How Has the COVID-19 Pandemic Affected the Different Branches of the Agri-Food Industry in Extremadura (Spain)?

Department of Economics, Faculty of Economics and Business Sciences, University of Extremadura, Avd. Elvas, s/n, 06006 Badajoz, Spain

*

Author to whom correspondence should be addressed.

Land 2022, 11(6), 938; https://doi.org/10.3390/land11060938

Submission received: 11 May 2022

/

Revised: 14 June 2022

/

Accepted: 16 June 2022

/

Published: 18 June 2022

(This article belongs to the Special Issue Economic, Social and Demographic Challenges of Rural Areas: Contributions From the Analysis of the Economic Activity Location and the Study of Depopulation)

Abstract

:The COVID-19 pandemic has had a significant impact on the world economy since 2020. This study analyzed the impact of the pandemic on innovative agri-food companies from different branches of agro-industrial activity located in Extremadura (Spain). The main aim of this study was to determine which activities have been most affected. Differences between actions and changes made depending on the nature of the product, process, or services were also evaluated. The information was obtained from an online questionnaire in which the research questions were posed (what consequences, actions, or changes has the pandemic had on the development of firms’ activities?). Data were analyzed descriptively, and a statistical study was conducted on the existence or absence of independence between effects and actions based on the branches of activity of agri-food industries. The main results showed that companies’ financial (decrease in turnover and reduction/displacement of product demand) and operational functioning (difficulty in marketing activities and standstill/decline in the fiscal year) has mainly been affected. In response, innovative agro-industries have acted regarding their processes (increased ICT use and new marketing strategies) and procedures (implementation of stricter hygienic-sanitary protocols and reorganization of activities and personnel) to deal with the negative effects on their activities. In general, all agro-industrial branches have incorporated changes in their products and services, mainly by providing new and better customer benefits, and improving product formats and forms of payment to suppliers. These findings provide information for the regional public administration in the development of initiatives that mitigate the negative effects of the pandemic and favor the implementation of actions that help the adaptation of agro-industrial activities. Agricultural policies should incorporate specialized measures to ensure the global sustainability of the food and agriculture system and the supply and production.

1. Introduction

In early 2020, the world turned its attention to China, where the COVID-19 pandemic was spreading throughout the country. Two months later, in Europe, the SARS-CoV-2 infection became the focus of the pandemic, spreading rapidly [1,2]. Globally, the pandemic situation has become a health threat and is having an unprecedented economic impact on the global economy [3,4]. This situation is challenging the management and financial capabilities of governments and medical systems, and the ability of many organizations to respond to pandemic-induced changes [5,6]. Overall, the pandemic has affected all areas, regions, and sectors of activity. In the case of the food and beverage manufacturing sector, the sector that is the focus of this study, food production and consumption patterns have been disrupted [7,8,9,10]. The challenges facing this sector involve operations, security, the supply chain, training, emergency response, awareness, incident management, recreation of business models, digitization, and other impacts that have not previously been considered [11].

In this context, the effects produced by the pandemic have also affected the Spanish economy with different intensities according to the regions and sectors of activity. This study focused on an analysis of the pandemic’s impact and its consequences on the agri-food industry in a specific Spanish region: Extremadura. Extremadura is a Spanish region that is composed of two provinces (Cáceres and Badajoz) and borders Portugal on its western side. Its territory is large in terms of surface area (8.22% of the country), although it is sparsely populated (it represents 2.2% of the total Spanish population). The region has 1,059,310 inhabitants (July 2020 data), with an average density of 25.7 inhabitants per km2 compared to 92.3 in the rest of the country [12].

As in other regions of the world, Extremadura has been affected by the COVID-19 pandemic. The negative effects have hit the Spanish regions with different intensities, with those that are the most dependent on tourism being the most affected and, on the other hand, those with a relative specialization in the primary sector being the least affected [13]. It is precisely this context that surrounds the economy of Extremadura. In fact, the two least-affected provinces of the national territory were Cáceres and Badajoz, which are characterized by lower exposure to tourism and a greater weight of the sectors that have been less affected by COVID-19, such as agriculture and the public sector [14].

According to a recent report by the University of Extremadura [15], the direct impact of the crisis in the region is estimated at 1066 M€, causing a 9.3% drop in gross domestic product (GDP) and an 11% drop in employment by 2020. The pandemic has had an economic impact on companies, affecting the variability of sales, which fell by 12.69%, especially in micro-companies (−15.1%) and, by sector, in industry (−15.8%) and services (−13.1%).

In Extremadura, the agri-food sector is strategic in terms of promoting the economic and territorial development of the region. As a whole, the agri-food sector represents 3.4% of the gross value added (GVA) and 4% of employment. The significance of the agri-food industry represents more than 35% of the industry and 3.96% of employment. Therefore, the weight of the agricultural sector and its associated industries is notably higher than the national average. According to data from the Spanish National Institute of Statistics (NIS) [16], in 2020, there were 1382 companies associated with the food, beverage, and tobacco industries, which represents 2.07% of the total in the Extremadura region. Agri-food organizations make up 0.89% of the total number of industries in the country, with agri-food organizations in Extremadura totaling more than twice that the national level.

The Extremaduran agri-food industry is characterized by medium-sized industries (mainly meat industries, vegetable and fruit canning industries, vegetable oils and fats, and animal feed producers), which coexist with a large number of small-sized bakery and confectionery companies [17]. The most outstanding subsector is the meat industry, which accounted for 26.21% (617,292,000 €) of the total business value of the agro-industrial subsectors of Extremadura in 2014. This is followed by the canning, fruit, and vegetable industry, with 21.11% (497,255,000 €), and the animal feed industry, with 16.31% (384,283,000 €) [18].

However, despite its relevance in regional economic development, Extremadura’s agribusiness suffers from chronic problems derived from a lack of business clusters, its small size and local nature, and marginal innovation activities [17]. Thus, the agri-food industry is undergoing substantial changes as it recognizes the need to include innovation in its strategies and to change its products. On the one hand, it must adapt its products to the new food demands of consumers and markets in order to be more competitive and “differentiate” itself from other producers. On the other hand, it must adapt its organizational structure, and especially its marketing strategies, in order to increase its competitiveness and adapt to the international market, all of which implies non-technological innovation changes. Innovation (technological and non-technological) provides agri-food companies with the opportunity to generate higher incomes and increase their productivity and competitiveness, which is especially relevant in crisis situations [19].

The present study was developed within the framework of wider research focusing on an analysis of innovation in the agri-food industry in Extremadura (Spain). At the beginning of the research, the pandemic and confinement occurred, which led to the focus of the study on an analysis of the aspects related to the impact that the pandemic had had on companies. An initial preliminary qualitative study developed by Corchuelo et al. [20] was performed in which the effects and actions carried out by the companies were detected. The findings of this study served as the basis for raising the questions analyzed in the present research and quantified the effects of the pandemic by differentiating among the various agri-food activity branches, which is the principal novelty of the present study.

There are few studies that have analyzed the impacts, implications, or consequences of the pandemic crisis and the actions implemented by innovative agricultural organizations and even fewer studies have focused on industries located in Extremadura. Specifically, in the study conducted by Corchuelo et al. [20], the impact of the pandemic on the Extremadura agri-food industry was analyzed in general terms. However, this industry encompasses a very heterogeneous set of activities ranging from the production of raw materials to the elaboration of more sophisticated foods, so it is of great interest to segregate the results based on the different branches of activity. The different branches of economic activities were defined according to the firms’ main activities using the Spanish National Classification of Economic Activities (NCEA-2009), which considers the subsectors 10 (food industry), 11 (beverages), and 12 (tobacco).

Given this framework, the main objective of this study was to analyze the impact, consequences, and implications of the pandemic on innovative agro-industries in the different branches of activity. We examined which activities have been most affected. Differences between actions and changes made depending on the nature of the product, process, or service were also evaluated. The following research questions were posed:

- o

- What consequences has the pandemic had on the development of the activities of agri-food companies in Extremadura, Spain?

- o

- What actions have Extremaduran agri-food companies taken to deal with its consequences?

- o

- What changes have Extremaduran agri-food companies been forced to make?

- o

- Are there any differences in terms of the effects/actions/changes according to the branches of activity of the industry?

