. Introduction

The course of the SARS-CoV-2 coronavirus pandemic and its negative economic dimension has been one of the hottest topics of recent years, and its effects will be experienced for many years to come. Already in the first months of 2020, the European Parliament estimated that the European Union tourism industry, which employs around 13 million people, will lose around EUR 1 trillion in revenue per month due to the spread of the COVID-19 pandemic [1]. According to the UNWTO data, in 2020 the global tourism economy regressed by 30 years in performance. In comparison to 2019, the loss of international tourist arrivals accounted for 74% and the loss in international tourism receipts was estimated at USD 1.3 trillion [2]. As shown by the UNWTO data, 62 million travel jobs were lost in 2020, representing a drop of 18.5%, leaving just 272 million employees across the sector globally, compared to 334 million in 2019 [3]. Based on the latest data, global international tourist arrivals more than doubled (+130%) in January 2022 compared to 2021 [4]. Presently, international tourism is expected to continue its gradual recovery in 2022 (however, the war in Ukraine poses new challenges).

For many hospitality companies, this is the most difficult time in the entire history of their business. It should be remembered that this is not the first crisis to affect the tourism economy, although it has certainly never had such a character and magnitude [5]. Indeed, the sector has proved to be one of the most vulnerable to the negative impact of the pandemic and related restrictions. The instability in the tourism sectors since March 2020 has caused problems in maintaining a steady and predictable movement of people around the world, and the crisis caused by the outbreak of the pandemic has contributed to several key adverse outcomes. These include loss of liquidity for tourism businesses, difficulties in meeting tax obligations, seeking state assistance, etc.

The empirical objective of the article is to evaluate the performance of hotels in the crisis caused by the COVID-19 pandemic from the point of view of selected economic and operational indicators in hotels. In the literature on the subject, the crisis in the functioning of the company is analyzed through various approaches: as a consequence of certain events, a stage in the development of an enterprise, a pathology, or a process occurring in an enterprise [6]. In this article, the phenomenon of crisis is interpreted as a consequence of unplanned events occurring in the company’s environment, which disrupt or threaten the normal functioning of the company [7]. In order to illustrate the processes taking place, several indicators were selected to provide information on the financial condition of the company. These are the so-called Key Performance Indicators (hereinafter KPIs) serving as a numerical measurement tool that describes the performance of the hotel. The KPI analyses of hotels were carried out in five Polish cities considered to be important centres of the city break and meeting industry: Kraków, Poznań, Tri-City (Gdańsk, Gdynia, Sopot), Warsaw and Wrocław. Among these cities, due to its coastal location, only Tri-City represents the leisure segment in addition to city tourism.

The data on the negative economic effects of the pandemic published by various international institutions and research centers mainly include integrated indicators for the entire tourism economy, such as employment, share in GDP, number of tourists, etc. There is a small number of analyses of individual sectors, such as travel agencies or hotels. Hence, the proposed research is a case study of representations for city hotels throughout the country, in this case in Poland. The variability in individual KPI values during the pandemic illustrates not only the negative impact of the decline in the number of guests, but also the decline in the alleged profitability of hotels.

2. Literature Review

The outbreak of the global SARS-CoV-2 coronavirus pandemic determined the transformation of a large social and economic area, one of the main elements of international economic growth in recent decades [8].

In the literature, there are numerous analyses and studies of the COVID-19 pandemic and its impact on various economic spheres, including tourism. Some of the first studies focused on the country that was the source of the COVID-19 infection: China [9,10,11,12]. As suggested by Estrada et al. [10], the Chinese tourism sector can suffer of a decrease in demand in 75%. Noteworthy, in terms of global tourism, China is both an important tourist destination and a major source market. There are also studies of Sri Lanka [13], Italy [14], and Australia [15]. They present, to a varying extent, the effects of the development of the pandemic and its impact on the economies of these countries.

One of the sectors with the highest impact of the COVID-19 pandemic is hospitality [16,17,18]. As indicated by the results reported by Smith Travel Research (STR), the occupancy rates in accommodation facilities in March 2020 fell by as much as 96% in Italy, 68% in China, 67% in the UK, 59% in the US, and 48% in Singapore compared to 2019 figures [19]. Detailed studies indicate that the COVID-19 has a large negative effect on the operation of accommodation facilities, as reflected by the core indicators. The impact of the COVID-19 pandemic on the hotel industry has been examined from an international perspective [20,21,22] or countries, among others, in the US [23], China [24], India [25], Indonesia [26], Israel [27], and Poland [28,29]. The analysis included not only hotels but also short-term vacation rentals [30,31] or small lodging establishments [32]. Attention was also drawn to modelling the realisation of pent-up demand based on the relationship between the incoming traffic of online booking platforms in the hospitality sector and the volume of tourist arrivals in the context of the COVID-19 spread [33]. Finanacial anlyses [32,34] and economic indicators of hotels during the pandemic have also been described [23,28,35,36]. Importantly, the indicators used in the evaluation must be specific, measurable, achievable, relevant, and time-bound. This is the so-called SMART criterion, the scope of which has been described by, e.g., Shahin and Mahbod [37].

The assessment of hotel KPIs is important for surviving an economic crisis [38]. Measuring KPIs can help a company decide whether they are operating in an appropriate way and whether the hotel company’s performance is competitive or not. Analysing and monitoring a relevant set of KPIs can also help a hotel achieve its sales targets. The most commonly used indicators such as the occupancy percentage (OCC), ADR (average revenue), and RevPAR (revenue per room) should be analysed on a daily basis [39].

The time of the pandemic provoked considerations of the sustainability of the hotel industry described globally [40] and illustrated by the example of the hotel industry in Poland [41], as the hotel occupancy rates continued to fall [42,43].

From this point of view, sustainable hotel industry should apply to all areas and management tools, as the basic, practiced KPIs are not sufficient. HOTREC-a Confederation of National Hotel, Restaurant and Cafeteria [44] manifests numerous initiatives, inter alia, in the field of legal regulations and innovative concepts of management in the hotel industry. There is a tendency in the hotel industry to increase the interest in hotels that apply the principles of sustainable development [45,46]. More and more, guests who want to express their support for environmental protection choose hotels that declare a green economy and claim to be environmentally friendly [47]. Many facilities in the hospitality industry implement low-emission energy technologies to reduce the concentration of carbon dioxide in the atmosphere. The conducted research shows that the implementation of the Sustainable Development Goals during the COVID-19 pandemic was not endangered, and was even extended in social initiatives [41]. This is confirmed by the research on the attitudes of tourism stakeholders towards the goals of sustainable development in one of the cities analyzed in this article, which is Kraków [48], and the opinions of hotel industry leaders from Sweden, the USA, and Israel [49].

At the same time, the issues of sustainability should be viewed not only from the point of view of environmental protection but also tools and techniques for managing the enterprise. It was the period of the pandemic that proved that the analyzed indicators based solely on financial KPIs are short-sighted in crisis situations and do not fit into the concept of change management. Social and technological changes also justify the adjustment of analytical indicators [50].

The dynamic transformation of the epidemiological situation in individual countries was associated with the need for tourism companies to obtain state subsidies depending on the states’ concept of protecting the national market. The subsidies, known in Poland as editions of the so-called ‘anti-crisis shield’, were intended to sustain employment levels and maintain businesses for the duration of the freeze of their normal market activity. Hotels faced the challenge of having to redefine their business models.

3. Operation of Hotels during the Pandemic

Prior to the announcement of the pandemic, the hospitality market in Poland was in a booming phase and hoteliers were experiencing a period of prosperity. Between 2015 and 2019 alone, the number of guests in hotels increased by 6 million, including foreigners by 1 million and the number of nights provided by more than 12 million from 32.7 to 44.8 million [51]. Unfortunately, the trend was abruptly interrupted with the restrictions introduced by successive decisions of the authorities of individual countries, leading to a complete halt in international tourism.

The hotel sector was therefore one of the most negatively affected by the COVID-19 pandemic through the administrative restrictions on operations and the drastic reduction in both domestic and international demand. According to Statistics Poland, there were 17.9 million tourists staying in all tourist accommodation establishments in 2020, which was almost half the number of tourists from the previous year. Hotels also suffered from the administrative restrictions on catering operations and a drop in activity to essentially zero affected the MICE segment during the pandemic. In 2020, after many years of uninterrupted growth, there was a decline in the number of accommodation establishments (by 8.5% y-o-y) and beds offered in these establishments (by 6.1% y-o-y) [51]. In the tourist travel segment, the decrease in demand for hotel services was related to the fear of infection and a reduction in trips and stays by private individuals. It is worth noting that even in the 2020 holiday season, i.e., during the relative weakening of the pandemic, small facilities (houses, holiday cottages, often located outside tourist destinations) were very popular, while there was less interest in stays in hotels, which naturally generate concentrations of people.