This research fills this gap by providing an overview of the consequences, implications, and actions taken by innovative agri-food industries in Extremadura according to the branch of activity. There are still few studies on the impact of COVID-19 in the Extremadura region and, more specifically, in the agro-industry sector, which, in turn, implies novelty. In this sense, the results of the present research make a useful contribution to the existing literature on the impact of the pandemic on the agricultural sector, especially in the Extremadura region.

This paper is organized as follows: Section 2 provides a background review of the research. Section 3 presents the research design, the collection of data, and the data analysis. The findings are shown in Section 4. Finally, in Section 5 and Section 6, the discussion and conclusions of the study are presented.

2. Literature Review: Impact of COVID-19 on the Economy

2.1. Worldwide State of the Pandemic Situation in Economic Sectors

Globally, the uncertainty generated by the pandemic has rendered business planning and problem-solving approaches incapable of managing the variability and evolution of the pandemic [5]. According to a study of the Argentine economy, this crisis, unlike previous ones, is a hybrid that affects economic and health aspects, challenging not only the fragility and inadequacies of health infrastructure but also mutations of the virus with different degrees of virulence. The profound economic, political, health, and technological impact of the pandemic has triggered the biggest global crisis since the post-war period. In response, governments have developed different measures aimed at minimizing economic, health, and social damage [21].

From a macroeconomic perspective, some business experts have drawn up a list of changes brought about by the COVID-19 pandemic that will have long-term implications [22]. The first is the acceleration towards a digital economy: Governments have adopted measures to restrict physical interpersonal contact, forcing people to interact and work remotely [23,24,25,26,27]. Second, a slowdown in border activity has occurred: the pandemic has disrupted trade, travel, and other border activities. This has particularly affected airlines and tourism [28,29]. A third change that has occurred is the greater protagonism of governments and the pressure placed on them to carry out reforms: the economic consequences of the crisis imply a greater demand for financial support for employees and companies from governments. On the other hand, the debate on the differences between the public and private health systems has also increased [30,31,32]. The fourth change relates to a greater focus on crisis management and recovery; the situations that society has had to face have raised an awareness of the importance of having a government capable of leading the re-establishment [33]. Last, there is the question of economic pressure. The sizes of the aid packages announced by governments are greater than the stimulus invested in the global financial crisis of 2008. In fact, in OECD (Organisation for Economic Co-operation and Development) countries, governments have pledged 3.5% of their global GDP to new programs aimed at reviving their economies, up from 2.1% in 2009 at the height of the global financial crisis. The International Monetary Fund (IMF) estimated that, globally, the average fiscal deficit in 2020 would be 10% of the GDP (compared to 3% per year, on average, since the global financial crisis) and that gross national debt would rise to 96% of the global GDP, up from 83% in 2019 [34].

Moreover, the impact of the crisis has unequally affected the sectors of economic activity globally. Chief financial officers (CFOs) in particular sectors such as semiconductors, retail, and software are generally hopeful about the impact of the pandemic on incomes and earnings compared to April 2020 while CFOs in other industrial goods industries (e.g., the automotive industry) are more reserved and pessimistic. Overall, more than half of the respondents to the Boston Consulting Group survey [35] indicated that the economic impact of the crisis continues to be severe. However, when it comes to recovery, they envisage different scenarios and focus on taking decisive action to support their businesses in the face of the crisis, putting costs, cash, and performance at the top of their agenda [35].

A study by Carlsson-Szlezak et al. [36] argues that the sectors least affected by the advance and speed of the spread of the pandemic globally have been the real estate, consumer goods, financial services, and grocery sectors. In the case of the automotive and other durable goods sector, it was affected at the onset of the pandemic and in particular by the physical shutdown measures, which, in turn, led to a lack of supplies and disruption of its own supply model. The results show that immunization could contribute to the recovery of the most-affected sectors. In addition, the relaxation of virus containment measures worldwide, together with the resilient capacity of these sectors, has led to their activities being reactivated with renewed strength, in some cases even exceeding pre-crisis levels [37,38].

The study by Bharadwaj et al. [39] states that the unequal impact of the pandemic across sectors of activity is determined by consumer behavior. According to Bona et al. [40], the crisis was triggered when massive changes were already taking place in the way people interact with the media (media consumption). However, health and wellbeing have become priorities for many consumers. For example, the lockdown led to the growth of certain product categories related to healthy habits, such as increased consumption of fresh food.

The global response to the pandemic has been the incorporation of creative and innovative trends across sectors that enable adaptation to changing markets [41]. The pandemic has accelerated the digital ecosystem [42,43,44,45]. An example of this is the way in which companies, their employees, customers, and suppliers relate to each other. Ninety percent of companies have changed their use of channels in their relationship with their customers during the pandemic, with the web and its apps being preferred by the customer when contracting new products [46,47]. Similarly, some organizations have been forced to implement teleworking to ensure business continuity [48].

The agri-food sector has also been affected by the pandemic, although it has not stopped its activities and has guaranteed the supply of food to society [20]. The prospective study by Barcaccia et al. [49] provides insight into the impact of the pandemic on the Italian agri-food sector during the national shutdown and analyzes this unexampled economic crisis as a turning point for addressing the overall sustainability of food systems and agriculture in the framework of the forthcoming European Green Pact. The study by Escobar et al. [50] establishes that the most damaged link in the agri-food industry is wholesale trade, with impacts derived from the state of alarm itself (with the closure of the HORECA channel), which generated a decrease in demand, amongst others, and an increase in surpluses.

Overall, food delivery and distribution in almost all countries has been interrupted, with several negative effects. The study by Mukhamedjanova [51] explains that the supply chain was severely affected during the pandemic. In addition, another emerging problem concerns the availability of labor in the agri-food sector, where substantial labor constraints have been experienced [52,53]. In general, the pandemic has also brought about a change in food consumption patterns in households; numerous studies have highlighted the change in food consumption patterns during confinement in different regions of the world [54,55,56,57].

The report by Hossain [58] summarizes the potential risks, responses, and policy actions that the Asian Productivity Organisation (APO) member countries have taken in the agri-food sector to prevent food security threats and to ensure business continuity. The United Nations (UN) report [59] analyzed the impact of the COVID-19 pandemic on the Egyptian food system through a qualitative evaluation using semi-structured interviews with key national stakeholders. The results of the report include recommendations to promote the adjustment, recuperation, and transformation of the agri-food sector in Egypt. Thus, the main recommendations provided in this study are: information and advice (e.g., on market opportunities, contingency measures, safety, and quality); financial support measures to support liquidness and ease the financial burden on enterprises; and proposed adjustments in food safety and import/export legislation.

The Food and Agriculture Organisation (FAO) of the United Nations has ighlighted the role of agribusiness in sustaining and operating food systems during the pandemic crisis [52]. This report also contains recommendations aimed primarily at ministries, public institutions, food industry associations, local business service providers, and chambers of commerce, including businesses oriented toward sustaining the agri-food industry from a strategic management point of view, such as business scenario planning, alternative input supply channels, phased investment plans for innovation, staff health and safety practices, and human resource planning in the face of increased demand [52].

In general, as in other sectors of activity, the speed and characteristics of the spread of the pandemic, together with the appearance of new variants of the virus, has meant that there is great uncertainty about the future effects and problems that the pandemic may cause in a sector such as the agri-food industry [60]. The study by Stephens et al. [61] tracked the unexpected risks, weaknesses, and systemic changes that agricultural systems have experienced as a result of the pandemic in order to understand the short-, medium-, and long-term effects. According to Aldaco et al. [62], the COVID-19 pandemic will have impacts on agriculture and food security, resulting in a food crisis, although this is still too early to say since the pandemic has not yet ended.

2.2. State of the Pandemic Situation for the Agri-Food Sector in Spain and Extremadura

In Spain, the principal effect of the pandemic situation on the economy was the historic fall of 17.8% quarter-on-quarter (21.5% year-on-year) in its GDP in the second quarter of 2020, the largest decline observed since 1995 [63]. The sectors of economic activity most affected by the health crisis were declared to have been the hotel and catering industry, commerce, and tourism. The Spanish hotel and catering industry accounts for 6.2% of the country’s GDP, which is higher than in other countries. Moreover, it is a critical axis of support for tourism, another engine of national wealth. However, despite its weight in the Spanish economy, it is a particularly fragile industry and is vulnerable to economic cycles and shocks, such as the current crisis caused by the COVID-19 pandemic [64,65]. The aggregate effects of the pandemic on the Spanish tourism sector have been even worse than in the rest of the world. During 2020, the number of foreign travelers fell by 77%, bringing the Spanish tourism sector to 1969 levels [66]. In addition, the Spanish tourism sector experienced a fall in GDP of around 69% in 2020 [67].