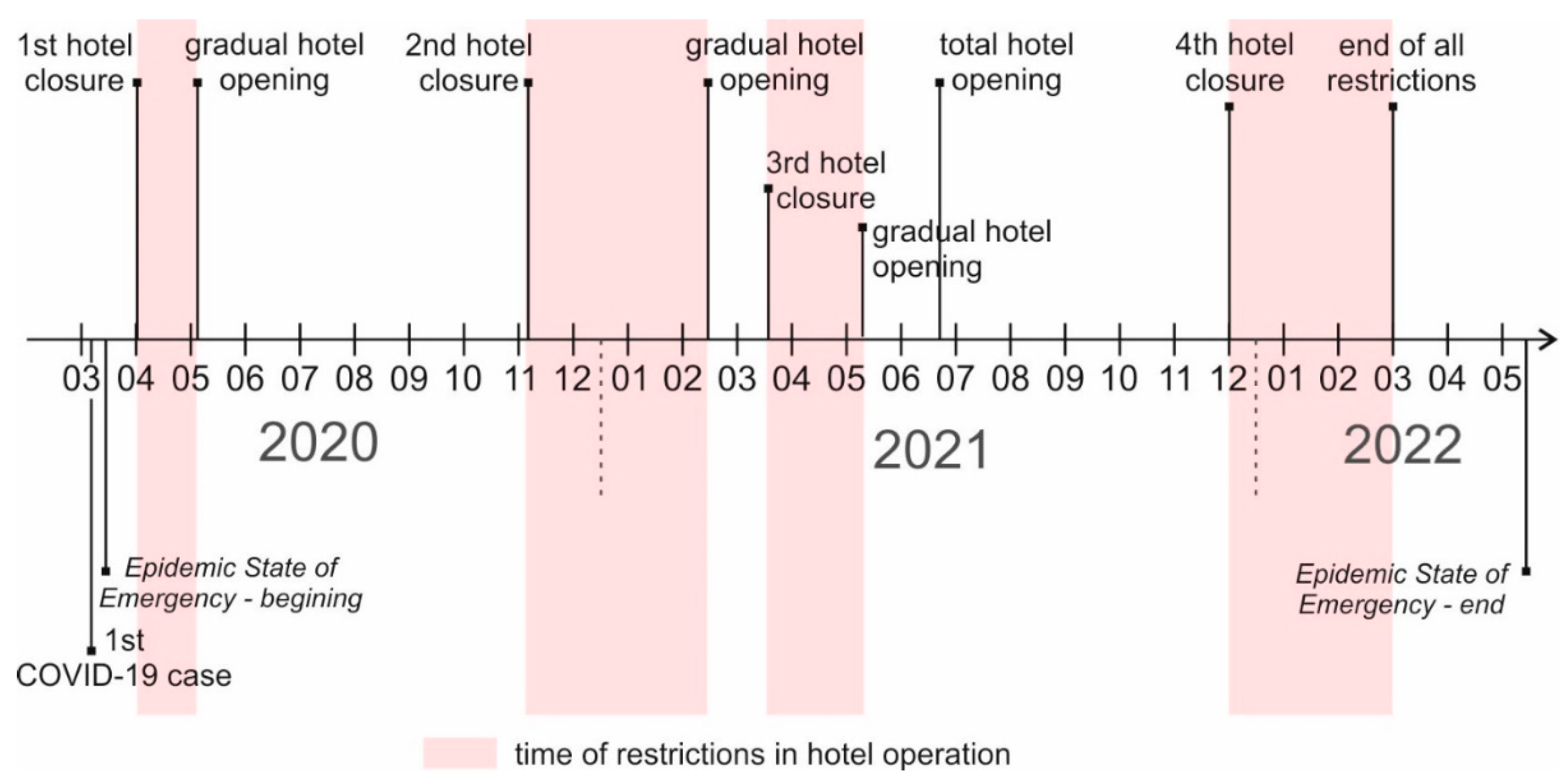

In Poland, the first case of COVID-19 was reported on 4 March 2020, and the government declared an Epidemic State of Emergency on 14 March. The first major restrictions on hotel operations were introduced between 1 April and 3 May 2020, when facilities mostly had to be closed. From 4 May 2020, there was a gradual process of ‘unfreezing’ hotel operations (Figure 1).

As early as in April 2020, interviews on the economic state of the hotel sector began to be published (mainly by the Economic Chamber of Polish Hotel Management publishing the results of surveys conducted among its members every 2–3 months on its website). Due to different methods and sample sizes, they cannot be comparable; nevertheless, they show the attitude and state of the hotel industry at different moments of the pandemic and formal restrictions on movement, opening of services, and flight connections. The data collected reveal the scale of losses, demand, areas of expected government assistance, the labour market situation, or prospects for restart, with each of the studies conducted under slightly different pandemic circumstances and constraints [52].

In autumn 2020, the exponential increase in infections recorded from the beginning of October led to the return of the restrictions. As of 7 November 2020, hotels were only allowed to accommodate guests using hotel services as part of business travel. Hotel restaurants remained closed, and meals were only served to rooms. The data on accepted bookings for the following months confirmed the high uncertainty on the hotel services market, the tendency to postpone purchasing decisions until the last minute, and the lack of visible prospects for a recovery in business traffic.

The decision to open hotel facilities to all guests was not taken by the government until February 2021, but under a limited sanitation regime: 50% of rooms available, closed restaurants (meals served in the room), pools open while maintaining 1.5 m distancing, closed saunas, etc.

In spring 2021, the epidemic situation in Poland continued to deteriorate and the hotels had to suspend their operations again. From 8 May 2021, the hotels were opened to guests with a maximum occupancy of 50% and closed restaurants and wellness and spa areas. From 28 May, restaurants were opened under a strict sanitary regime (maximum occupancy of 50%) and special events were allowed inside the facilities (limit of up to 50 people). With the start of the summer holidays, the government reduced many of the restrictions. The occupancy limits in hotels and restaurants increased to 75%—the limits did not apply to groups of young people under the age of 12 and fully vaccinated persons.

The restrictions persisted until 1 December 2021, when the limit of persons in hotels was reduced to 50% (vaccinated persons were not included in this number). These regulations were tightened from 15 December, when the limit of unvaccinated persons allowed in the facility was reduced to 30%. They were in force until the end of February 2022. As of 1 March 2022, all hotel occupancy limits were lifted. However, new challenges arose a few days earlier, as the war in neighbouring Ukraine began.

4. Material and Methods

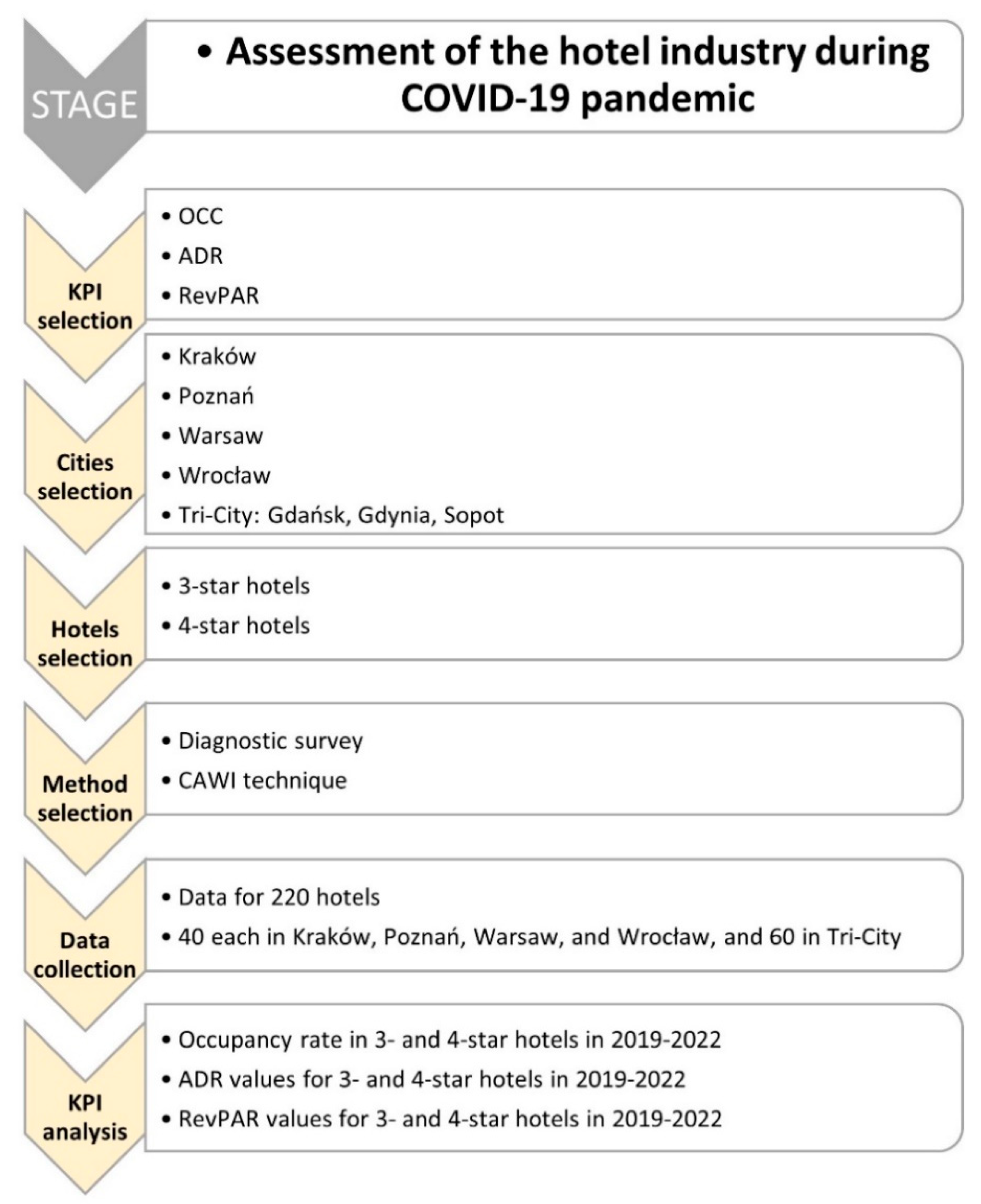

The research process of the assessment of hotel operations during the crisis caused by the COVID-19 pandemic was divided into six main stages: (1) KPI selection; (2) city selection; (3) hotel selection; (4) method selection; (5) data collection; (6) KPI analysis (Figure 2). These stages are described below.

4.1. KPI Selection

The quantifiable measures that allow a company to assess the revenue management strategies are the Key Performance Indicators (KPIs). Therefore, the assessment was carried out using three of the main economic and operational indicators [23,28,39,53,54,55,56]:

- (1)

- OCC (Occupancy)—the room occupancy rate (expressed as a percentage), indicating the ratio of the number of rented rooms to the nominal number of rooms (the total number of rooms prepared for tourists on each day of hotel operation) [57]:

OCC is one of the most popular KPI’s in the hotel industry for revenue management, highlighting how much of the available space in a hotel is actually being utilised. However, it should be used in conjunction with other metrics because the goal is to maximise revenue, not occupancy rate. For this reason, the occupancy rate should always be viewed in context, alongside average daily rate and revenue per available room.

- (2)

- ADR (Average Daily Rate)—an indicator of the average daily income per occupied room per day excluding breakfast [58]:

By using ADR, hotel management can know the average price paid per room on a specific day and monitor trends over a longer time frame. It should be noted that only rooms that were actually available for sale should be included in the calculation (rooms used by employees or complimentary rooms that were allocated to guests should not be taken into account).

- (3)

- RevPAR (Revenue Per Available Room)—an indicator of the level of revenue per available room in relation to the occupancy of the facility [59]:

RevPAR is a metric used in the hospitality industry to assess a property’s ability to fill its available rooms at an average rate. It allows for obtaining a more accurate and broad picture of the hotel’s performance and helps to see how much revenue the hotel made within a certain period of time.

Analysis of the above indicators provides a broader view of the hotel’s financial performance and thus its ability to operate on the market. In contrast, it does not indicate the effectiveness of the full management, as it only indicates acquired guests and not potential ones. The analysed indicators are certainly not the only ones that allow management accounting, but even a slight increase in the occupancy level (OCC) or average price (ADR) yields a significant increase in the revenue on an annual basis. Given the hotel indicators, it is possible to keep track of deviations that affect the hotel’s profitability or cost structure.

4.2. Cities Selection

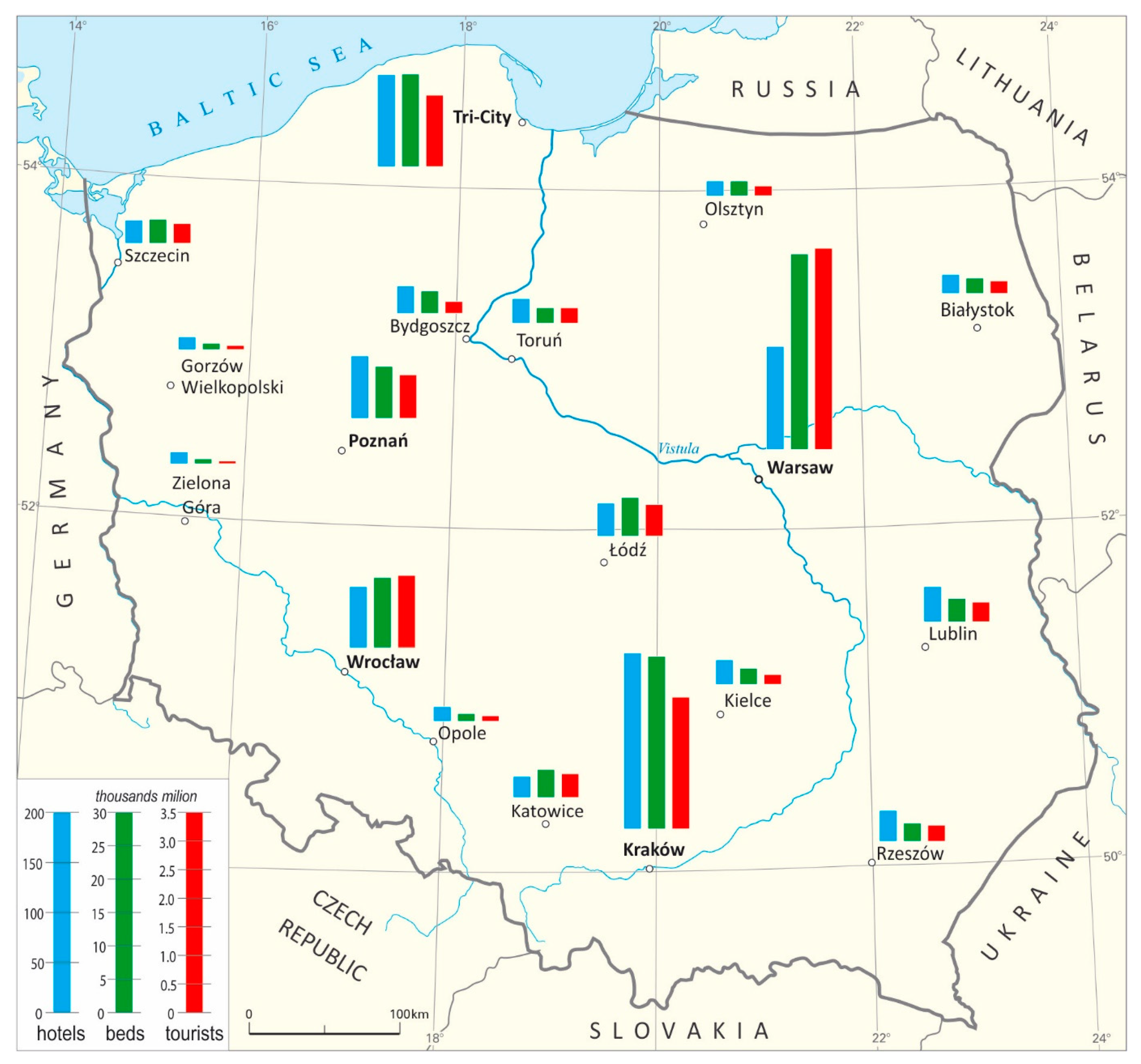

The research was conducted in five Polish cities (Kraków, Poznań, Warsaw, Wrocław, and Tri-City—the metropolitan area of three cities: Gdańsk, Gdynia, Sopot), where the largest number of hotels, bed places, and accommodated tourists occur, according to Statistics Poland data [60] (Figure 3, Table 1).

4.3. Hotels Selection

As of 31 July 2019, the number of tourist accommodation facilities in Poland amounted to 19.2 thousand facilities. The structure of the establishments was dominated by guest rooms and agrotourism lodgings, which together constituted almost 60% of all tourist accommodation facilities. As a rule, these are small facilities with several bed places. The next largest group of facilities was hotels, whose share was 14%, but these offer over 32% of all facilities bed places [60].

The size of the hotel sector in Poland amounted to over 2635 hotels (of which nearly 75% in cities), offering almost 290,000 beds. For detailed analyses, three- and four-star hotels were selected, which both offer the largest number of beds (which is 71%) and are the most frequently chosen category of hotels by tourists nationally (which is 72%) and in the individual cities (Table 1).

4.4. Method Selection

To collect data, needed to calculate the KPIs, a diagnostic survey using the Computer-Assisted Website Interview (CAWI) technique was applied. CAWI is considered a quantitative method in which numeric parameters are determined in given units so the subject of the investigations can be characterized. It is currently the most quickly developing survey method. It enables the data to be collected much cheaper and quicker in comparison to traditional methods [61,62]. The choice of survey method was determined by the constraints of the pandemic, the ability to easily reach a large number of respondents, and the speed of obtaining results. The use of the CAWI technique to survey businesses has additional justification. According to Statistics Poland [63], 100% of businesses with at least 10 employees and providing accommodation and catering services have internet access.

Surveys were sent to the management of three- and four-star hotels in selected cities.

4.5. Data Collection

The data were collected monthly in two study periods:

- January 2019 to February 2020—the period before the pandemic was declared;

- March 2020 to February 2022—the entire duration of the pandemic in Poland.

The research covered 220 hotels (8.4% of all hotels in Poland), 40 each in Kraków, Poznań, Warsaw, and Wrocław, and 60 in Tri-City. Two survey forms were received back from each hotel (the first covered the period before the announcement of the pandemic and the second covered the entire duration of the pandemic in Poland), resulting in a total of 440 questionnaires to be analysed.

4.6. KPI Analysis

On the basis of data and information obtained from the hotels’ management KPIs have been calculated by the Authors. KPIs analysis: OCC, ADR and RevPaR for three- and four-star hotels, for the period 2019–2022 are presented in Chapter 5. Results—hotel economic indicators in the COVID-19 pandemic.

5. Results—Hotel Economic Indicators in the COVID-19 Pandemic

Clearly, the constraints described above have had an impact on the economic performance of the hotels, which is reflected in the economic indicators achieved.