In the case of Extremadura, the report by Hernández-Mogollón et al. [15] analyzed the impact of the health crisis on small- and medium-sized business enterprises (SMEs) in Extremadura from an economic, employment, and organizational point of view. This study was based on a questionnaire sent to Extremaduran companies with 6 to 249 workers. The main results showed a similar decrease in sales in Spain (12.76%) as in Extremadura (12.69%). However, most of the companies indicated that they expected stability or growth in sales in 2021. The economic-financial impact had a greater negative impact on micro-enterprises while investments, debt level, and liquidity affected medium-sized companies more negatively.

However, the effect of the COVID-19 pandemic has emphasized the relevance of the agri-food sector as a vital part of the Spanish economy, a sector that has not stopped its activity and has guaranteed food supplies since the state of alarm was declared (14 March 2020) and during the subsequent containment measures imposed by the government [20]. The pandemic has tested the resilience and capacity of the food chain to adapt to a sudden increase in demand since, in recent history, this sector had never been subjected to such a level of stress. Retrospectively, it is fair to highlight the excellent response of the entire sector to overcome this challenge and to guarantee the food supply for the entire population. In fact, the weight of the primary sector in the total economy has increased and the agri-food industry underwent a much smoother decline than the manufacturing industry in the second quarter of 2020 [63,68].

In this sense, numerous economic reports have uncovered that the Spanish agri-food sector is one of the sectors that was least impacted by the pandemic. According to the CaixaBanck Research report [63], the gross value added (GVA) of the primary sector expanded by 3.6% quarter-on-quarter (6.3% year-on-year) in the second quarter of 2020, with a significant increase in the consumption of staple goods and in the importance of the weight of the primary sector in the total economy, providing 3.8% of the GDP, 1.1% more than in 2019. However, as previously stated, other sectors in Spain, such as tourism, which has a direct influence on the activities of other productive occupations of the Spanish economy, have been severely affected, and this, in turn, has damaged the agri-food sector [69]. A study carried out by the Bank of Spain [70] established that the agri-food industry (food, beverages, and tobacco) acts as a supplier of tourism activities, and the results of an analysis of input-output tables showed that for every euro of turnover in accommodation and catering services, 30 cents is produced by the agri-food sector. Therefore, the decline in tourism is transmitted to the food chain to suppliers of food to restaurants, products that tend to be consumed less frequently at home and that cannot easily find an alternative market [71]. This has also meant that the agri-food industries that have suffered the most are those that target their products to the HORECA channel (hotel, restaurant, and café). Specifically, in June 2020, the hotel and catering sector recorded a 17.4% drop in the number of social security affiliates, with a loss of more than 300,000 employees. This represents a decrease of 1.5 million registered employees in the hotel and catering sector, compared to almost 1.8 million in the same period of the previous year [71].

The report of the Spanish Federation of Food and Drink Industries (FIAB) [68], also highlights the importance of the agri-food industry in generating employment in Spain. During the months of February to May 2020, the agri-food sector was one of the few sectors that recorded less job destruction, had fewer workers affected by ERTE (temporary employment regulation files), and experienced an increase in the average affiliation, general regime (a rise of 5.9% compared to a drop of 4.1% in the national average), and self-employed (increase of 0.3% compared to a decrease of 1.1% in the national average).

Regarding foreign trade activities, although there has been a general decrease in exports in other economic sectors, in the agri-food, fisheries, and forestry sector, exports increased and reached 40,997 million euros in the period from April to December 2020, compared to 39,905 million in the same period of 2019 (an increase of 2.7%). The food groups that registered an increase in export rates were fruit and nuts, followed by meat, vegetables and legumes, beverages, and oils and fats, with these groups having the same order of relevance for the same period of 2019 [72].

As with the rest of the world, Spain has experienced changes in food habit trends. During March–May 2020, the consumption of Mediterranean and nutritionally rich foods increased. The study by Pérez-Rodrigo et al. [73] shows that the main changes in consumption trends during the first confinement in Spain (mid-March to mid-May 2020) were the purchase of healthier foods, less spending on foods of low nutritional interest, and increased cooking at home. Regarding the type of food and its consumption, in accordance with the report published by the Ministry of Agriculture, Fisheries, and Food (MAPA) on 15 May 2020, in relation to data from the consumption panel relating to the purchase volume of Spanish households during the month of March, an increased presence of meat, vegetables, legumes, rice, and dairy products was observed in shopping baskets, and a greater demand for fish products [74]. This trend is maintained in a subsequent report of the Ministry of Agriculture, Fisheries and Food [75], published on 19 May 2020, referring to household consumption between 4 May and 10 May [74,75].

Similarly, other reports and studies have also revealed that during the lockdown, there was a 50% increase in spending in supermarkets and large food outlets. There was also a 60% increase in the use of online commerce for food purchases, thus avoiding movement, travel, and contact among people. In addition, spending on restaurants was reduced by 90% [63,76].

The report by Caldart et al. [71] collected the opinions of executives from 185 Spanish companies related to the food and beverage sector; it analyzed the progress of invoicing, foreign sales, occupation, and inversions of the companies and provided a final reflection on the future of the food sector. The conclusions revealed that the turnover that has suffered most since the state of emergency in Spain is the hotel and catering industry. In the case of exports, 45% of companies with international sales reported significant drops in exports and approximately 23% reported increases. Finally, the report also analyzed the changes and impact of the COVID-19 pandemic on investment decisions, with the main conclusion being an increase in investments and advances in the field of digital transformation, with investments in product innovation in second place, and, lastly, investments in capital goods and people training.

The report by the FIAB [68] established measures to enhance the competitivity of the agri-food sector after analyzing the impact of COVID-19 on this sector. The figures show that the food and beverage industry has established itself in Spain as a stable, competitive, and wealth-generating sector despite the consequences of the COVID-19 pandemic. The responsibility and efforts of companies and workers have ensured that the performance of this industry in 2019–2020 maintained positive progress in areas such as employment and exports, thus contributing to a solid image of the sector within and beyond Spanish borders despite the pandemic crisis [68].

In the case of the Extremaduran agri-food sector, there are no studies that have analyzed the impact caused by the COVID-19 pandemic, which is an essential sector for the economic and territorial development of the region. The study by Corchuelo et al. [20] addressed this issue by means of a qualitative analysis through a multiple-case study. The results showed that innovative agri-food industries in Extremadura have been affected by negative impacts, which is detrimental to the operational and financial performance of the companies. In response, industries have incorporated changes in their processes and procedures to adapt their activities. However, no previous studies have analyzed the effect of the pandemic on the different branches of the agri-food sector in Extremadura. The main novelty of this study lies in its analysis of the responses provided by the main managers of agri-food companies in Extremadura, and the impacts and actions developed in the various branches of activity.