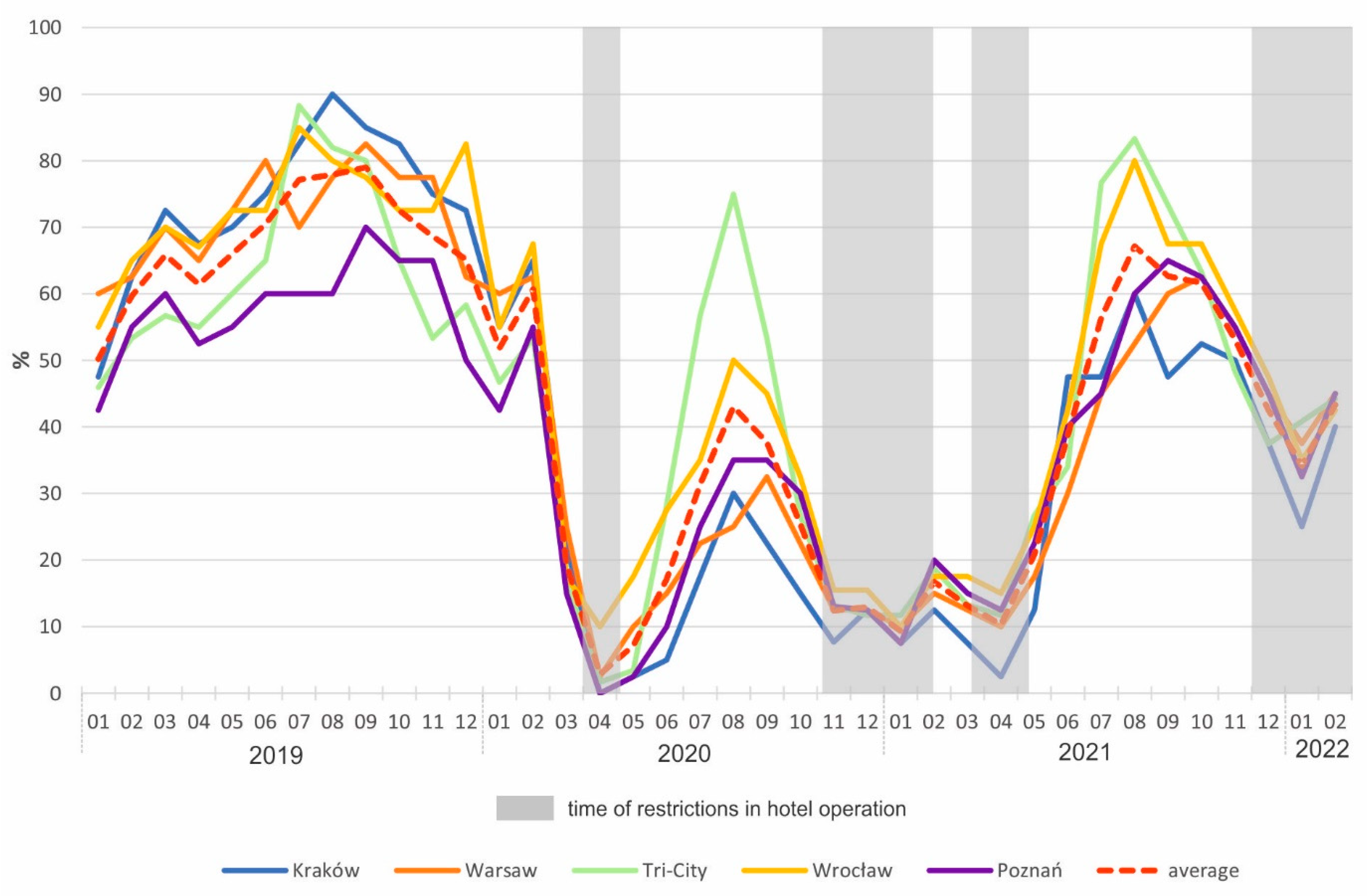

The first strong collapse in hotel occupancy (OCC) was already recorded in March 2020 (Figure 4)—from 61.7% in February to 19.4% (average for all cities). The comparison of these figures to data from the previous year demonstrated a large difference, as the OCC in March 2019 was on average 66.3%. Already in April, the OCC fell to an average of 2.8% (the lowest value—at 0%—was recorded in Poznań and Kraków, and the highest was noted in Wrocław 10.0%). A slight increase in the OCC of the hotels to 7.2% and 17.2% on average was recorded in May and June 2020, respectively. Already in this period, differences between individual cities are noticeable, and results above the average were recorded in Tri-City and Wrocław.

Summer 2020 was associated with the improvement of the OCC in the hotels of the cities in question. In the following three months of July–September, the average hotel occupancy rate was over 40% (max. average value—August 2020—43%). During this period, however, significant disparities between the cities were noticeable. The highest OCC, at a level similar to the pre-pandemic period (75%), was recorded by the hotels in Tri-City.

The following autumn-winter months (November 2020 to April 2021) were again a period of a significant decrease in the OCC, with the rate at a level of several per cent (not exceeding 20%), compared to the 50–70% achieved in 2019 over a comparable period.

From May 2021 onwards, an increase in occupancy rates was recorded to a value of 20.8% in May and 38.8% in June. It is noticeable that this increase was very similar in all the analysed cities. The further increases in the OCC values were also associated with the holiday months, with its average increasing to 56.3% in July and 67.2% in August. Although the average value was significantly lower than in 2019, the values recorded in two cities: Wrocław (80.0%) and Tri-City (83.3%) were at levels similar to the pre-pandemic period.

From September 2021, a gradual decline in the hotel OCC was observed, with an average of 34.2% in January 2022 and the lowest values recorded in Kraków. In February, the occupancy rate increased. The average OCC values for the consecutive years were 67.8% in 2019, 26.8% in 2020, and 37.7% in 2021.

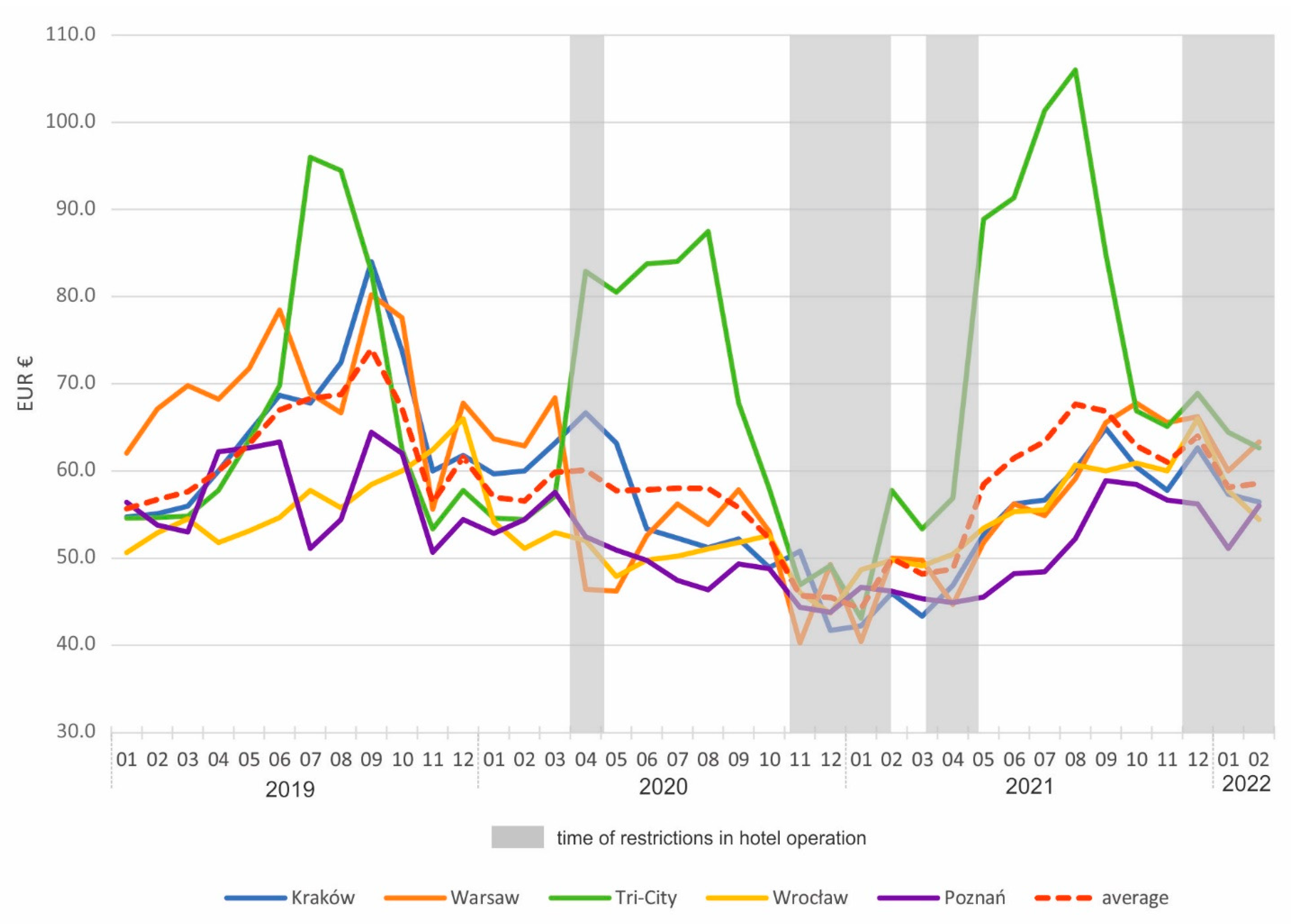

Another analysed indicator—ADR, i.e., the average income received per room rented (excluding breakfast), is determined independently of the occupancy of the property. The average ADR determined for 2019 at EUR 63.1 (For simplicity, a rate of 1 EUR (EUR) = 4.5 PLN was used) fell to EUR 55.3 in 2020. In 2021, the ADR increased to EUR 58.0. The analysis of the changes in the ADR occurring with the course of the pandemic showed that its value decreased successively from April 2020 (Figure 5). In 2020, there was no increase in the ADR value in the spring-summer months (May–September), in contrast to 2019. The first increase in its value was recorded in February and the next in May 2021. The increasing ADR indicated an improvement in the situation, but the values achieved were still lower than in 2019.