3. Materials and Methods

3.1. Research Design and Data Collection

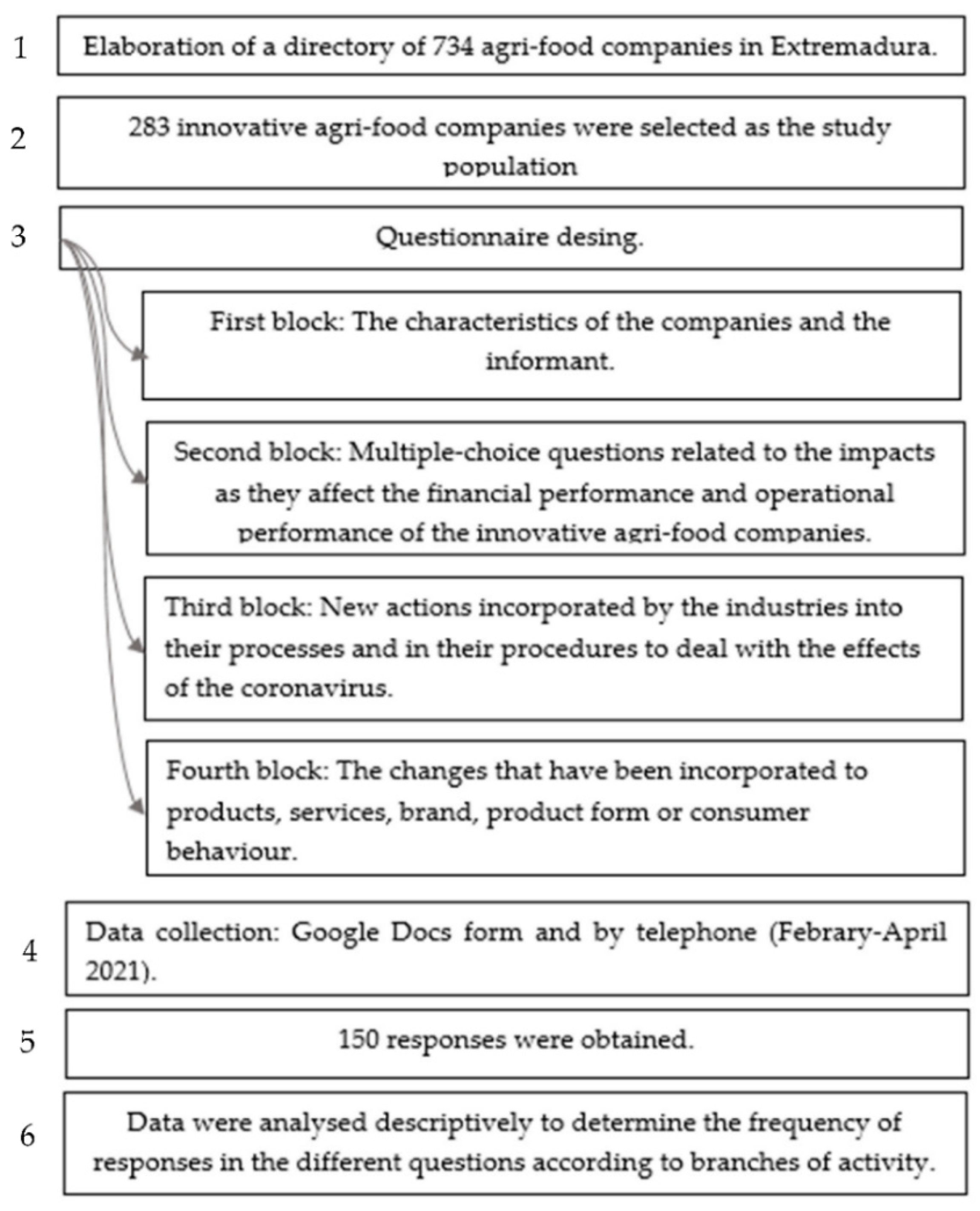

The information that can be obtained on the innovative activities of companies in Spain (mainly, Statistics on R&D Activities [77] and the Business Innovation Survey of the Spanish National Statistics Institute, NIS [78]) is at the national level. Data corresponding to Extremaduran companies is scarce, especially data referring to a specific sector of activity. In addition, information is offered for companies with more than 10 workers, with micro-companies (companies with less than 10 workers) being the main size of the business fabric in the region. The scarcity of information on agribusiness in Extremadura led to the creation of a bespoke database that constituted the starting population. Figure 1 shows the stages of the research design.

The population on which this study is based was obtained from a previously prepared report/directory based on the crossing and analysis of various databases [79,80,81]. Agri-food companies belong to the sector codes 10 (agri-food industry), 11 (beverages), and 12 (tobacco) of the Spanish National Classification of Economic Activities (NCEA). The report/directory contained information on 734 companies, of which innovative agri-food companies (283 companies) were selected as the study population. In contrast to the official data from the Spanish NIS, which offers data on the innovative activity of companies with more than 10 employees, the database used contains information on companies with less than 10 employees.

Secondly, a questionnaire was designed based on the results of previous research [20]. In this previous study, a qualitative methodology (multiple case study) was used. Based on this methodology, 15 in-depth semi-structured interviews with managers of innovative companies in the Extremaduran agricultural sector were conducted, providing a previous diagnosis of the effects of the pandemic situation in the sector. This study evidenced the different impacts of the pandemic on the Extremadura agri-food industries, which the interviewees classified as “impacts or negative consequences” and “actions” taken to mitigate the effects of the pandemic [20].

The questionnaire was structured in four blocks of questions (Appendix A). The first block included questions on the characteristics of the companies and the informant. In this first block of questions, the companies were asked about the type of innovation developed, which was classified into technological innovation (product or process) and non-technological innovation (organizational or marketing) according to the definition of the Oslo Manual [82]. The second block included multiple-choice questions related to the impacts as they affected the financial performance (decrease in turnover, reduction/displacement of demand, slowdown in the development of R&D projects, and decrease in the investment budget) and operational performance (difficulty in carrying out marketing activities, lack of personnel due to quarantines, stoppage/decline of activity, and problems in receiving supplies from their suppliers) of the innovative agri-food companies. The third block analyzed the new actions incorporated by the industries into their processes (increased production, search and diversification of suppliers and customers in other markets, increased use of communication technologies, and new marketing strategies) and procedures (reorganization of activities and personnel and implementation of stricter hygienic-sanitary protocols) to deal with the effects of the COVID-19 pandemic. A fourth block of questions was included to expand the information and obtain a more detailed view of the changes that were incorporated into the products, services, brand, product form, or consumer behavior; this fourth section provided a more detailed vision of the changes that were incorporated specifically in products, services, branding, product format, or consumer behavior in the sub-sectors of the agri-food sector.

Data collection was carried out by means of a Google Docs form and by telephone, with the field study being conducted during the months of February to April 2021. The questionnaire was sent to managers of agri-food companies. The characteristics of the companies and informants are presented in the Section 4.

The participation of the companies was voluntary. Of the 283 innovative agribusinesses in Extremadura that were contacted, 150 responses were obtained (53% of all innovative agribusinesses). It is assumed that the sample is adequate (confidence level 95% and margin of error 5.5%, according to Equation (1) formulated in the work of [83]) for the objectives of this study:

where:

- s = required sample size.

- N = the population size.

- = the table value of chi-square for 1 degree of freedom at the desired confidence level (3.8416).

- P = the population proportion (assumed to be 0.50 since this would provide the maximum sample size).

- d = degree of accuracy expressed as proportion (0.05).

3.2. Data Analysis

Data were analyzed descriptively to determine the frequency of responses in the different questions according to the branches of activity. From a statistical point of view and considering the frequencies observed for each question, the Pearson chi-square test applied to the study of two variables (contingency tables) was used [84,85,86]. This contrast is based on the comparison of the observed frequencies (empirical frequencies) in the sample with those expected (theoretical or expected frequencies) if the null hypothesis (indicating that both variables are independent) was true. In this way, the existence of an association (or dependence) in each of the aspects analyzed (consequences, actions, and changes) and the branches of activity of the agri-food industry was analyzed.