The comparison of the average ADR values in the different months of the analysed years revealed that only in the first four months of 2020 the ADR was comparable to the results from 2019, which is related to the fact that the pandemic outbreak occurred in March. From May 2020 onwards, the ADR value was lower in each month, compared to the previous results, over the entire subsequent year. The ADR reached a value close to that of 2020 only in June 2021, and a gradual increase in the indicator value was noticeable from this point onwards. A breakthrough month was November 2021, as the ADR value (EUR 61.1) was higher than the corresponding value in the two previous years (2019—EUR 56.4; 2020—EUR 45.8). From then on (until February 2022), the highest month-to-month ADR value was recorded.

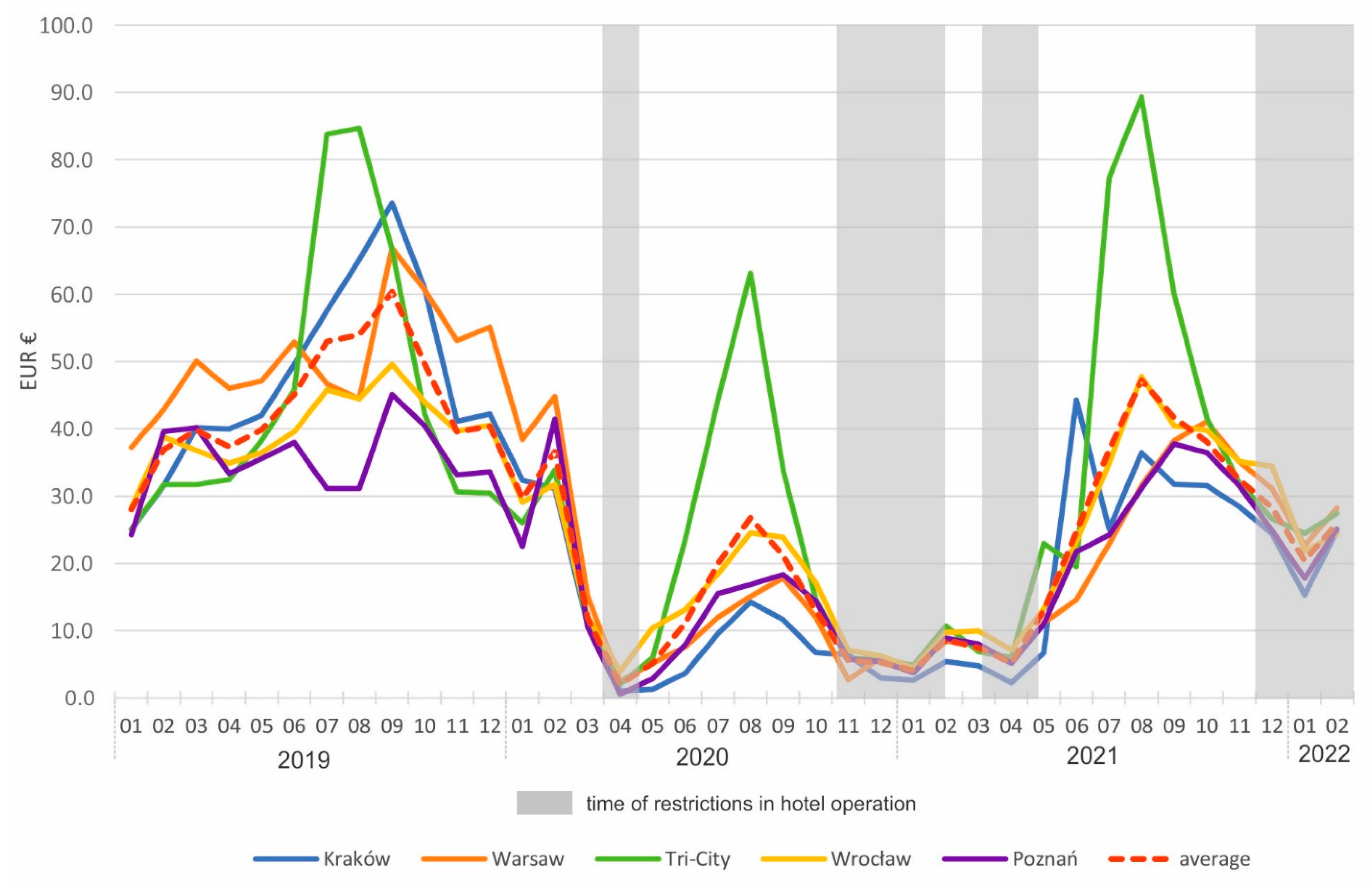

The last of the analysed indicators RevPAR, i.e., the revenue per available room, is an indicator of performance in the hotel industry. From March 2020 to June 2021, the average RevPAR was below even the lowest values recorded for 2019 (in January and February—EUR 28.0 and EUR 36.9, respectively). July 2021 was the first month in which the average index exceeded the minimum values recorded for 2019.

RevPAR first fell dramatically to EUR 11.8 in March and as low as EUR 2.0 in April (Figure 6). In the following months, it gradually increased, reaching a maximum average value of EUR 26.7 in 2020. The turn of 2020 and 2021 (November–April) was a period when RevPAR exceeded EUR 11 in none of the analysed cities. From May 2021, a gradual increase in RevPAR was noticeable, reaching a maximum average value of EUR 47.3 in August 2021.

6. Discussion

From the day of the introduction of the epidemic alert in Poland, a sharp drop in new bookings and a significant increase in cancellations of existing reservations began to be recorded. Not only individual stays but also group bookings and conferences were cancelled. Therefore, already at the beginning of the pandemic, the Polish hotel industry experienced its negative effects [28], as it did in other countries [23,38]. At the time of the greatest restrictions, both the USA [23,56] and Poland recorded huge drops in KPIs. Polish hotels recorded an approximately 95% decline in the OCC and RevPAR values. Hotels in cities dominated by foreign tourism suffered the greatest losses. However, it should be noted that Wrocław showed the highest occupancy rate during this period, among not only all major cities in Poland but also in Central and Eastern Europe [64,65]. As suggested in the trade magazine [66], high rates may have been achieved thanks to accommodated foreign workers employed in various investments in the city, who could not back home because of closed borders and largely restricted international flights.

The gradual ‘unfreezing’ of hotels operation was s slow process [67], especially since international tourist traffic was virtually non-existent. In the months that brought a considerable loosening of the restrictions—the holiday period (July–August)—the occupancy rates improved, as clearly seen in Tri-City. These were the highest results not only in Poland but also in the entire CEE region. Following the STR SHARE Center data [65], it was found that none of the other areas surveyed by the STR managed to exceed an occupancy rate above 35%. However, the lowest occupancy rates were achieved by the hotels in Kraków and Warsaw, whose market was based on foreign guests. The disparity between the hotel industry in the coastal tourist regions and the city hotel industry was noted again in the summer of 2021. The hotel occupancy rates significantly increased in the Tri-City (even surpassed the pre-pandemic statistics), which, in conjunction with high interest in a holiday by the Polish seaside, drove the prices up and led to a 50% increase in RevPAR. Data showed how psychological factors, i.e., the fear of infection and the increased caution of foreign tourists as well as the various restrictions imposed also in other countries, have deterred a significant proportion of tourists from previous holiday activity. These circumstances were also noted among Polish tourists who, according to the report [68], have chosen domestic holidays and spent their summer holidays exclusively in the country site. The diversity of indicators between coastal regions and cities clearly showed how the dynamic is more heterogeneous than ever depending on the region and the time of year. Such a process was also noticed during the pandemic in the French hotel industry [69].

The autumn–winter period was another very difficult time for the hotel industry, also in Poland. According to estimates [70], the number of tourists was significantly smaller and resulted in a drop in the OCC. Surveyed hotels in the vast majority, declared that they would have difficulties in maintaining liquidity and did not expect to make an operating profit earlier than the end of 2021. As many as 97% of the hotels predicted a return to the 2018–2019 revenue levels no earlier than in 2022 [71]. The optimistic time for the hotel industry came to an end with the introduction of strict regulations which were in force until the end of February 2022.

By observing the course of KPIs during the pandemic, hoteliers became aware of the impact of factors related to their competitive environment on economic outcomes. The Economic Chamber of Polish Hotel Management put forward some general demands to support and sort out issues with the greatest relevance to the hotel industry in Poland [72] and worldwide. These include the exclusion of hotels from the so-called minimum tax, the introduction of a zero VAT rate for hotel services, the updating of categorisation regulations and the increased protection of the name ‘hotel’, the regulation of short-term rentals, the outlawing of so-called narrow clauses used by online booking portals (OTAs), quality certifications, changes in employee rights, the liberalisation of running businesses, or the simplification of public procurement law. This means extending the analyses of hotel productivity to include non-economic indicators as well. Among these indicators, the ones reflecting changes and reactions on the demand side should be taken into account to a greater extent, which can be seen again in some countries (the Baltic states, the Czech Republic, and even Austria) after the outbreak of the war in Ukraine.