4. Results

4.1. Characteristics of Informants and Companies

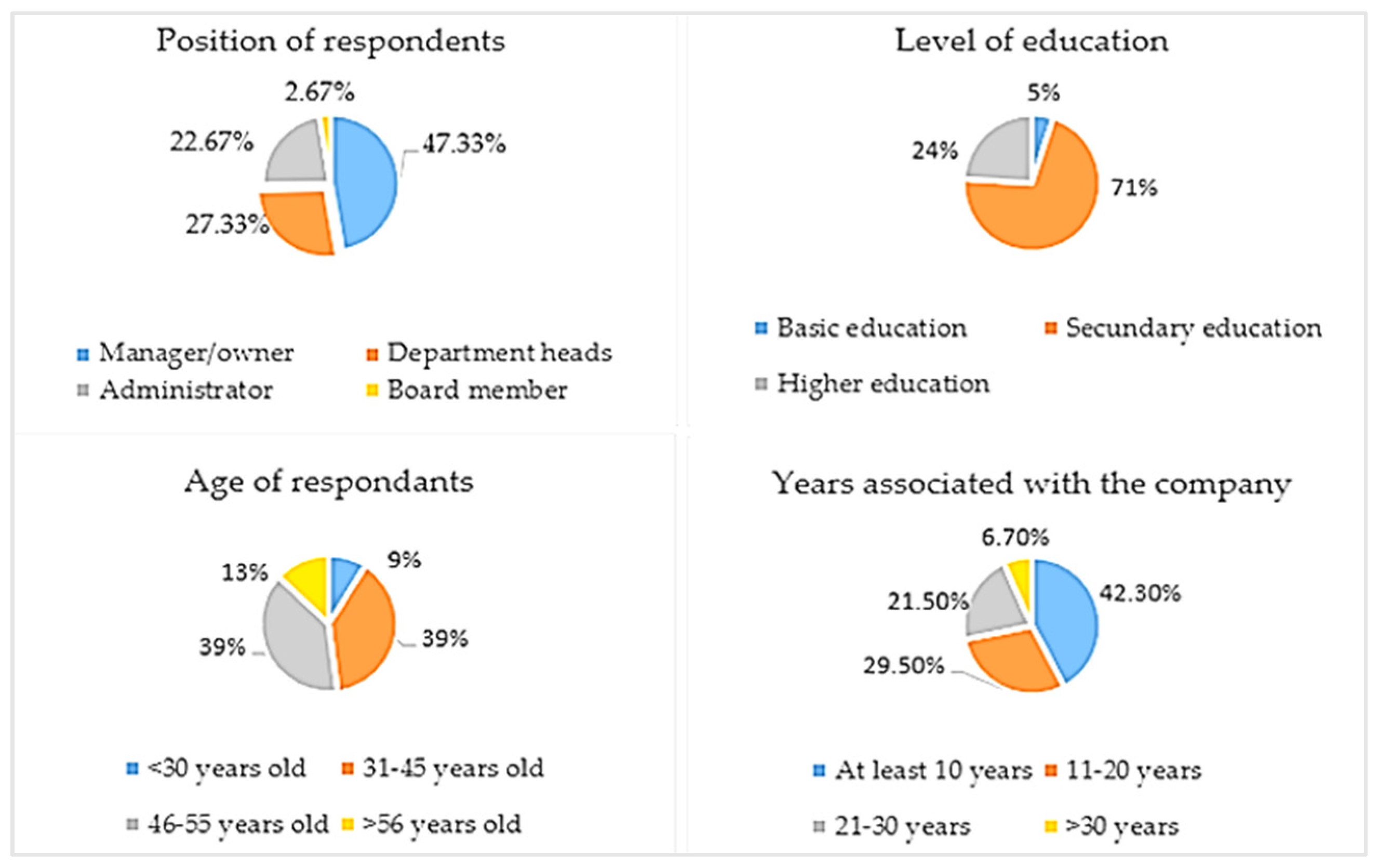

As previously indicated, the final sample included 150 innovative agri-food companies. Most of the informants were company managers/owners (47.33%), followed by department heads (finance, quality, R&D, operations, sales) (27.33%) and administrators (22.67%). The education level of the informants was mostly secondary education (70.7%), followed by higher education (24%) and basic education (5.3%). Regarding the age of the informants, 8.7% were under 30 years old; 38.7% were between 31 and 45 years old; 39.3% were between 46 and 55 years old; and 13.3% were over 56 years old. The predominant age of the informants was in the range of 31–55 years (Figure 2).

In total, 52 companies were located in the province of Badajoz (34.7% of the total) and 98 companies in the province of Cáceres (65.3% of the total).

With regard to the legal form, most of the companies were private limited companies (60.7%), of which three were unitary limited companies. Cooperatives represented 24% of the total, of which 3 were agricultural transformation companies. The rest were public limited companies, and three companies had other legal forms (self-employed and family businesses).

Regarding the size of the companies, most were micro companies (less than 10 workers), representing 47.3% of the total, and small- and medium-sized companies (SMEs), representing 34.7% of the total. The percentage of large companies (>200 workers) was low (15.3%). The size is representative of the business fabric of Extremadura. According to data from the Business Innovation Survey of the Spanish NIS, the total number of innovative companies in the agri-food industry in the period 2018–2020 was 1267 (10–49 employees) and 531 (50–249 employees). For the same period, the total number of innovative companies in all sectors at the national level was 36,026 companies, with 477 in Extremadura. It should be noted that the FIS does not provide data for companies with less than 10 employees. Table 1 shows the main characteristics of the companies.

Regarding the branches of activity (NCEA 2009 codes 10, 11, and 12, which correspond to the agri-food industry), Table 2 shows the distribution in the sample. Although all branches of activity were represented, the largest number of companies were involved in the activities of processing and preservation of meat and other meat products (24.7%), processing and preservation of fruits and vegetables (16%), manufacture of beverages (14%), manufacture of animal and vegetable oils and fats (12%), manufacture of other food products (12%), and manufacture of animal feed products (7.3%). Together, these activities represented 78.7% of the sample and are representative of the main products produced in the region (Iberian sausages, wine, oil, paprika, etc., amongst others).

4.2. Negative Consequences of the Pandemic

In accordance with the previous study by [20], the negative consequences of the pandemic were analyzed by classifying them into those that affected the financial function of the companies and those that affected their operational performance.

4.2.1. Negative Consequences Affecting the Financial Function (FC)

The main negative consequences affecting the financial function of agri-food companies were a decrease in turnover (68% of the total) and a reduction or displacement of product demand (51.3%). The effect on investments (36%) and the development of R&D projects (29.3%) was smaller.

According to the branch of activity (Table 3), a decrease in turnover (FC1) affected more than 50% of the companies in all branches (except in the manufacture of other food products (108)) but was especially notable in the manufacture of animal feed products (109), manufacture of bread and pasta (107), and manufacture of dairy products (105). Regarding the reduction/displacement of demand (FC2), it was more markedly observed in the branches of the manufacture of beverages (110), manufacture of dairy products (105), and production and preservation of meat and meat products (101). A slowdown in R&D projects (FC3) had a greater impact on the manufacture of other food products (108), manufacture of dairy products (105), and production and preservation of meat and meat products (101). A general decrease in investments (FC4) mainly affected the branches of the manufacture of bread and pasta (107), manufacture of dairy products (105), and production and preservation of meat and meat products (101). In general, the branches most affected by factors affecting the financial function of the companies were the production and preservation of meat and meat products and manufacture of dairy products.

In all cases and for each of the negative consequences affecting the financial function, the chi-square test accepted the null hypothesis that the variables analyzed were independent. Despite the different answers, there is, therefore, no association between the consequences detected in relation to the branches of activity, which affected the agri-food industry equally.

4.2.2. Negative Consequences Affecting Operational Function (OC)

Table 4 shows the results of the negative impacts that affected the companies from the operational point of view according to the different branches of activity. Mainly, industries have experienced difficulties in carrying out marketing activities (56.7%) and have experienced a decline in or even stoppage of their activities (42%). On the other hand, a lack of personnel (34%) and supply problems on the part of their suppliers (20%) have affected the operational performance of the industries to a lesser extent. In general, the branches of the manufacture of dairy products and manufacture of beverages have been the most affected by consequences on their operational function.

It is observed that companies have had difficulties in carrying out marketing activities (OC1); this has mainly affected the branches of the manufacture of beverages (110), manufacture of dairy products (105), production and preservation of meat and meat products (101), and manufacture of bread and pasta (107).

With respect to the lack of personnel (OC2), this is a consequence that has affected, in general, less than half of the companies in all the branches of activities and has mainly influenced the manufacture of animal and vegetable oils and fats (104) and manufacture of dairy products (105). A decrease in activity (OC3) was most noticeable in the manufacture of beverages (110). With regard to the negative consequence of a lack of supply by suppliers (OC4), the companies belonging to the branch of activity of the manufacture of dairy products (105) indicated that this was an important consequence that negatively affects the operational functions of the agro-industries.

For each of the negative consequences affecting the operating functions, the Pearson chi-square test accepts the null hypothesis that the variables analyzed are independent. Similarly, therefore, no association was detected between the consequences caused in operational performance, according to the branch of activity of the agri-food industry.

Finally, eight companies added additional negative impacts in the other consequences section: Mobility restrictions, which have caused a drop in the number of customers and sales (101); delays in obtaining documentation and logistics (103); increased costs (103); cancellation of on-site training activities (107); more than double the price of raw materials (109); loss of confidence in public administrations and difficulty in planning production due to reduced demand (110); drop in prices (110); and problems in presenting a new product and in collections (110).

4.3. Actions Induced by the Changes

The negative consequences highlighted in the previous sections led to a series of actions that have been driven by the pandemic’s effects on processes and procedures.

4.3.1. Actions Carried out in Processes (APr)

In relation to actions carried out by the companies in their processes for dealing with the consequences derived from the pandemic, the following stand out: increase in the use of new information technologies (ICTs) (58.7%), new marketing strategies (50%), and search for and diversification in suppliers and clients in other markets (44%). Respondents mentioned the search for and design of new products to a lesser extent (28%).

According to the branch of activity (Table 5), the search for and diversification in suppliers and clients in other markets was especially evident in the manufacture of beverages (110) and production and preservation of meat and meat products (101). The increase in the use of ICTs is an action that is especially being carried out in companies in the branches of the production and preservation of fruits and vegetables (103), manufacture of other food products (108), manufacture of beverages (110), and production and preservation of meat and meat products (101). In relation to new marketing strategies, changes were observed mainly in companies in the branches of the manufacture of beverages (110), production and preservation of meat and meat products (101), manufacture of animal and vegetable oils and fats (104), and manufacture of other food products (108). As for the search for and design of new products, these actions are being carried out by companies in the production and preservation of meat and meat products (101), as shown below.

In general, regarding the changes that are being implemented to face the undesired consequences of the pandemic, companies dedicated to the production of beverages (especially wines) and meat products (especially products derived from Iberian pork) stand out.

Despite the different answers, and with regard to the changes carried out in processes according to the branch of activity, the Pearson chi-square test accepts the null hypothesis that the variables analyzed are independent. This means that there was no association in the changes according to the branch of activity.

4.3.2. Actions Carried out in Procedures (APrd)

The implementation of stricter hygienic-sanitary protocols (73.3%) together with the reorganization of activities and personnel (51.3%) are the two main actions carried out by the industries in their procedures to face the negative effects of the pandemic. Only 10% of those surveyed increased production as an action to adapt to the new situation.

The increase in production factor was only reported in companies in the manufacture of other food products (108), production and preservation of meat and meat products (101), manufacture of bread and pasta (107), and production and preservation of fruits and vegetables (103) branches. The companies in which changes were indicated in relation to the reorganization of activities and personnel belong to the production and preservation of meat and meat products (101), manufacture of dairy products (105), and manufacture of oils and fats of animal and vegetable origin (104) branches. The implementation of more hygienic sanitary protocols is notable in almost all branches of activity (Table 6).

In relation to the changes carried out in the procedures according to the branch of activity, the Pearson’s chi-square test accepts the null hypothesis, indicating independence in the actions of the production increase (APrd1) and reorganization of activities and personnel (APrd2). The result of the chi-square test, however, rejects the null hypothesis of no association (independence) in relation to the response of implementing stricter hygiene and sanitary protocols (APrd3), indicating the existence of an association due to the specific and varied measures adopted depending on the activity.

As in the previous block of questions (negative consequences), most of the companies indicated one or several actions were carried out. Only nine companies (representing 6% of the total) indicated that they did not carry out any type of action (eight private limited companies and one cooperative).

4.4. Changes Made to Meet Customer Needs

Finally, the changes that agri-food companies have been forced to make in order to meet customer needs in terms of products, services, brands, product format, and consumption behavior were analyzed.

4.4.1. Changes in Products

Nearly half of the companies surveyed indicated that they had not made any changes in the products offered. Of the companies that did make changes, the main ones reported an expansion of services (46 companies) followed by the development of new products (40 companies). A small number of companies (21) reported that they made changes in product design and 28 companies reported improved product features. A total of 39 companies revealed that they made more than one change to the products indicated.

According to the branch of activity, Table 7 shows the companies that indicated that they made changes to their products. The branches of the production and preservation of meat and meat products (101), manufacture of beverages (110), manufacture of other food products (108), manufacture of animal feed products (109), and production and preservation of fruits and vegetables (103) stand out.

For all changes made regarding products according to the branch of activity, the Pearson chi-square test accepts the null hypothesis that the variables analyzed are independent.

Other additional changes specified by the companies were the diversification and opening of new sales and marketing channels and guaranteeing product quality.

4.4.2. Changes in Terms of Service Provision

Of the companies that responded positively to the implementation of changes in services, 47 companies revealed the provision of new services (47 companies) and the expansion of their services (47 companies). Only 16 companies (10.67%) indicated the implementation of a new design, and 36 companies (24%) improved their characteristics. A total of 65 companies indicated that they had not acted differently in this regard while 39 companies reported that they made more than one change to the services.

According to the branch of activity, Table 8 shows the companies that reported changes in their services. Firms in the branch of the production and preservation of meat and meat products (101) stand out in all aspects, manufacture of other food products (108) in new services and expansion of services, manufacture of dairy products (105) in new services and improvement of their characteristics, manufacture of other food products (108) in new design, and manufacture of beverages (110) in new services and expansion of services.

As shown in the last row of Table 8, the Pearson chi-square test accepts the null hypothesis that changes made to services according to the branch of activity are independent and so there is no difference in the changes made to services.

Other additional changes indicated by the companies were the assumption of transportation costs to facilitate sales to customers, providing better services according to needs and improving payment conditions, replacing the functions of some employees, and adapting to health regulations.

4.4.3. Changes in Terms of Brand

Few changes have been made in relation to this variable. Only 42 of the 150 companies responded positively, indicating actions related to the brand. Of note was the creation of new brands in 28 companies (18.7%). On the other hand, 20 companies (13.3%) indicated changes in relation to brand extension.

According to the branch of activity, Table 9 shows the companies that reported making changes in their brand. Firms in the production and preservation of meat and meat products (101) branch and manufacture of animal feed products (109) stood out, mainly with regard to brand extension, and firms in the manufacture of animal feed products (109) and manufacture of beverages (110) branches were notable in terms of new brands.

The Pearson chi-square test accepts the null hypothesis that the variables analyzed are independent. There is no association between changes in the brand according to the branch of activity.

4.4.4. Changes in Product Format

As in the previous aspect, only a small number of companies (55 companies) reported making changes to the product format. In total, 44 companies (29.3% of the total) reported making changes to the packaging and 36 companies (24%) reported an increase in the size of their product packaging.

According to the branch of activity (Table 10), firms in the production and preservation of meat and meat products (101) branch indicated that they made changes in terms of the two questions posed; the manufacture of oils and fats of animal and vegetable origin (104), manufacture of dairy products (105), and manufacture of bread and pasta (107) to new sizes; and the manufacture of beverages (110) to new packaging.

For the changes in the format of the products according to the branch of activity, the Pearson chi-square test accepts the null hypothesis that the variables analyzed are independent. This means there is no association between these types of changes depending on the branch of activity in the agri-food industry.

4.4.5. Changes in Consumer Behavior

Finally, changes in terms of consumption behavior were analyzed. The change in payment methods, indicated by 43 companies (28.7%), stands out. A total of 67.2% of the companies (94 companies) did not make any change in this aspect. A total of 13 companies indicated that they made more than one change.

According to the branch of activity (Table 11), in relation to changes in consumption behavior, companies in the processing and preservation of fish, crustaceans, and mollusks (102) stand out regarding change in the suppliers and vertical integration. The production and preservation of meat and meat products (101), manufacture of dairy products (105), and manufacture of beverages (110) stand out in terms of payment method changes.

The Pearson chi-square test accepts the null hypothesis that the variables analyzed (changes made according to consumer behavior and branches of activity) are independent.

Other actions in addition to the questions indicated were direct home deliveries (telematic sales) and the search for new customers.

5. Discussion

The results obtained in this study show that, despite the negative consequences resulting from the speed and spread of the pandemic since the first infections appeared at the end of 2019, the agri-food industry has experienced a softer decline than the manufacturing industry as a whole. This general result coincides with that obtained in the study conducted by Caldart et al. [71], which analyzed the opinions of senior managers of 185 companies related to the food and beverage sector on the impact of COVID-19 on the sector and their companies.

Generally, and coinciding with the study by Vázquez-Martínez et al. [11], the challenging and changing scenario caused by the pandemic means that organizations belonging to the food sector have faced impacts that have not previously been considered. However, it can be seen that all companies, regardless of their branches of activity, carried out actions and procedures as a result of the negative impacts they suffered.