7. Conclusions

Prior to the announcement of the pandemic, the hospitality market was in a dynamic phase and hoteliers were experiencing a period of prosperity. Unfortunately, the trend was abruptly interrupted. The restrictions introduced had a negative impact primarily on international and domestic tourism and, consequently, on the entire hotel industry.

Based on the analyses carried out, it was concluded that:

- –

- 2020–2021 proved to be the most difficult period for the hospitality industry in its entire history. Indeed, the sector has proven to be one of the most vulnerable to the negative impact of the pandemic and its associated restrictions.

- –

- a clear discrepancy has emerged between the urban hotel industry, based primarily on foreign guests and business tourism, and the hotel industry in coastal tourist regions where domestic leisure tourists predominate.

- –

- the gradual increase in the OCC index in 2022 cannot be the basis for assessing the economic condition of hotels, because the losses incurred in the pandemic and measured by, for example, RevPAR will require a longer time perspective.

It was also found that KPI indicators (resulting from demand volatility during pandemic) are not fully sufficient for assessing hotel productivity and management tools. This underscores the need to increasingly utilise competitor-based revenue KPI benchmarks [73] or balanced scorecard [74]. Attention is also drawn to the need for revenue management flexibility in order to convert the revenue indicator into profit. It is even proposed to develop a value stream mapping (VSM) model based on six key drivers: organisational culture, demand forecasting, dynamic distribution channels, competition breakdown, dynamic and customised pricing, and daily reviewing [75].

Studies conducted during the COVID-19 pandemic in hotels in Poland and elsewhere, e.g., in Hungary [38], indicate that financial KPIs such as ADR and RevPAR are still important in the assessment of hotel performance. However, it has been noted that it is worthwhile to extend the analyses with non-economic indicators, e.g., employee satisfaction and loyalty [38], if hotel managers wish to ensure high quality of services and achieve high levels of guest satisfaction and productivity at the same time [76,77].

8. Limitations and Future Work

The research was conducted during the COVID-19 pandemic and the presented indicators relate to the crisis period, which is atypical for hotel operations. Only a representative group of three-star and four-star hotels were covered by them, as the majority of hotels in lower categories do not run revenue management and, consequently, do not calculate the RevPAR index. The choice of hotels has been limited to the most important tourist cities in Poland. Only economic KPIs were analyzed. In the future, in the post-co-vid period, similar research should be continued, supplemented with the creation of non-economic indicators, extended by hotel analyses to include five-star hotels and those of a lower standard, and also those located in other cities with different functions.

Author Contributions

Conceptualization, R.K. and M.W. Methodology, R.K. and M.W. Formal analysis, R.K. and M.W. Resources, R.K. and M.W. Writing—original draft preparation, R.K., M.W., B.W. and Z.K. Writing—review and editing, R.K., M.W., B.W. and Z.K. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Not applicable.

Acknowledgments

We are particularly grateful to the management of hotels in Poland for supporting the research process.

Conflicts of Interest

The authors declare no conflict of interest.

References

- COVID-19 and the Tourism Sector. European Parliament (EP). Available online: https://www.europarl.europa.eu/RegData/etudes/ATAG/2020/649368/EPRS_ATA(2020)649368_EN.pdf (accessed on 2 June 2021).

- 2020: A Year in Review. COVID-19 and Tourism. UNWTO. Available online: https://www.unwto.org/covid-19-and-tourism-2020 (accessed on 22 June 2021).

- Economic Impact Reports. WTTC. Available online: https://wttc.org/Research/Economic-Impact (accessed on 22 June 2021).

- Tourism Enjoys Strong Start to 2022 While Facing New Uncertainties. Barometer UNWTO (25 March 2022). Available online: https://www.unwto.org/taxonomy/term/347 (accessed on 9 May 2022).

- Gössling, S.; Scott, D.; Hall, C.M. Pandemics, tourism, and global change: A rapid assessment of COVID-19. J. Sustain. Tour. 2020, 29, 1–20. [Google Scholar] [CrossRef]

- Sochoń, M. Podatność przedsiębiorstwa na kryzys—Koncepcja ostrzegania przed zagrożeniem wystąpienia kryzysu w przedsiębiorstwie. Mod. Manag. Rev. 2017, 24, 179–189. Available online: http://doi.prz.edu.pl/pl/pdf/zim/304 (accessed on 22 June 2021). [CrossRef]

- Oldcorn, R. Management, 2nd ed.; Palgrave Macmillan: London, UK, 1989; ISBN 9780333487969. [Google Scholar]

- Smoliński, M.; Zakrzewska, L. Normalność 2.0, Harvard Business Review Polska (1 August 2020). Available online: https://www.ican.pl/a/normalnosc-20/DKRXcLEmh (accessed on 22 June 2021).

- Ayittei, F.; Ayittei, M.; Chiwero, N.; Kamasah, J.; Dzuvor, C. Economic impacts of Wuhan 2019-nCoV on China and the world. J. Med. Virol. 2020, 92, 473–475. [Google Scholar] [CrossRef]

- Estrada, M.; Park, D.; Lee, M. How a Massive Contagious Infectious Diseases Can Affect Tourism, International Trade, Air Transportation, and Electricity Consumption? The Case of 2019 Novel Coronavirus (2019-nCoV) in China. SSRN Electron. J. 2020, 3540667. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3540667 (accessed on 16 June 2020). [CrossRef]

- Hoque, A.; Shikha, F.A.; Hasanat, M.W.; Arif, I.; Hamid, A.B.A. The Effect of Coronavirus (COVID-19) in the Tourism Industry in China. Asian J. Multidiscip. Stud. 2020, 3, 52–58. Available online: https://asianjournal.org/online/index.php/ajms/article/view/213/96 (accessed on 16 June 2021).

- McCartney, G. The impact of the coronavirus outbreak on Macao. From tourism lockdown to tourism recovery. Curr. Issues Tour. 2020, 24, 2683–2692. [Google Scholar] [CrossRef]

- Ranasinghe, R.; Damunupola, A.; Wijesundara, S.; Karunarathna, C.; Nawarathna, D.; Gamage, S.; Ranaweera, A.; Idroos, A.A. Tourism after Corona: Impacts of COVID-19 Pandemic and Way forward for Tourism, Hotel and MICE Industry in Sri Lanka. SSRN Electron. J. 2020. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3587170 (accessed on 18 June 2021). [CrossRef]

- Panarese, P.; Azzarita, V. The Impact of the COVID-19 Pandemic on Lifestyle: How Young people have Adapted Their Leisure and Routine during Lockdown in Italy. Young 2021, 29, S35–S64. [Google Scholar] [CrossRef]

- Folinas, S.; Metaxas, T. Tourism: The Great Patient of Coronavirus COVID-2019. Int. J. Adv. Res. 2020, 4, 365–375. Available online: https://mpra.ub.uni-muenchen.de/103515/ (accessed on 18 June 2021). [CrossRef]

- Kaushal, V.; Srivastava, S. Hospitality and tourism industry amid COVID-19 pandemic: Perspectives on challenges and learnings from India. Int. J. Hosp. Manag. 2020, 92, 103012. [Google Scholar] [CrossRef]

- Aigbedo, H. Impact of COVID-19 on the hospitality industry: A supply chain resilience perspective. Int. J. Hosp. Manag. 2021, 98, 103012. [Google Scholar] [CrossRef]

- Burhan, M.; Salam, M.T.; Hamdan, O.A.; Tariq, H. Crisis management in the hospitality sector SMEs in Pakistan during COVID-19. Int. J. Hosp. Manag. 2021, 98, 103037. [Google Scholar] [CrossRef]

- Sorells, M. Data Shows Severe Impact of Coronavirus on Global Hospitality Industry. Phocus Wire (26 March 2020). Available online: https://www.phocuswire.com/str-global-hotel-data-march-21-coronavirus (accessed on 16 June 2020).