5.1. Negative Consequences of the COVID-19 Pandemic on the Development of Agri-Food Companies

5.1.1. Negative Consequences of the Pandemic in Financial Functions

Extremaduran agri-food industries perceived a decrease in their turnover as the greatest negative consequence of the pandemic affecting their financial function, as has been shown in other reports [15,68]. This negative consequence was reported by more than 50% of the companies in all branches of activity, with the exclusion of the manufacture of other food products group. In addition, more than 85% of the branches of the tobacco industry and the manufacture of beverages have seen their turnover particularly affected. In the case of the tobacco industry, as reported in García [87], monthly tobacco sales from the month of March 2020 began to fall by 23.8% in April compared to the same month in 2019. Unlike other sectors, tobacconists remained open during the March and April confinement. However, the restrictions associated with other activities, such as tourism, catering, and nightlife, have also had an impact on the tobacco sector, as leisure and social time has been reduced, and tourism has an influence on many sectors. Regarding beverage manufacturing, 100% of the companies are wine and beer (alcoholic beverages) manufacturers and have seen their turnover decrease, as indicated by 85.7% of the total. This trend is in line with what was previously observed in the tobacco industry [87]. The decline in turnover occurred despite the fact that alcohol continued to be available at all times, although this trend seems to confirm the importance of the social consumption of alcoholic beverages. The overall drop in drinking did not prevent a likely increase in alcohol ingested at home since during the months of confinement, a large increase in the purchase of products usually consumed in bars and restaurants, such as wine, beer, and spirits, was observed, although not in the same volume [63,88]. In the study by Villanueva et al. [88], it was examined whether risky drinking varied during the COVID-19 confinement. The conclusions were that risky drinking declined across the board during the COVID-19 confinement, although changes in the prevalence and likelihood of being a risky alcohol user were dependent on sociodemographic variables.

Industries have also been affected by the shift in demand for products. There has been a decrease in the demand for some food products as a result of the restrictions and measures adopted by governments to deal with the pandemic. As indicated in the study by Pérez-Rodrigo et al. [73], the pandemic is generating changes in food consumption patterns. Thus, since the first confinement was decreed in Spain until the “new normality” (14 March–21 June), food consumption trends were oriented towards the consumption of healthier, fresh, and nutritionally rich products. In line with the study by Bona et al. [40], the lockdown led to the growth of certain product categories related to healthy habits, such as increased consumption of fresh food.

The report by the MAPA [74] indicated that during the first confinement in Spain, a greater demand for fruits, vegetables, legumes, cereals, and dairy products was observed in shopping baskets, a trend that has been maintained in subsequent reports [75]. Consequently, the branches of activity that were most affected are meat and beverage manufacturing. Companies in the processing and preserving of meat and other meat products branch have seen their demand drop. According to the study by Sinisterra-Loaiza et al. [89], this trend can be explained by the fact that most of the meat companies in the sample not only work with fresh meats but also manufacture sausages and cold cuts, which could be perceived by consumers as less healthy products.

Moreover, the manufacture of beverages branch of activity has also experienced a notable shift in the demand for its products. In the case of sparkling wines, the decline in sales and the shift to other types of wines, such as still wines, is basically due to the fact that the sparkling wine category is closely associated with celebratory occasions, although producers are increasingly making great marketing and communication efforts to change this perception regarding the moment of consumption. As the study by Bharadwaj et al. [39] states, the unequal impact of the pandemic across sectors of activity is determined by consumer behavior.

On the other hand, coinciding with the report by FIAB [68], companies perceived the decrease in the investment budget (36% of the total) and slowdown in R&D projects (29.3% of the total) as minor negative consequences affecting their financial function.

With regard to the Extremaduran region, the report by Hernández-Mogollón et al. [15] analyzed the impact of the health crisis on SMEs in Extremadura in general. This report highlights the effect that the pandemic has had on the fall in sales. It also shows that the greatest economic-financial impact of turnover, profitability, and productivity has fallen on micro-enterprises (less than 10 workers) while for the effect on investments, the level of debt and liquidity has had a more negative effect on medium-sized companies.

5.1.2. Negative Consequences of the Pandemic in Operational Functions

With respect to the negative consequences affecting the operational function of the industries, these have had an effect mainly on their marketing activities (56.7% of the total). In general, as has happened worldwide, the agri-food industries in Extremadura have experienced difficulties in carrying out trade activities due to the virus containment measures. The physical closing of international borders has had negative impacts on the freedom of the exchange of goods, although the flexibilization and relaxation measures of governments, together with the resilience of companies, have contributed to soften this negative trend [28,29].

However, other measures adopted to control the virus, such as the closure of catering establishments or the limitation of opening hours, have been extended over time depending on the speed and characteristics of the propagation of the pandemic. This has caused changes in food marketing channels. As it is concluded in the study by Bolívar et al. [46], 90% of companies have changed the use of channels in their relationship with their customers during the pandemic, with the web and its apps being preferred by the customer when contracting new products. Similarly, some organizations have been forced to implement teleworking to ensure business continuity [47,48].

Specifically, the most adversely affected channel is the HORECA channel [50,71]. In the study by Escobar et al. [50], a survey was carried out to assess the impact of the situation on the agri-food sector in Spain along the entire value chain. Among the results obtained, the majority of the channels used were reduced, especially in the case of the HORECA channel. Similar results are presented in the report by Caldart et al. [71], which analyzed the impact and future of the food and beverage sector due to the pandemic crisis. This fact also coincides with the findings of this study, so the branches of activities most closely related to the hospitality industry, such as the manufacture of beverages or the manufacture of dairy products, where cheese is included, and, finally, the industries that produce, transform, or market meat and meat products have stated that they have been significantly affected.

Industries in the food and beverage sector have also been adversely affected operationally because of the reduced availability of personnel due to sick leave caused by the COVID-19 infection as shown in studies from [52,53]. In addition, labor shortages have contributed in part to the occasional decline in activity in some production centers. According to the study by Corchuelo et al. [20], this negative effect was enhanced in agro-industrial branches that concentrate their activity on seasonal work campaigns due to the characteristics of their products, as is the case of fruits and vegetables. Thus, the large food processing industries have been forced to introduce staggered entries to work centers, thus reducing interpersonal contact at specific times of peak activity. Finally, the results reveal that the lack of supplies from suppliers has also affected the operational functioning of the companies (20% of the total), although to a lesser extent. The processing and preservation of fish, crustaceans, and mollusks branch of activity has been the most affected. This may be explained by the fact that most of the raw materials with which the fish processing industries are supplied with are from coastal areas, with the exception of lake fishing and aquaculture, since Extremadura is an inland region; so, at specific times during the pandemic, they may have been affected by the lack of goods from some of their abroad suppliers.

5.2. Actions Taken to Deal with the Negative Consequences

5.2.1. Actions in Processes Undertaken to Deal with the Consequences of the COVID-19 Pandemic

In response, industries belonging to the food sector have incorporated and continue to include actions in their activities to minimize the negative effects caused by the pandemic [52,53,58,59]. First, with respect to the changes they implemented in their processes and as shown by other previous studies and reports, the pandemic has accelerated the trend towards a digital economy [15]. In this sense, governments have adopted measures to restrict physical interpersonal contact, forcing people to interact and work remotely [23,24,25,26,27].

In general, these results are in line with what has happened in other economic sectors, as shown in several studies. The food industry has undergone changes in the way it relates to its workers, suppliers, and customers. On the one hand, the agri-food industries, as far as possible, have incorporated teleworking in some areas of work not related to production, such as administration, thus allowing them to continue with their activities as evidenced by previous studies [15,48]. The food sector has also used new channels to relate to the market, such as the use of virtual communication and purchasing platforms, an action which industries belonging to the beverage processing branch have highlighted above the rest according to the reports [63,72]. Another action manifested by agro-industries is the search for different clients and suppliers in alternative markets [46,47]. The results show, however, that the search for and design of new products is less frequently mentioned by the companies as an action carried out in the processes.

5.2.2. Actions in Procedures Undertaken to Deal with the Consequences of the COVID-19 Pandemic

The industries of the food sector have also incorporated actions in their procedures to minimize the negative consequences of the pandemic in their activities. Mainly, the implementation of hygienic-sanitary protocols (73.3% of the total) and the reorganization of activities and personnel (51.3%) stand out, notwithstanding the fact that the food industry usually has very demanding criteria regarding quality, hygiene, and food safety. In this sense, the pandemic has caused a revision of these standards to ensure supply and safety throughout the food chain. In addition, those industries that manufacture and market products for different channels, such as retail and HORECA, have had to reorganize their activities. For example, in the study conducted by Corchuelo et al. [20], the actions carried out by a meat company that was targeting the restaurant sector as its main market and, in January 2020, was beginning to implement lines for the retail channel, mainly for sales in supermarkets, are described. The pandemic has accelerated the incorporation of new lines that will allow marketing of a greater volume of its products in supermarkets and hypermarkets in an attempt to compensate for the losses that will be generated by the closure of the hotel and catering business.

5.3. Changes Made as a Result of the Pandemic in Terms of Product, Services, Brand, Product Format, and Consumer Behavior

The agri-food industries have incorporated changes mainly in the performance of their products and services to meet the changing market trends and the demands of their customers. Conversely, with regard to changes in terms of the brand and format of their products, 70% of the total number of industries surveyed in Extremadura did not incorporate these changes into their products (64% of the total). Therefore, and in relation to the study by Corchuelo and Mesías [17], despite the fact that the agri-food industry suffers from chronic problems, in addition to the difficult and changing pandemic scenario, the agri-food sector is undergoing substantial changes as it sees the need to include innovation within its strategies and change its products. As the study by Corchuelo and Martín-Vegas [19] stated, the incorporation of innovation (technological and non-technological) offers agri-food companies the opportunity to increase their income, productivity, and competitiveness, which is especially relevant in crisis situations.

5.4. Differences in Terms of Effects/Actions/Changes According to Branches of Activity

It was observed that, except for the implementation of stricter hygienic-sanitary measures, the results of the chi-square test reveal that there is independence between the consequences, actions, and changes carried out on the basis of the branches of activity, which reveals that the pandemic has affected the agri-food industry equally. In short, the pandemic has unfavorably affected the financial and operational performance of all branches of the food industries in Extremadura. This fact has brought about actions in processes and procedures aimed at overcoming these negative effects. Mainly, there has been a trend towards the acceleration of digitalization and the incorporation of even more demanding hygienic-sanitary protocols, and the reorganization of activities and personnel. The main changes that industries are incorporating entail the provision of their customers with improved benefits related to their products and services.

This study has some limitations, such as its cross-sectional nature in the analysis of data referring to a specific moment in time, and the fact that it was directed at a sample of companies to analyze the impact of the pandemic in a specific sector of a region. This study and the results obtained are, however, a precedent in the study of the impact of COVID-19 on a specific industry and a basis for exploring and extending the effects of the pandemic crisis during the post-pandemic stage in the agri-food industry and other industries at the regional or national level.

6. Conclusions

The COVID-19 pandemic has affected all sectors of economic activity worldwide. In general, the Spanish agricultural sector has also been affected by the characteristics and speed of the spread of the pandemic, although to a lesser extent than other sectors directly dependent on the service sector, such as tourism.

The agri-food sector in Extremadura, the region on which this study was focused, is strategic for promoting the economic and territorial development of the region. This research aimed to analyze the impact, consequences, actions, and changes of the pandemic on innovative agro-industries in different branches of activity to determine which activities were most affected and whether there were differences between them depending on the nature of the product, process, or services. This study fills a gap by providing an overview of the effects of the pandemic in this sector and its branches of activities.

According to the results obtained, the pandemic has had different negative impacts on the financial performance of the Extremadura agri-food industry (decrease in turnover and demand of products in the branches of agri-food activity). This has affected, in particular, firms related to the HORECA channel, which remained closed and suffered numerous restrictions from the state of alarm in March 2020. Agro-industries have also faced difficulties affecting their operational performance. The lack of personnel is one of the main ones, especially in those activities related to the seasonality of their products (e.g., fruit and vegetable plants), and the difficulties in carrying out marketing activities. In response, firms have taken actions that have allowed them to adapt their activities and face the negative effects, guaranteeing their continuity. Mainly, the industries have promoted the use of ICTs in their communication and trade activities, and the incorporation of more demanding hygienic and sanitary protocols. In relation to the changes included in their organizations, these have mainly been based on the performance of their products and services. The consequences, actions, and changes produced by the pandemic have affected the agri-food industry equally and, except in the implementation of more demanding hygienic and sanitary protocols, there were no associations between them and the different branches of activity.

The main conclusion is that the agri-food industry has not stopped its activity and has developed strategies that allow it to guarantee the food supply by adapting to the characteristics of the pandemic spread.

The findings may be beneficial for senior executives of Extremadura agri-food companies and for the public administration of the region, providing information for the development of initiatives that can mitigate the negative effects of the pandemic and favor the implementation of actions that help the adaptation of agro-industrial activities.

In this sense, this study has two main implications. On the one hand, it provides an overview to the managers of agribusinesses of the importance of the impact of the pandemic on their businesses and the actions carried out by other managers according to their branches of activity. On the other hand, it provides a contribution as a guide for public administrations, particularly the regional government, in the endorsement of specialized measures that can diminish the prejudicial consequences according to the branch of activity in the sector, and help to overcome the changes that are necessary. These measures are aimed at promoting policies that maintain the profitability of the activities, and especially focus on the value of the food system for people’s health, and an awareness of healthy eating styles. Agricultural policies must also incorporate measures to ensure the global sustainability of food and agricultural systems, and the supply and production.

Author Contributions

Conceptualization, C.S.-B. and B.C.M.-A.; methodology, B.C.M.-A. and C.S.-B.; formal analysis, B.C.M.-A. and C.S.-B.; investigation, C.S.-B. and B.C.M.-A.; data curation, B.C.M.-A. and C.S.-B.; writing—original draft preparation, C.S.-B. and B.C.M.-A.; writing—review and editing, C.S.-B. and B.C.M.-A.; visualization, C.S.-B. and B.C.M.-A.; supervision, C.S.-B. and B.C.M.-A.; project administration, B.C.M.-A.; funding acquisition, B.C.M.-A. All authors have read and agreed to the published version of the manuscript.

Funding

This research was financed by the Junta de Extremadura (Spain) and European Regional Development Fund grant number IB18040 and GR21134 (SEJ022-Research Group INVE).

Informed Consent Statement

Informed consent was obtained from all subjects involved in this study.

Data Availability Statement

Not applicable.

Acknowledgments

An initial version of this paper was introduced at the workshop ‘Economías de aglomeración y desarrollo rural: innovación, competitividad e internacionalización frente a la despoblación’ [Agglomeration economies and rural development: innovation, competitiveness, and internationalisation in the face of depopulation], Universidad de Extremadura, May 2021. We would like to thank the participants and organizers of this workshop. The authors also would like to thank the anonymous referees and the editors for their helpful suggestions on the earlier draft of our paper. Finally, our special thanks also go to Pedro Eugenio López-Salazar, co-author of the questionnaire and research design who, unfortunately, due to the consequences of this pandemic, has not been able to continue with this project.

Conflicts of Interest

The authors affirm no conflict of interest.

Abbreviations

| Acronyms and abbreviations | |

| Apr | Actions in processes |

| APrd | Actions in procedures |

| APO | Asian Productivity Organisation |

| CFO | Chief Financial Officer |

| FAO | Food and Agriculture Organisation |

| GDP | Gross Domestic Product |

| GVA | Gross Value Added |

| HORECA | Hotel, Restaurants and Café |

| FC | Financial consequences |

| ICT | Information and Communication Technology |

| IFM | International Monetary Fund |

| MAPA | Ministry of Agriculture, Fisheries and Food |

| NCEA-2009 | National Classification of Economic Activities |

| NIS | National Institute of Statistics |

| OC | Operational consequences |

| OECD | Organisation for Co-operation and Development |

| SME | Small and medium enterprise |

| UN | United Nations |

Appendix A. Questionnaire

| Block I: Characterization data of the company and the informant | |

| 1. Name of informant:___________________________________________________________________ | |

| |

| Basic education | |

| Secondary education | |

| Higher education | |

| 2. Company name: | |

| (a) Location:_________________________________________________________________________ | |

| (b) Province:_________________________________________________________________________ | |

| (c) Municipality:______________________________________________________________________ | |

| (d) Year of creation of the company:_____________________________________________________ | |

| (e) Sector of activity (NCAE-2009):______________________________________________________ | |

| (f) Description of the activity:___________________________________________________________ | |

| (g) Company size (number of employees): | |

| <10 employees | |

| 10–49 employees | |

| 50–199 employees | |

| >200 employees | |

| (h) Legal form: | |

| Cooperative | |

| Private limited company | |

| Public limited company | |

| Other legal form____________________________________________________________ | |

| (i) Approximate turnover range: | |

| 0–500,000 € | |

| 500,001–1,000,000 € | |

| 1,000,001–2,000,000 € | |

| 2,000,001–6,000,000 € | |