- Sanabria-Díaz, J.M.; Aguiar-Quintana, T.; Araujo-Cabrera, Y. Public strategies to rescue the hospitality industry following the impact of COVID-19: A case study of the European Union. Int. J. Hosp. Manag. 2021, 97, 102988. [Google Scholar] [CrossRef] [PubMed]

- Duarte Alonso, A.; Kok, S.K.; Bressan, A.; O’Shea, M.; Sakellarios, N.; Koresis, A.; Buitrago Solis, M.A.; Santoni, L.J. COVID-19, aftermath, impacts, and hospitality firms: An international perspective. Int. J. Hosp. Manag. 2020, 91, 102654. [Google Scholar] [CrossRef] [PubMed]

- Ostrowska-Tryzno, A.; Pawlikowska-Piechotka, A. Tourism, the hotel industry at the time of the COVID-19 pandemic. Sport Tur. Srod. Czas. Nauk. 2022, 5, 139–152. [Google Scholar] [CrossRef]

- Ozdemir, O.; Dogru, T.; Kizildag, M.; Mody, M.; Suess, C. Quantifying the economic impact of COVID-19 on the U.S. hotel industry: Examination of hotel segments and operational structures. Tour. Manag. Perspect. 2021, 39, 100864. [Google Scholar] [CrossRef]

- Hao, F.; Xiao, Q.; Chon, K. COVID-19 and China’s Hotel Industry: Impacts, a Disaster Management Framework, and Post-Pandemic Agenda. Int. J. Hosp. Manag. 2020, 90, 102636. [Google Scholar] [CrossRef]

- Nair, G.K.; Hameed, S.; Prasad, S. Ready for recovery: Hoteliers’ insights into the impact of COVID-19 on the Indian hotel industry. Res. Hosp. Manag. 2021, 11, 199–203. [Google Scholar] [CrossRef]

- Japutra, A.; Situmorang, R. The repercussions and challenges of COVID-19 in the hotel industry: Potential strategies from a case study of Indonesia. Int. J. Hosp. Manag. 2021, 95, 102890. [Google Scholar] [CrossRef]

- Shay, R.; Cohen, E. The COVID-19 pandemic effect on stock prices of leading public chain hotels in Israel. In Reviving Tourism, in the Postpandemic Era, 1st ed.; Evangelos, C., Anestis, F., Eds.; School of Economics and Business, International Hellenic University: Sindos, Greece, 2022. [Google Scholar]

- Napierała, T.; Leśniewska-Napierała, K.; Burski, R. Impact of Geographic Distribution of COVID-19 Cases on Hotels’ Performances: Case of Polish Cities. Sustainability 2020, 12, 4697. [Google Scholar] [CrossRef]

- Piechaczek, A. Polish Domestic Tourism in the Face of SARS-CoV–2 Pandemic. Folia Oeconomica Acta Univ. Lodz. 2021, 2, 29–42. [Google Scholar] [CrossRef]

- Soh, J.; Seo, K. An Analysis of The Impact of Short-Term Vacation Rentals on the Hotel Industry. J. Hosp. Tour. Res. 2021. [Google Scholar] [CrossRef]

- Medeiros, M.; Xie, J.; Severt, D. Exploring relative resilience of Airbnb and hotel industry to risks and external shocks. Scand. J. Hosp. Tour. 2022, 22, 274–283. [Google Scholar] [CrossRef]

- Rivera, M.; Kizildag, M.; Croes, R. COVID-19 and small lodging establishments: A break-even calibration analysis (CBA) model. Int. J. Hosp. Manag. 2021, 94, 102814. [Google Scholar] [CrossRef]

- Kostynets, V.; Kostynets, I.; Olshanska, O. Pent-up demand’s realization in the hospitality sector in the context of COVID-19. J. Int. Stud. 2021, 14, 89–102. [Google Scholar] [CrossRef]

- Wieczorek-Kosmala, M. COVID-19 impact on the hospitality industry: Exploratory study of financial-slack-driven risk preparedness. Int. J. Hosp. Manag. 2021, 94, 102799. [Google Scholar] [CrossRef]

- Lock, S. Impact of COVID-19 on Hotel RevPAR in Europe 2020. Statista (10 November 2021). Available online: https://www.statista.com/statistics/1128655/covid-19-change-in-trevpar-europe/ (accessed on 9 May 2022).

- Lock, S. Global Change in Travel and Tourism Revenue due to COVID-19 2019–2020. Statista (7 January 2022). Available online: https://www.statista.com/forecasts/1103426/covid-19-revenue-travel-tourism-industry-forecast (accessed on 9 May 2022).

- Shahin, A.; Mahbod, M.A. Prioritization of key performance indicators. An integration of analytical hierarchy process and goal setting. Int. J. Product. Perform. Manag. 2007, 56, 226–240. [Google Scholar] [CrossRef]

- Németh, M.; Gyurácz-Németh, P. Key performance indicators before and during/after the “COVID-19 times” in the Hungarian hotel sector. In Reviving Tourism, in the Postpandemic Era, 1st ed.; Evangelos, C., Anestis, F., Eds.; School of Economics and Business, International Hellenic University: Sindos, Greece, 2022; ISBN 978-618-5630-06-5. [Google Scholar]

- Srivastava, N.; Maitra, R. Key performance indicators (KPI) in the hospitality industry: An emphasis on accommodation business of 5 star hotels of National Capital Region. Int. J. Tour. Hosp. Res. 2016, 2, 34–40. [Google Scholar] [CrossRef]

- Chang, L.-C.; McAleer, M.; Ramos, V.A. Charter for Sustainable Tourism after COVID-19. Sustainability 2020, 12, 3671. [Google Scholar] [CrossRef]

- Dahlke, P.; Orfin-Tomaszewska, K.; Sosnowski, P. Sustainability in the Hospitality Industry in the Shadow of the COVID-19 Pandemic: A Case Study of the Hospitality Industry in Poland. Available online: https://www.e3s-conferences.org/articles/e3sconf/abs/2021/83/e3sconf_dsdm2021_08002/e3sconf_dsdm2021_08002.html (accessed on 21 May 2022).

- Krishnan, V.; Mann, R.; Seitzman, N.; Wittkamp, N. Hospitality and COVID-19: How Long Until ‘No Vacancy’ for US Hotels? (10 June 2020). Available online: https://www.mckinsey.com/industries/travel-logistics-and-infrastructure/our-insights/hospitality-and-covid-19-how-long-until-no-vacancy-for-us-hotels (accessed on 21 May 2021).

- Hoisington, A. 5 Insights about How the COVID-19 Pandemic Will Affect Hotels. Hotel Management (17 March 2020). Available online: https://www.hotelmanagement.net/own/roundup-5-insights-about-how-covid-19-pandemic-will-affect-hotels (accessed on 21 May 2021).

- Annual Report 2020–2021. HOTREC, June 2021. Available online: https://www.hotrec.eu/wp-content/customer-area/storage/f365e34316edd2cbe372d1bbfb08a372/HOTREC-Annual-Report-20-21.pdf (accessed on 10 September 2022).

- Barber, N.A. Profiling the Potential “Green” Hotel Guest: Who Are They and What Do They Want? J. Hosp. Tour. Res. 2012, 38, 361–387. [Google Scholar] [CrossRef]

- Peng, N.; Chen, A. Luxury Hotels Going Green—The Antecedents and Consequences of Consumer Hesitation. J. Sustain. Tour. 2019, 27, 1374–1392. [Google Scholar] [CrossRef]

- Kim, Y.J.; Kim, W.G.; Choi, H.-M.; Phetvaroon, K. The Effect of Green Human Resource Management on Hotel Employees’ Eco-Friendly Behavior and Environmental Performance. Int. J. Hosp. Manag. 2019, 76, 83–93. [Google Scholar] [CrossRef]

- Szromek, A.R.; Kruczek, Z.; Walas, B. Stakeholders’ Attitudes towards Tools for Sustainable Tourism in Historical Cities. Tour. Recreat. Res. 2021, 1–13. [Google Scholar] [CrossRef]

- Shapoval, V.; Hägglund, O.; Pizam, A.; Abraham, V.; Carlbäck, M.; Nygren, T.; Smith, R.M. The COVID-19 pandemic effects on the hospitality industry using social systems theory: A multi-country comparison. Int. J. Hosp. Manag. 2021, 94, 102813. [Google Scholar] [CrossRef] [PubMed]

- Danilewicz, D. Management Challenges in the Hotel Industry in the Face of Social and Technological Changes. In Wyzwania Społeczne i Technologiczne a Nowe Trendy w Zarządzaniu Współczesnymi Organizacjami; Urbaniak, M., Tomaszewski, A., Eds.; SGH: Warszawa, Poland, 2020; ISBN 978-83-8030-374-4. [Google Scholar]

- Tourism in 2020. Statistics Poland (SP). Tables in XLSX Format in ZIP File. Available online: https://stat.gov.pl/en/topics/culture-tourism-sport/tourism/tourism-in-2020,1,18.html (accessed on 21 June 2021).

- Walas, B. Badania Opinii Pracodawców Podsektora Hotelarstwa w Czasie Pandemii COVID-19; Instytut Turystyki: Kraków, Poland, 2021. [Google Scholar]

- Enz, C.A.; Canina, L.; Walsh, K. Hotel-industry averages: An inaccurate tool for measuring performance. Cornell Hotel Rest. A 2001, 42, 22–32. [Google Scholar] [CrossRef]

- Lieberman, W.H. Getting the most from revenue management. J. Revenue Pricing Manag. 2003, 2, 103–115. [Google Scholar] [CrossRef]

- Hayes, D.K.; Miller, A.A. Revenue Management for the Hospitality Industry; John Wiley & Sons: Hoboken, NJ, USA, 2011; ISBN 978-0-470-39308-6. [Google Scholar]

- Smart, K.; Ma, E.; Qu, H.; Ding, L. 2021. COVID-19 impacts, coping strategies, and management reflection: A lodging industry case. Int. J. Hosp. Manag. 2021, 94, 102859. [Google Scholar] [CrossRef]

- Landman, P. Occupancy Rate, Xotels. Available online: https://www.xotels.com/en/glossary/occupancy-rate (accessed on 12 September 2022).

- Hotel KPI’s Explained: ADR, REVPAR and GOPPAR, Revfine.com. Available online: https://www.revfine.com/what-is-adr-revpar-goppar/ (accessed on 12 September 2022).

- Key Performance Indicators, Fáilte Ireland, Business Tools. Available online: https://www.failteireland.ie/FailteIreland/media/WebsiteStructure/Documents/2_Develop_Your_Business/1_StartGrow_Your_Business/Key-Performance-Indicators.pdf (accessed on 12 September 2022).

- Tourism in 2019. Statistics Poland (SP). Tables in XLSX Format in ZIP File. Available online: https://stat.gov.pl/en/topics/culture-tourism-sport/tourism/tourism-in-2019,1,17.html (accessed on 21 June 2021).

- Wójcicki, T. Application of the CAWI method for the holistic support of innovation transfer to business practice. Maint. Probl. 2012, 4, 175–186. [Google Scholar]

- Barbu, A.; Isaic-Maniu, A. Data collection in Romanian market research: A comparison between prices of PAPI, CATI and CAWI. Manag. Mark. 2021, 6, 349–364. Available online: file:///C:/Users/User/Downloads/DATA_COLLECTION_IN_ROMANIAN_MARKET_RESEARCH_A_COMP-2.pdf (accessed on 20 September 2022).

- Wykorzystanie Technologii Informacyjno-Komunikacyjnych w Jednostkach Administracji Publicznej, Przedsiębiorstwach i Gospodarstwach Domowych w 2019 Roku, Statistics Poland. 2020. Available online: https://stat.gov.pl/obszary-tematyczne/nauka-i-technika-spoleczenstwo-informacyjne/spoleczenstwo-informacyjne/wykorzystanie-technologii-informacyjno-komunikacyjnych-w-jednostkach-administracji-publicznej-przedsiebiorstwach-i-gospodarstwach-domowych-w-2019-roku,3,18.html (accessed on 20 September 2022).

- Market Report. Poland Market Update. Horwath HTL (August 2020). Available online: https://www.hospitalitynet.org/file/152008876.pdf (accessed on 14 September 2021).

- STR SHARE Center. Available online: https://str.com/training/academic-resources/share-center (accessed on 4 June 2022).

- Kwiecień w Hotelach: RevPAR w Krakowie—3,9 zł, Obłożenie w Trójmieście—3,5 Proc., Hotelarz (20 May 2020). Available online: https://www.e-hotelarz.pl/artykul/67719/kwiecien-w-hotelach-revpar-w-krakowie-39-zl-oblozenie-w-trojmiescie-35-proc-2/ (accessed on 14 September 2021).

- Działania Hoteli w Związku z Pandemią Koronawirusa—Wyniki Ankiety IGHP. Izba Gospodarcza Hotelarstwa Polskiego (23 April 2020). Available online: https://www.ighp.pl/aktualnosci/szczegoly-aktualnosci?NewsID=46938 (accessed on 14 September 2021).

- Turystyka Letnia w Czasach Pandemii. Komunikat z Badań (125/2020). Available online: https://www.cbos.pl/SPISKOM.POL/2020/K_125_20.PDF (accessed on 14 September 2021).

- Panayotis, V. Assessment of the Hotel Industry in 2021: The French Hotel Industry Still Marked by the Crisis in 2021, Positive Signals Can Be Seen at the End of the Year. Hospitality ON Magazine, 17 January 2022, Updated on 17 March 2022. Available online: https://hospitality-on.com/en/hotel-trends/assessment-hotel-industry-2021-french-hotel-industry-still-marked-crisis-2021-positive (accessed on 20 September 2022).

- Wykorzystanie Turystycznej Bazy Noclegowej w Polsce w Październiku i Listopadzie 2020 r. Statistics Poland (SP). Available online: https://stat.gov.pl/obszary-tematyczne/kultura-turystyka-sport/turystyka/wykorzystanie-turystycznej-bazy-noclegowej-w-polsce-w-pazdzierniku-i-listopadzie-2020-r-,6,23.html (accessed on 14 September 2021).

- Fatalny Październik w Hotelach—Ceny Wciąż Spadają, Gości Brak. Izba Gospodarcza Hotelarstwa Polskiego (9 November 2020). Available online: https://www.ighp.pl/aktualnosci/szczegoly-aktualnosci?NewsID=51764 (accessed on 14 September 2021).

- Hotelarstwie w Dobie COVID-19 Podczas V Forum Hotelarzy IGHP. Izba Gospodarcza Hotelarstwa Polskiego (9 October 2020). Available online: https://www.ighp.pl/aktualnosci/szczegoly-aktualnosci?NewsID=50786 (accessed on 14 September 2021).

- Magnini, V.; Crotts, C.J.; Calvert, E. The increased importance of competitor benchmarking as a strategic management tool during COVID-19 recovery. Int. Hosp. Rev. 2021, 35, 280–292. [Google Scholar] [CrossRef]

- Fatima, T.; Elbanna, S. Balanced scorecard in the hospitality and tourism industry: Past, present and future. Int. J. Hosp. Manag. 2020, 91, 102656. [Google Scholar] [CrossRef] [PubMed]

- Zaki, K. Implementing dynamic revenue management in hotels during COVID-19: Value stream and wavelet coherence perspectives. Int. J. Contemp. Hosp. Manag. 2022, 34, 1768–1795. [Google Scholar] [CrossRef]

- Wadongo, B.; Odhuno, E.; Kambona, O.; Othuon, L. Key performance indicators in the Kenyan hospitality industry: A managerial perspective. Benchmarking Int. J. 2010, 17, 858–875. [Google Scholar] [CrossRef]

- Mohamadkhani, K.; Lalardi, M.N. Emotional intelligence and organizational commitment between the hotel staff in Tehran, Iran. Am. J. Bus. Manag. 2012, 1, 54–59. [Google Scholar] [CrossRef] [Green Version]

Figure 1.

Timeline of the COVID-19 hotel restrictions in Poland.

Figure 2.

Flow chart of research process.

Figure 3.

Number of hotels, bed places, and tourists accommodated in the selected Polish cities in 2019 (source: based on “Tourism in 2019” [60]).

Figure 3.

Number of hotels, bed places, and tourists accommodated in the selected Polish cities in 2019 (source: based on “Tourism in 2019” [60]).

Figure 4.

Occupancy rate in 3- and 4-star hotels in selected Polish cities in 2019–2022.

Figure 5.

ADR values for 3- and 4-star hotels in selected Polish cities in 2019–2022.

Figure 6.

RevPAR values for 3- and 4-star hotels in selected Polish cities in 2019–2022.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table 1.

Number of hotels, bed places, and tourists accommodated in analyzed Polish cities in 2019.

| City | Total Number | Category | During Categorisation | ||||

|---|---|---|---|---|---|---|---|

| 5-Star | 4-Star | 3-Star | 2-Star | 1-Star | |||

| Hotels | |||||||

| Poland | 2635 | 76 | 418 | 1318 | 559 | 136 | 128 |

| Kraków | 167 | 13 | 49 | 81 | 17 | 5 | 2 |

| Poznań | 59 | 3 | 15 | 32 | 8 | 1 | – |

| Tri-City a | 87 | 11 | 15 | 45 | 14 | – | 2 |

| Warsaw | 98 | 14 | 19 | 37 | 19 | 6 | 3 |

| Wrocław | 58 | 7 | 13 | 27 | 4 | 4 | 3 |

| Bed places in hotels | |||||||

| Poland | 286,231 | 19,191 | 82,023 | 122,433 | 41,546 | 11,087 | 9951 |

| Kraków | 24,618 | 2548 | 8638 | 8842 | 3582 | 869 | 139 |

| Poznań | 7424 | 480 | 2725 | 3281 | 902 | 36 | – |

| Tri-City a | 13,202 | 2141 | 3436 | 6030 | 1501 | – | 94 |

| Warsaw | 27,868 | 5710 | 9020 | 8060 | 2726 | 1837 | 515 |

| Wrocław | 10,047 | 1546 | 2710 | 3907 | 788 | 773 | 323 |

| Tourists accomodated in hotels | |||||||

| Poland | 23,511,588 | 1,851,601 | 7,230,202 | 9,783,583 | 2,993,850 | 974,781 | 677,571 |

| Kraków | 2,194,340 | 200,270 | 854,872 | 856,761 | 180,155 | 102,282 | |

| Poznań | 719,508 | 51,756 | 248,879 | 314,531 | 104,342 | – | |

| Tri-City a | 1,188,367 | 182,036 | 358,397 | 509,478 | 131,404 | – | 7052 |

| Warsaw | 3,345,722 | 665,510 | 1,039,913 | 1,038,881 | 312,792 | 288,626 | |

| Wrocław | 1,203,967 | 183,961 | 340,291 | 435,518 | 81,602 | 131,328 | 31,267 |

a metropolitan area of three cities: Gdańsk, Gdynia, and Sopot; source: based on “Tourism in 2019” [60].

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Widz, M.; Krukowska, R.; Walas, B.; Kruczek, Z. Course of Values of Key Performance Indicators in City Hotels during the COVID-19 Pandemic: Poland Case Study. Sustainability 2022, 14, 12454. https://doi.org/10.3390/su141912454

AMA Style

Widz M, Krukowska R, Walas B, Kruczek Z. Course of Values of Key Performance Indicators in City Hotels during the COVID-19 Pandemic: Poland Case Study. Sustainability. 2022; 14(19):12454. https://doi.org/10.3390/su141912454

Chicago/Turabian StyleWidz, Monika, Renata Krukowska, Bartłomiej Walas, and Zygmunt Kruczek. 2022. "Course of Values of Key Performance Indicators in City Hotels during the COVID-19 Pandemic: Poland Case Study" Sustainability 14, no. 19: 12454. https://doi.org/10.3390/su141912454

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.